This month's models have been posted. There are CHANGES in EVERY MODEL. New funds are highlighted in yellow.

Expansive times

The good news – and there’s plenty of it – is that the economy is doing very well. The U.S. economy just notched its 121st consecutive month of expansion. That is, it has been more than a decade since America experienced two consecutive quarters of negative gross domestic product (GDP), which is what defines a recession. That has never happened before. Even the dotcom-fueled, peace dividend-financed expansion of the 1990s petered out after 120 months.

The bad news– and there’s some of that too – is that doesn’t mean this is the strongest economy we’ve ever seen. In the 1990s’ expansion, GDP grew at an overall annualized rate of 3.6%, compared to the current 2.3%. Employment growth then averaged 2.0% per year, compared to today’s 1.4% annualized increase in jobs. By those two metrics, the expansions of the 1950s and ‘60s were even more vibrant. Surprisingly – to us more than anyone – the expansion that stretched from March 1975 to January 1980 saw 4.3% annualized GDP growth and 3.6% annualized job growth. We don’t recall the Ford and Carter years that fondly, but those are the numbers.

And therein lies a tale.

Why this time feels good

The difference between now and the late 1970s has nothing to do with GDP or job growth. It has to do with how everyday people experience the economy.

While The Jeffersons were movin’ on up, they were leaving a lot of people behind. It wasn’t that average Americans couldn’t find jobs or that goods weren’t available to satisfy demand. That was all working well. The problem was, while wages were going up 3.6% per year, prices were going up several times that. Inflation never fell below 5% year-over-year and, at its peak, hit 14.6%.

Remember these? Credit: ACOwatch.me

So even though the numbers on the paycheck were getting bigger, the prices at the stores were getting higher faster. The numbers at the gas pump were even worse. Who could afford $1.19 per gallon? Such a gouging!

Another reason why the late 1970s didn’t feel like a recovery is that interest rates were enormous. The fed funds rate is the risk-free interest rate. It’s what the Federal Reserve and the largest banks charge each other for overnight deposits. It’s a fraction of the prime rate, which is the best rate banks will lend to anyone who isn’t a bank. Anything you borrow for – mortgage, car, education, furniture– will be higher than that. The effective fed funds rate at the end of the 1975-1980 expansion was 17.61%. That’s what Chase Manhattan charged Manufacturers Hanover. Today it’s what you pay when you carry a hefty balance on your credit card.

So the current expansion really does feel like an expansion. Not only are there jobs, but inflation and interest rates are low, and have been for so long that it seems like the natural order of things.

Why this time doesn’t feel good for everyone

Fast-forwarding through an expansion or two, there’s an apocryphal story that President Bill Clinton bragged to a crowd during the 1990s boom times about how many millions of jobs he “created.” A heckler in the crowd, the story goes, shouted out, “I know. I got three of ‘em!”

There’s political hay to be made out of presenting the average American as needing to work multiple jobs to make ends meet. The data don’t back that up, though. Only about 5% of American workers have more than one job – in the formal economy at least – and that number hasn’t changed much over time.

But it is more complicated now with the rise of the gig economy. Nobody knows for sure what proportion of Americans work as contractors instead of on the books as employees, but the numbers seem to coalesce somewhere around one-third. Some of these people, perhaps most, make a decent living, but they are foregoing healthcare insurance, retirement plans and educational benefits that usually go with full-time employment. For them, these are not necessarily the best of times.

This overlaps with underemployment – defined officially in its most narrow form as working part-time but desiring to work full-time. According to the Bureau of Labor Statistics, that’s 2.9%, which is actually a fairly satisfactory number. But Gallup, the polling company, also looks at people who are working full-time but below their skill level, who puts the number at 12.6%. This is a subjective thing, of course.

Policy matters

When stories started appearing about how old this expansion is, it might have taken some people by surprise. It doesn’t seem that old, does it?

Economists often conflate the words “expansion” and “recovery” as they both refer to the time between recessions. The difference is really one of confidence. It’s hard to tell a recovery from a recession when you’re in the middle of it.

The recovery phase was really quite a long slog. It consumed all of President Obama’s first term and much of his second. It’s hard to say at what point – a date in time, an employment milestone reached –the nation regained confidence in its own economic might, but the argument could be made for the third quarter of 2015. That’s the moment when wage growth started to exceed inflation. Average hourly wages, net of inflation, are still rising – but slowly.

Having hit on inflation and interest rates – the twin pickpockets the Fed is charged with policing – we should turn briefly to that other thief in the night, taxes. Although tax policy is generally proposed by the president and is thus closely associated with him, it is actually the purview of Congress.

Not that this distinction matters. The average federal tax rate for all households was 22.4% in 1980. Today – after the Reagan Revolution, the Trump tax reform and all the other changes that came out of the Ways and Means Committee in between, that number hasn’t yet dropped into the teens. Of all the economic factors over the past 40 years, the proportion of our income we give to Uncle Sam looks to be the most constant.

Getting it right from here

Not that consistency is bad. A 10-year expansion – even one that isn’t all that strong on a month-to-month basis – is a good thing. Consistency in economic policy, though, is not a given in 2019.

President Trump made some outstanding nominations for Federal Reserve governorships early in his term. But he has lately been critical of the job they have done so far, despite their role in promoting a generally strong economy. They recently, in a controversial action, cut interest rates due at least in part to the president’s words and deeds. Only time will tell whether this was the right move or the wrong move. The same could be said about the question of the Fed’s independence. Has the central bank lost its autonomy under Mr. Trump, or did he just reveal to the rest of us that this autonomy was always an illusion?

While we ponder that, though, it’s best to keep things in perspective. Compared to where the rest of the world is in this moment, the U.S. is certainly the economic envy of all its trading partners.

Are you over 59 ½?

Most investors know that you’re allowed to transfer the money in your 401k account to an IRA after retirement, but did you know you can transfer 401k money years before retirement? Without penalty. Without taxes.

The technique is known as an “In-Service Rollover” and is available to any retirement plan participant who is 59 ½ or older. Federal law and your FedEx 401k plan provisions allow you to transfer a sizable portion of your 401k over to an IRA in your name. An In-Service Rollover (ISR) allows you to get more control of your hard-earned money, and in many cases you can upgrade the investments available to you.

Call us today at 1-800-301-8486, or email us at emailinfo@smithanglin.com, to learn more about the benefits of an In-Service Rollover, and whether doing one is right for you.

Provided by Smith Anglin, a 2018 Financial Times 300 Top Registered Investment Adviser Firm.

U.S. GDP grew at a +2.1%. annualized rate in the second quarter. This was significantly lower than the 3.1% posted in the first quarter, but consecutive quarters of over +3% GDP growth is a rare thing for a developed economy.

US Stocks

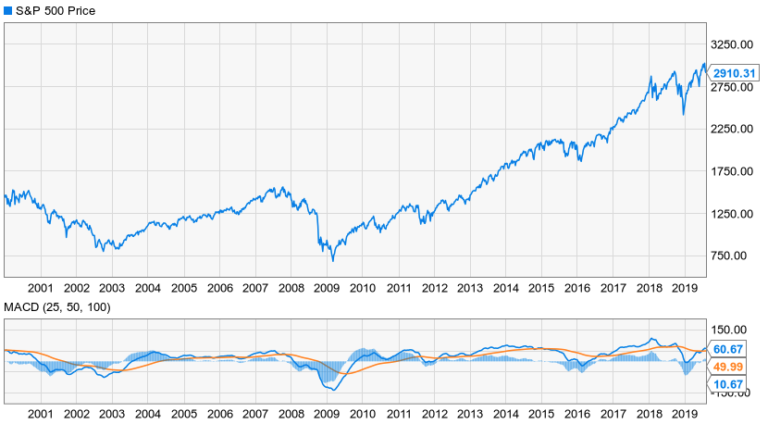

U.S. equities continued to press into record-high territory in July, but with less enthusiasm than they showed the previous month. The S&P 500 wound up +1.3% for the month, following a fairly spikey line to get there.

The CBOE VIX index, which measures market volatility, showed signs that there is increasing trepidation among equity investors. The so-called “fear index” had been trending down until the last week of the month, but ended July up +6.9%, approaching a reading of 17.

International

World markets, which had been very broadly positive in June, could not keep up the momentum in July. In Europe, Germany’s DAX lost -1.7% in June, while Britain’s FTSE 100 fell -2.2%. In Asia, Shanghai’s SSE Composite dropped -4.5%, Japan’s Nikkei 225 -0.9%, and Hong Kong’s Hang Seng -3.4%.

Central Banks

For the first time since the Great Recession, the Federal Reserve cut its target Fed Funds rate 25 bps to a 2%-2.25% range. This was greeted by a mixed reaction in the financial services industry. The economy is already creating jobs and generating just enough inflation to stimulate reinvestment, which would indicate a rate hike might be in order if, indeed, any action need be taken. Still, this historically long-running expansion is showing signs of slowing and, even during the cycle of the 1990s, the Fed cut rates to a positive effect.

Commodities

West Texas Intermediate crude settled at $58.58 per barrel, up a mere +0.2%, despite a turbulent July reacting to news that Mideast oil exports could be disrupted.

Gold gained only +0.9% to $1,426 per ounce in July. As this newsletter is being written, though, trade tensions have escalated and August is looking sharply positive for the precious metal.

The British pound is sinking fast on no-deal Brexit fears and it is taking the euro with it. Against the dollar, they settled down -4.2% and -2.6% respectively at the end of July. The Japanese yen, which had up to now been appreciating against the greenback, traded -0.8% lower.

Bitcoin settled into a trading range. It does that sometimes. After three months of mid-double-digit gains, the bellwether cryptocurrency closed at $10,053, -7.8% lower for July.

Is Your Card Up To Date?

Is your credit card about to expire? Have you recently received a new card? It’s easy to update your CREDIT CARD information. Just call us at 717-569-8162, or go to the Update Credit Card Information section under the Member’s Tab.

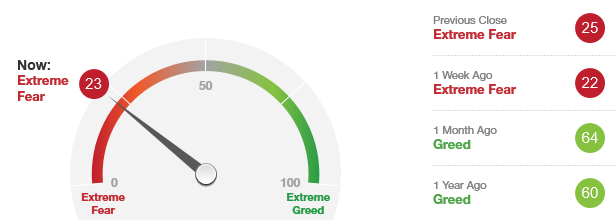

Fear & Greed Index

As of 8/12/19.

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

IPOs: Not just for high rollers

There sure have been a lot of big-name initial public offerings (IPOs) so far this year, and a lot more in the pipeline.

Already we’ve seen Zoom, Slack, Beyond Meat, Chewy, Fiverr, Pinterest and both Uber and Lyft. Still on deck are AirBNB, Postmates, Robinhood and WeWork parent The We Company.

Traditionally, though, retail investors have been unable to participate in IPOs. The big winners were investors affiliated with the underwriting banks that sell the initial shares.

Recent innovations in both regulations and how the financial services industry responded to them, though, now make IPO investment possible for the retail investor.

Think twice

Just because you can do something, though, doesn’t mean you should. Many investment advisors, when presented with a client interested in IPOs, suggest waiting a few months to avoid the initial volatility. This might limit the upside, but it gives the investor a chance to actually get a peek at company earnings.

Still, we can’t avoid the subject. There are a lot of IPOs being floated now. There were 70 in the first half of this year, so we’re on a pace to exceed the 134 debuting in 2018, which eclipsed the 107 the year before.

What this suggests is an appetite – presumably among both issuers and investors – for more of these. The underwriters are nowhere near capacity. So far this millennium, barely 2,000 IPOs hit Wall Street. From 1990 through 2000 – a period that’s only about half as long – there more than double that number.

In 1996 alone, there were 677 IPOs including Yahoo, which Business Insider once called one of “the 11 greatest IPOs of all time”. It also saw the debut of Cymer, a semiconductor equipment maker that is still publicly traded and returned ample value to its Day 1 investors. Ingram Micro was also part of the Class of ’96 and thrived for 20 years before agreeing to be acquired.

But it also included Remec, a onetime wireless communications equipment maker that was eventually liquidated; a court-appointed receiver now runs its website. Then there was PointCast, a dot-com that declined to take News Corp’s half-billion-dollar offer for a screen saver and ended up going nowhere. Lest we forget, 1996 also brought us InVision Technologies, a security screening device maker that ran afoul of the Foreign Corrupt Practices Act.

So give the following menu of ideas a read, but please think about it – and talk about it – before you act.

Public options

Let’s start with the caveat that IPO investing can be risky – it is day-trading in its undiluted form: taking shares that had no market value when you woke up this morning and flipping them before your kid’s soccer game at a price greater than the issuer might ever reach again. So absolutely talk to a financial professional before dipping your toe into this particular pond.

That said, here are a few potential paths to buying into new companies.

Non-traditional underwriters. For its IPO, Intercontinental Exchange, the parent company of the New York Stock Exchange, picked Etrade as an underwriter. That’s the same Etrade that helped bring Facebook public. Other small-scale underwriters include Keefe Bruyette Woods, Allen & Company, Canaccord Genuity and Northland Securities. If you’re what the Securities Act of 1933 defines as a “qualified investor” – and if you make more than $200,000 per year from all sources, you quite possibly do – opening accounts with non-traditional underwriters might be the best pathway for you.

IPO funds. Many exchange-traded funds are owned by institutions that underwrite IPOs or are otherwise toward the front of the line when it comes to participating in them. Some of these specialize in using their parent firm’s clout to give retail investors a chance to get in.

Direct listing. In a direct listing, a company lists on a stock exchange but doesn’t actually sell shares. Instead, current equity holders – that is, the executives, vested employees and early-round venture capitalists – can then sell their shares on the exchange. This is how Spotify and Slack launched.

Regulation A. Regulation A of the Jumpstart Our Business Startups Act of 2012 allows for startups to do a light version of an IPO, providing that they’re seeking to raise less than $50 million. This path gained the market’s respect in August 2017 when Chicken Soup for the Soul Entertainment turned a $30 million Reg A raise into a stock trading on Nasdaq as CSSE.

Equity crowdfunding. Equity in issuing companies – usually going the Reg A route – can be purchased away from the exchanges through such online platforms as AngelList, CircleUp and Fundable. This is the next generation of IPO-focused exchange-traded funds. If you find ETFs more comforting, they are still an available option.

Investing in companies with IPO stakes. Every innovation-heavy enterprise has a “Ventures” subsidiary that finds and nurtures startups that they hope will transform the business. SoftBank, the exemplar of this dynamic, started out as an electronics parts retailer in Japan, then invested in Vodafone and Sprint, which caused it to morph into a telecom. Then it bought into Alibaba, Uber and WeWork and essentially became a merchant bank. It now backs DoorDash, Wag and Flipkart among others. But Salesforce, Google, Tesla and other brainpower nodes are all playing the same game. If you want to invest in the tech these companies are excited about, you could do so indirectly by buying their stock. Of course, that means you’re primarily investing in their core businesses, so you’ll want to be sure you’re comfortable with that.

Directed shares. IPO issuers sometimes allocate shares to "friends" of the company. The trick here is to be intimately involved with the issuer while it’s still pre-IPO. So you would need to be of some perceived value to the founding team. This isn’t an option for passive financial investors, but we’re just throwing it out there.

Weigh the risks

The two decades since the dot-com boom and bust have seen the advent of many policy initiatives that have changed the IPO landscape. The main reason the JOBS Act was considered necessary is that, in 2002, the Sarbanes-Oxley Act (SOX) overreached and quashed small firms’ prospects of going public. In an effort to rein in the excesses of the 1990s equity markets, SOX placed an excessive financial burden on publicly traded companies and, despite the JOBS Act, IPO volume for small firms remains far below historical norms.

The passage of time has also seen changes in the business climate. Established companies with strategic interests in innovative young firms are offering startups enough cash that many are skipping the IPO road shows entirely. In 1991, around 90% of venture capital exits went to the IPO market and the remainder were purchased through mergers-and-acquisitions deals. By 2001, these proportions were reversed, and to this day M&A has maintained that position.

This would tend to depress supply of IPO issuances while demand remains strong, which in turn suggests that today’s Day One investors might be paying a premium for the privilege of being first in line.

Also, consider the age of the present expansion. Nobody wants to be the last one to leave the party. It’s telling that there were 380 IPOs in 2000, but only 79 the following year. There were 159 in 2007, and only 21 the year after that. Depending on how much room for growth you believe is left in this economic cycle, an IPO might not be a suitable investment.

So, while there are lots of ways to get in the ground floor of new stock issuances, maybe you ought to speak with a financial professional first.

Chris

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.