Market Overview

This month's models have been posted. There are CHANGES IN ALL THE MODELS.

Real estate markets face the mortgage-rate disconnect

It used to be so simple and predictable: The economy grows. People prosper. They buy homes. Housing prices spike and inflation works its way through the economy. The Federal Reserve raises the fed funds rate – the rate big banks charge each other for overnight holds – thus the banks have to raise mortgage rates. More expensive mortgages result in less demand for homes, and the economy slows down.

That’s the way it has always worked, and it continued to do so for the first six months of this year. But that’s not what’s happening now.

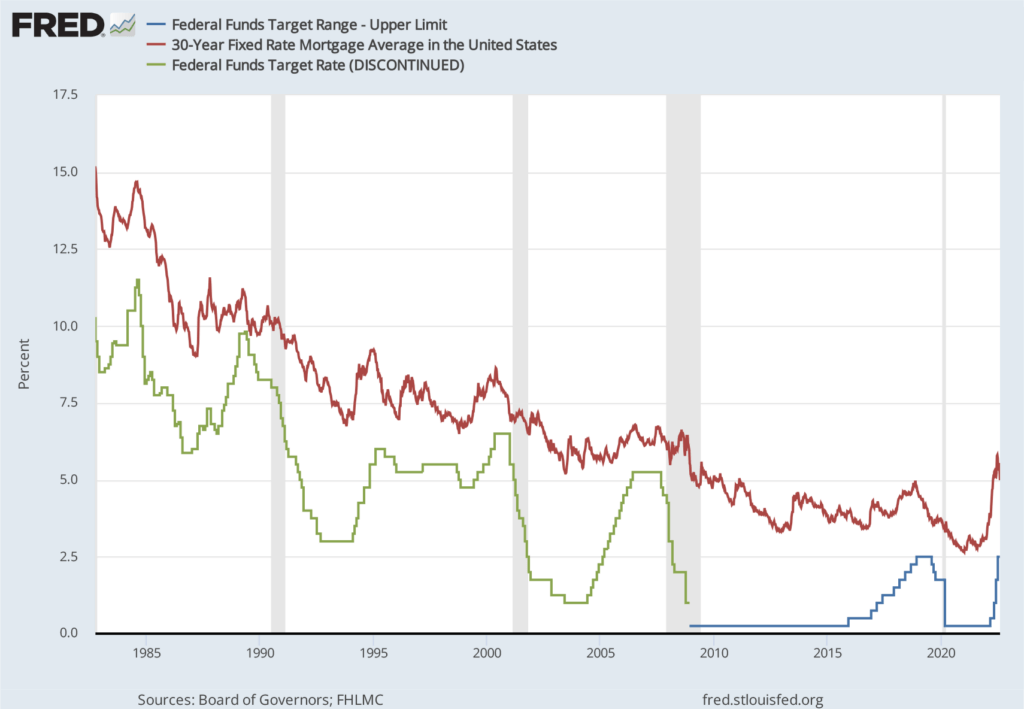

On June 16, the central bank increased the fed funds target range by 0.75 percentage points, the first time it raised it that aggressively in decades. Mortgage rates went up proportionately, as expected, peaking the following week at 5.81%. But then things got weird. At last check, the average 30-year fixed mortgage rate had dropped back below 5% -- even in the wake of another 0.75 percentage-point increase in the fed funds target rate. Is there something wrong with the law of supply and demand? What’s going on here?

The question isn’t why are mortgage rates so high – it’s why aren’t they higher? Credit: Federal Reserve

Starting at zero

The law of supply and demand still holds, by the way. If the past couple years have taught us anything, it’s that economic laws all include the stipulation, “other things being equal”. Externalities – pandemics, wars, disasters or even an unpredicted change in cultural norms – can disrupt everything.

It also bears mentioning that, when it comes to interest rates, we’ve been in a sweet spot for quite some time. In the early 1980s, the average mortgage rate rose to almost 20%, which you’d expect with a fed funds target rate exceeding 10% at that time. But then the same thing happened: The fed funds rate went higher, to 12%, but mortgage rates fell, to below 15%.

Actually, this meant that the Fed’s monetary policy was working. The inflation bubble had burst. People could more readily afford homes again and banks competed for the lending business. Both the fed funds rate and mortgage rates trended downward for decades. By the time of the Great Recession, the fed funds target range was lowered to 0%-0.25% and mortgages could be had for under 5%. The range stayed at rock bottom for seven years, and mortgage rates drifted down below 4%. The Fed then increased its target incrementally from 2016 until the start of the pandemic, with little effect on the mortgage market. In response to the shutdown of the economy, fed funds returned to the 0%-0.25% target range and suddenly mortgage rates dove toward 2.5%.

So even if a 5% fixed-rate mortgage sounds pricey, it’s still pretty cheap historically speaking. Ditto for the fed funds rate. But there’s always going to be a lag. Growing families might defer buying a home if the mortgage rate suddenly returns to early-1980s levels, but are less likely to when rates inch up by a percentage point or two. They’ll take on the extra cost now and refinance later when rates go down again. Interest rates tend to be the least of their worries, so they’ll keep buying houses. Home prices often soar because school districts, plot sizes and proximity to places of interest are unique and non-fungible – but you can get a mortgage anywhere. Financial institutions still have to compete for the prospective homeowner’s business and the best way to do that is to offer a loan for an interest rate just a shade below the next lender’s, then hope to make up in market share what they lose in margin.

Not just your castle … your office

And there is no lack of a market for real estate these days.

The average home price at the end of the Great Recession was $214,300, according to the U.S. Census Bureau. It rose steadily until 2017, when it fell into a three-year rut with a price around $325,000. As of mid-2022, though, it had skyrocketed to $440,300. So what changed?

The pandemic was a major contributor to the recent spike in home prices. We realized that office space was optional, but a place to live comfortably wasn’t.

The lockdown didn’t so much create demand as pull it forward in time. Suddenly, everyone felt a need to make that home purchase they were deferring until they were more financially stable. They still had jobs – and they were all of a sudden getting raises. They were also getting government stimulus checks while saving a not-insignificant amount of money by not commuting. It was a perfect recipe for a spike in home prices, even if supply was sufficient – which it wasn’t.

Real estate developers couldn’t keep pace with demand, which helped to buoy prices.

So we find ourselves in a situation where, even if we entirely refocused our economy on homebuilding, it would be years before we would have all the units that are needed. And we’re likely to sell out of single-family houses and luxury penthouses before we make a dent in the rowhouses, duplexes and garden apartments needed for middle- and working-class families.

When will home prices fall?

Of course, home prices can’t rise forever. Frankly, the most obvious way for housing costs to drop is if unemployment spikes, which would likely trigger a recession. That wouldn’t be good news and would mean that we’d be a nation of cash-poor, house-rich people with four-bedroom Colonials and no jobs. Those of us who remember 2009 do not want to go back to that.

As discussed below, we might be in a recession or slipping into one already. If it turns out to be a mild one, the Fed could brag it had gotten the formula right and had nailed the elusive “soft landing”.

But it’s not that simple. Just because we’ve been getting some good news lately on the employment front doesn’t mean a serious recession isn’t still possible. As of this writing, we are experiencing a yield curve inversion – that is, short-term notes offer higher interest rates than longer-term bonds. Most of the time, that is not a good thing as it means that the longer investors commit their money, the less money they make on the deal. When that happens, investors tend to scramble for the quick buck rather than invest for the future, which hurts lending and development. Inverted yield curves are indicators – albeit imperfect indicators – that a serious economic contraction might be coming.

So, given all that, should you be buying a house now? Should you be investing in real estate investment trusts? If you’re a qualified investor, maybe you should be looking at collateralized mortgage debt – or maybe you should be running from it as fast as you can. Nobody has a crystal ball, but a trusted financial advisor could help you navigate this economy and the markets – and advise you how to hedge your bets when the signals are mixed.