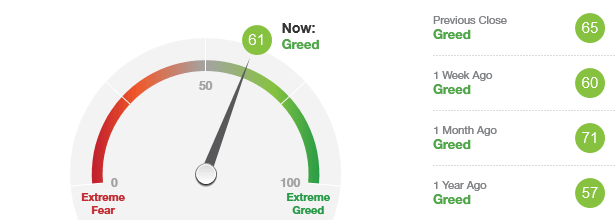

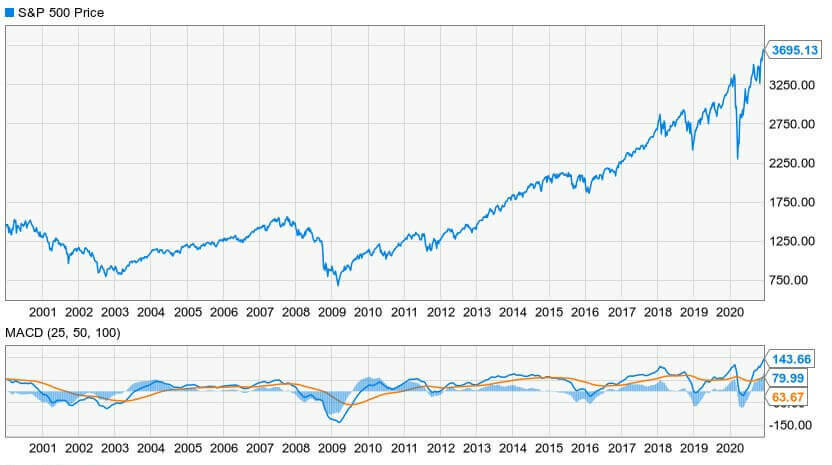

Market Overview

This month's models are posted.

Personnel is policy

It can be presumed at this point that on January 20, 2021, Joe Biden will be in office. Elections, no matter how well-executed and no matter how flawed, come to a conclusion at some point.

The winner gets to pick the people who will execute the agenda. It is these appointments that, more than anything else, drive that agenda. As of this writing, much of the Biden team is still being vetted. The economic crew has been named, though, and this provides some clarity surrounding America’s financial future.

\ ‘Who’s who’…

Say what you will about the Trump economics team, but you’ve heard of them before. Gary Cohn, Trump’s Day One National Economic Council director, was president of Goldman Sachs and his replacement, Larry Kudlow, came right off the set of CNBC’s Squawk Box. Steven Mnuchin, the full-term Treasury secretary, was a high-profile Goldman alumnus who went Hollywood; as an executive producer, he got his name in front of some of the biggest blockbusters of the 2010s.

In this regard, the Trump administration was not unique. Barack Obama tapped Timothy Geithner – the Federal Reserve’s fireman who doused the 2008 financial crisis – as Treasury secretary, as well as Lawrence Summers – Bill Clinton’s Treasury secretary – as NEC director. While NEC director is a fairly new position – created by Clinton – past presidents going back to George Washington have also named luminaries to the top Treasury post.

So Biden’s announcement that he will nominate Janet Yellen to serve as his Secretary of the Treasury is consistent with history. The former chair of both the Fed and Clinton’s Council of Economic Advisors faces an easy Senate approval process.

But the rest of the economic team is largely unknown to anybody without an Inside Baseball knowledge of macroeconomic policy.

Mnuchin’s Hollywood past or Yellen’s Washington Future? Credit: Warner Bros.

… ‘Who’s that?’

The designated core team, announced December 1, is comprised of:

- Yellen

- Office of Management and Budget Director: Neera Tanden

- Deputy Treasury Secretary: Wally Adeyemo

- Council of Economic Advisers Chair: Cecilia Rouse

- CEA Member: Jared Bernstein

- CEA Member: Heather Boushey

- NEC Director: Brian Deese

They never heard of you either. But let’s quickly look at what the job descriptions are for the roles they’ve been named to.

The Treasury secretary formulates economic and tax policy while overseeing a department of 87,000 employees which includes the U.S. Mint, the Internal Revenue Service and the Social Security and Medicare trust funds. The OMB director is the federal budget’s primary architect, whose pencil and eraser determine how much each agency gets to spend on what. The CEA is the key economic research arm of the administration, a relatively apolitical facts-and-figures operation. That’s distinct from the NEC, which is the policy shop; the NEC director is the top economist working inside the White House.

Tanden is perhaps the most controversial choice. She is the most partisan Democrat on the list. That said, she’s nowhere near the farthest left. An adherent to the moderate wing of the blue team, she is a lifelong Clinton loyalist – first Bill, then Hillary – and a John Podesta protege. According to the New York Times, she once slugged a Bernie Sanders proponent, a charge she denies: “I didn’t slug him, I pushed him.”

She also has a tendency to weaponize Twitter. Some of her microblogs target Republican office holders and office seekers by name while others call out the entire GOP down to its base. While she has since deleted many of these – after all, Tanden will likely need some Republican support in the Senate for her confirmation– CNN has catalogued many of them. After four years, it’ll be interesting to see how many Trump allies will take exception to something someone tweeted.

Despite still being in his 30s, Adeyemo is an old hand on the policy side, as opposed to the politics side. While he might be a step to the left of Tanden, he pursued such mainstream goals of the Obama administration as the establishment of the Consumer Financial Protection Bureau and negotiation of the Trans-Pacific Partnership. Under Trump, the first was deemphasized and the second abandoned.

Yellen, Tanden and Adeyemo must be approved by the Senate before being sworn in. The CEA and NSC designees do not.

Rouse was a CEA member under Obama, so this nomination could be seen as a promotion along an existing career path. A professor and dean at Princeton University, her academic interest is in labor economics broadly, but her specialization has been in how to pay for college. Bernstein has been Biden’s in-house economist for years and is more focused on the erosion of the middle class; while solidly on the Democratic side of the aisle, his trade policies are not that far removed from the Trump team’s. Joined at the political hip with the firebrand Tanden, the more empirically minded Boushey is also a policy centrist; her focus is on the role of women in the economy.

Deese is another Obama alumnus, who worked initially in leadership roles in OMB. He eventually rose to the rank of senior advisor to the president. When you consider that his two successors Jared Kushner and Stephen Miller – as well as Kudlow, the man he’ll succeed at NSC -- are so high-profile, it says something that Deese has thus far avoided the spotlight.

What they’ll do

Before we get into what’s of the greatest importance to each of these players, let’s understand what’s of greatest importance to America at this moment: recovery from the Covid-19 crisis. It’s a false dichotomy to say we can solve either the medical problem or the economic problem; clearly, they both need addressing.

With the imminent arrival of vaccines, the much-improved ability to treat active cases and the election of a president who is seen as a proponent of a centralized approach to fighting the pandemic, the medical end is looking hopeful. Still, some dismiss Biden’s mask protocol as “virtue signaling” while others call it “setting a good example.”

So, what does the economy need? First, it needs more economic stimulus. Last week, Congressional Democrats and Senate Republicans seemed to have reached an understanding on a sub-trillion-dollar deal, the details of which are still entirely murky as of this writing. Senate leadership can now say it did something besides obstruct and keep a lid on the cost. House leadership can settle for nowhere-near-half-a-loaf – barely enough slices for a club sandwich, really – with the expectation that a Democratic president will help them pass a larger measure early in the coming year.

Democrats also have a not unreasonable hope of securing a Senate majority, which would make life much easier for them. While the two Georgia runoffs both feature GOP incumbents, these senators face solid opposition on January 5. It’s going to be a matter of turnout, and the wind might be at the Democrats’ back on the day. If they win both seats, the Senate will be comprised of 50 members in each caucus, so newly elected Vice President Kamala Harris would decide all tie-breakers, essentially handing the chamber to her party.

If that happens, then the Democrats will be able to run the table with their policy preferences. Coronavirus relief will be doled out as if deficits don’t matter – and there are some on both sides of the aisle who’ll tell you they really don’t.

These moves will be seconded by an even more expansionary monetary policy than the Fed is currently offering. There’s really very little daylight between former Fed chair Yellen’s thinking and that of her successor, Jay Powell. Don’t be surprised if the Fed funds target rate actually goes negative – essentially paying businesses to borrow money so they can stay afloat and perhaps even expand.

Can’t spend what you don’t have

Where there will be a massive change will be in tax policy. According to the center-right Tax Foundation, the Biden administration would:

- Raise taxes on households making more than $400,000, getting much of it from capital gains and some of it from increasing transfer payments to Social Security and Medicare;

- Increase corporate income tax from a top rate of 21% to one of 28% (it was 35% prior to Trump’s tax reform package);

- Impose higher taxes on income repatriated from foreign subsidiaries; and

- Temporarily increase earned income, child-and-dependent-care and other tax credits available to low- and middle-income filers.

While the foundation’s model shows that these moves would benefit 80% of the public immediately, it would have a long-term deleterious effect on almost all households. Still, it was not able to examine the impacts of the entire Biden tax plan due to a lack of specifics on some points. First and foremost, it remains to be seen what will change under the Affordable Care Act, for which the courts are as much a wild card as the legislative process. Will the individual mandate penalty be re-established? Will Biden be able to push through a public option? And, if Obamacare is buttressed in this manner, will it mean higher taxes? The most important – though least frequently asked – question is: If taxes go up to pay for Obamacare, will insurance premiums go down enough to offset?

Trees, trade and transit

While the potential return of Obamacare might make conservatives anxious, they need not concern themselves with a “Green New Deal.” It’s a pipe dream put forth by some very junior members of Congress and will have few friends in the Biden White House. That said, expect any tax plan that comes out of Tanden’s office to renew credits for energy efficiency investment and electric vehicle purchases.

On the global front, it’s telling that Biden has yet to name the new U.S. Trade Representative, a Cabinet-level post. At the moment, Adeyemo is the only designee with hands-on trade experience and he’s all about multilateral agreements. Bernstein, though, isn’t overly fond of them and he has Biden’s ear. You can expect some heated discussions about trade around the West Wing. Having this kind of discussion, though, might be more productive ultimately than Trump’s protectionist reflex or Obama’s and Clinton’s penchants for opening up all markets everywhere for everyone. A nuanced approach – in which we align with allies to call out China and other bad actors on specific grievances, but ultimately find a way of exchanging goods and services – might be a welcome change.

Another welcome change would be one in which both parties overcome their rivalries and do something non-controversial that’s good for the entire country’s economic growth. We refer of course to infrastructure. The last time that happened was in 2015, when Congress voted on the Fixing America’s Surface Transportation Act, a measure to spend $305 billion on … well very little. It was basically a 1,300-page mash note to Boeing, reauthorizing the Export-Import Bank. In addition to the FAST Act, Obama more famously signed the American Recovery and Reinvestment Act, known at the time as “the stimulus.” While it scattered $800 billion in spending throughout the Great Recession, only about $100 billion of that had anything to do with hard infrastructure. The last time there was a meaningful bill addressing the issue was in 2005, when Bush signed the so-called SAFE-TEA Act.

Funny thing about Obama’s stimulus and Bush’s SAFE-TEA acts: They were both achieved during moments when one party controlled both houses of Congress as well as the White House. Although they had legitimate bipartisan backing, this was irrelevant. We could have had infrastructure bills before and since, and yet we haven’t. The next time that a divided government passes what should be a no-brainer of a highway or mass transit bill will be the first time in memory.

Stocking stuffers

To round out some Democratic wish-list items, Rouse is likely to be a strenuous advocate for student loan forgiveness and increased funding for public education. That said, she isn’t exactly in a power position. Adeyemo, for his part, will probably call for more funding for financial regulators and consumer protection agencies, but he’s just going to be the No. 2 at Treasury. His boss Yellen will likely be all about increasing expenditures to stimulate the economy, with the goal of decreasing unemployment and raising the workforce participation rate. Raising expenditures means raising revenues too. While some of that is going to come from tax increases on the wealthy, it’s also going to increase borrowing. The case can be made that, with interest rates this low, it would be malpractice for the government not to borrow every dollar it can. Still, we can be sure that the Biden administration – like those of both Democratic and Republican presidents for generations – will continue to set deficit and debt records.

So how should you move money around your portfolio in response to the changing of the guard in Washington? What difference would it make if the Georgia Senate contests tilted one way or the other? These are difficult questions. Maybe you should talk to a qualified financial professional before committing to any course of action.