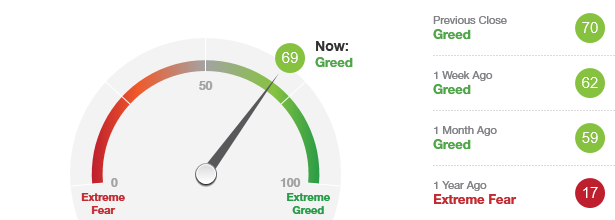

Market Overview

This month's charts are posted. There are NO CHANGES in the models.

Could Brexit be good for your portfolio?

The United Kingdom is leaving the European Union! Implications for global trade could be disastrous! Implications for the global financial industry could be even worse! The British government is in disarray! People are panicking!

But should they? To say the U.K. has weathered worse would be so trite an understatement that even the British – for whom understatement is as much a part of their idiom as lifts, queues and car parks – would consider it too obvious.

So keep calm, carry on, and realize Brexit is not the doomsday scenario it’s often painted as. And it just might lead to found money for the typical American investor.

What happens next

Whether or not Brexit is a good idea, whether or not the politicians and their operatives committed some truly stunning malpractice (they did), no matter how close the vote was or how many people might change their vote today, an election is an election and the “Leave side” beat the “Remain side” on the one day it counted. Many Britons who opposed Brexit with every fibre of their beings want to see it executed now because even if they disagree with the decision it’s the will of the British people as a whole and needs be respected.

The holdup is that it’s not as simple as just pulling up a drawbridge. Once the U.K. and E.U. go their separate ways, suddenly new trade agreements have to be put in place, rights of Europeans in Britain and Britons in Europe must be mutually guaranteed and a ton of new customs officers and passport control agents need to be hired and deployed by both sides.

And it’s that last part that’s touchy. Border control would actually be pretty easy, considering Great Britain is an island. You just reconfigure the airport security lanes, beef up customs at the ports, back up traffic from one end of the Chunnel to the other and, as the Brits say, “Bob’s your uncle.”

The fly in this ointment is that the long name of the country is the United Kingdom of Great Britain and Northern Ireland. In 1921, following their own Leave vs. Remain vote, six Irish counties in the Ulster province chose to stay part of Britain, while the other 26 counties eventually formed the Republic of Ireland that exists today – importantly, as an E.U. member state. Still, there is no appetite for a land border between Ulster and the other three Irish provinces.

But that’s exactly how it’s playing. Regardless of what the Irish think of the prospect, such a border must exist to protect the sovereignty of both the U.K. and the E.U.

The majority of the English, Scottish and Welsh also don’t like the idea, nor do they like the proposed “back stop” that would allow an unguarded border in Ireland. And they have a point: Why bother paying a tariff at the Port of Grimsby when you can just ship your cargo to Dublin and drive north?

The only way to square this circle would be for the U.K. to invade and conquer Ireland again, and that is not a policy currently under consideration by any responsible party.

England’s long, contentious history with Ireland hit an all-time low with the 1649 assault on Drogheda. Nobody is suggesting that this should be the model for Brexit, but nobody can agree on any other way, so … Credit: Henry Doyle (1868).

So the choice now is between a deal that involves the back stop and no deal at all, a so-called “hard Brexit” in which the U.K. “crashes out of the E.U.” as the pundits like to say. That could have some devastating effects on both trade and investment throughout both continental Europe and the British Isles.

It’s not as bad as it looks

There will be some serious pain on both sides. But the case could be made that the pain would be short-term and, perhaps, worth it in the long run.

First, other countries have endured sudden economic disruptions and thrived in the aftermath. India had a major calamity in 2016, when all 500- and 1,000-rupee notes had to be taken out of circulation without notice because of rampant counterfeiting and other financial crimes. If you had any of those notes in your wallet, they were immediately declared worthless. A cash shortage ensued, and a lot of ordinary Indians lost a lot of money. But the one-off event solved the problems it needed to solve – though it won the government few fans. India’s GDP growth rate lost a percent or two for each of the subsequent years but is now back to the status quo ante.

We’re reminded of Poland’s Balcerowicz Plan – usually called “Shock Treatment” which is easier to spell. It called for the nation, newly freed from Soviet domination and the associated command economy, to adopt market capitalism overnight (literally: December 31, 1989 to January 1, 1990). Prices spiked. Inefficient companies went bankrupt. People were thrown out of work. And three years later, Poland had the fastest growing economy in Europe. Economists widely credit Shock Treatment – with a small assist from the International Monetary Fund – for a turnaround that was little short of miraculous.

Britain itself has, at the edge of living memory, experienced something almost as extreme. In the wake of the Second World War, the leading national economies were governed by the Bretton Woods accords which, among other things, established the U.S. dollar as the only currency to be pegged to a gold standard, with all the other currencies pegged to the dollar. The British pound sterling was set at $4.03, near its historic norms up to that point. Then one day in 1949, Britons woke up to a pound note that was worth only $2.80. It’s less than half that today but the White Cliffs of Dover have not crumbled into the Channel.

That said, it’s clear Britain, despite London’s world leadership in financial services, has not seen the sort of economic growth in recent years enjoyed by its former viceroyalties, or its rivals on the Continent. For that matter, the standard of living in Ireland has long eclipsed that of the U.K. Again, there’s no point in relitigating Leave vs. Remain, but the Brexiteers wouldn’t have been able to make their case if there weren’t some legitimate, widely felt displeasure about Britain’s economy as compared to its neighbors’.

Speaking of its neighbors, it’s important to note that Britain isn’t the only European(-ish) nation that declines the honor of E.U. membership. It joins Norway and Switzerland and others – including Greenland, which pulled out of what was then called the European Economic Community in 1985. None of them are going broke, and Brussels isn’t leaning on them to join. That’s because there’s an organization called the European Free Trade Association, which promotes commerce in the region regardless of E.U. membership status. The EFTA spans pretty much from one end of Europe to the other, including studiously neutral Switzerland. Instead, these non-E.U. countries within EFTA deal quite well with the E.U. via bilateral trade agreements. So Britain has a well-trodden path to continue doing business business with Europe without remaining part of Europe.

It’s also important to remember that Britain, through much of its history, was in competition with the Continent’s other states. That’s why it established the British Empire, which survives today in a diluted form known as Commonwealth of Nations. Those 53 countries, mostly former colonies, present a natural alternative trading bloc. The Commonwealth comprises one-fifth of the world’s land mass, so whatever the U.K. might want to buy from E.U. nations it could probably find somewhere in there.

Good news for Americans?

If we’re going to talk about former British colonies, we ought to take a look in the mirror. Brexit is bound to lead to increased bilateral trade with the United States and its partners in NAFTA – or whatever, if anything, comes next. (That’ll have to be another article.) This, in turn, could lead to higher revenues for firms based here as tariff-adjusted prices for agricultural products, cars, planes and everything else the U.S. and E.U. compete on suddenly start favoring American vendors.

Historically, 40% of the revenues of S&P 500 firms have tended to come from international operations. That figure has trended down sharply in recent years, but it’s still around 30%. The U.K. is the third-largest overseas trading partner for these large American companies, accounting for 2.5% of the total. It might not overtake No. 1 China – which generates 4.3% of S&P 500 sales – but Brexit could very well cause Britain to overtake Japan’s 2.6% slice by growing the pie as a whole.

Meanwhile, Brexit could also cause a windfall for its Commonwealth partners, so U.S. investors would be wise to look at emerging market funds as well as the S&P. Blending those Brexit-specific opportunities with those driven by other world events and by ongoing economic cycles is always an exercise in complexity, though. Maybe not on the scale of negotiating a divorce from the E.U., but complex nonetheless. As you already know - best to consult a professional financial advisor in these instances.