Market Overview

This month's models are now posted. There are NO CHANGES in the models. The rest of the newsletter should be published by mid-month.

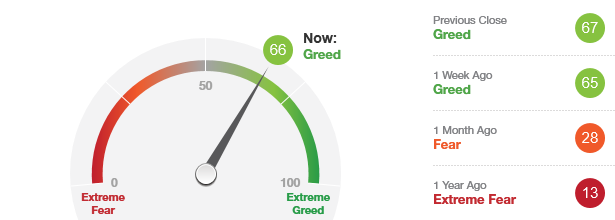

As stated in last month’s Newsletter, the Bull Bear Oscillator (BBO) turned bearish and remains in bearish territory as we begin February. The models will hold a defensive position of bonds and cash until we get an “All’s Clear” on the BBO.

These are very volatile and dangerous markets for investors. Volatility is a friend to traders but an adversary to investors. Investors prefer smooth ups and downs, and this is nothing of the sort. Consider the recent headlines - December 31st 2018: Dow, S&P 500 post worst December since 1931, as Nasdaq has worst on record1 and this one from Feb 1, 2019: U.S. Stocks Have Their Best January in 30 Years.2 In the words of Warren Buffett, “The stock market is a device to transfer money from the impatient to the patient.” We know it can be frustrating being allocated to a defensive position when the market continues to march higher. There will be less volatile and safer times to move back into the market but for now we will play it safe.

1 FoxBusiness.com December 31, 2018

2 Furtune.com February 1, 2019

Ensuring you’re sure about your insurance

Utility company stocks, as you’re probably aware, are considered among Wall Street’s safest bets. In return for agreeing to be highly regulated to the point where they’re practically in the public sector, the issuers are granted monopolies from the states, which virtually guarantee them a profit. It’s a small profit, but steady one. If you’re the CEO of a utility company that has to file for bankruptcy, you’d have to be either flagrantly incompetent or have the lousiest luck on the planet.

And bad luck sometimes happens. For example, think about what occurred in California during the most recent fire season, when the Camp Fire claimed 86 lives before it was contained. Along the way it consumed more square miles than Chicago. There are almost 20,000 homes, businesses and other structures which are no longer standing because of the Camp Fire. Three people are still missing.

It was the deadliest and most destructive fire in California history. Smoke plumes were reportedly seen as far away as New York.

Nobody knows – for certain – yet – what caused it. The notorious, gale-force Jarbo winds were blowing downslope, and the National Weather Service had issued a red flag warning for most of the surrounding area. A years-long drought was in effect, including seven recent months of particularly dry weather. A fire was, if not inevitable, at least likely.

It was an interruption in Pacific Gas & Electric (PG&E) service that was the first hint an ominous fire had started. And it was a PG&E employee who first spotted the fire; its reported location was directly under PG&E power lines.

While it’s far from conclusive that PG&E was at fault, this was not the first time that PG&E has garnered suspicion. Other recent fires had been blamed on the utility. But PG&E has had a target on its back ever since a section of its San Bruno pipeline ruptured in 2010, resulting in an explosion that sent a 1,000-foot-high wall of fire into the sky, which claimed at least eight lives. PG&E is still under probation for those deaths.

So, in anticipation of civil and criminal penalties, PG&E filed for bankruptcy protection after the Camp Fire incident. This is a rare move for a utility, as they are virtually insulated from the need to take such actions, in part because the executives who run utility companies tend to be risk-averse.

California’s Camp Fire, November 2018. Credit: Forest Service Photography

High above, but not above it all

Commercial airline pilots also tend to be risk-averse, especially when it comes to doing their job. Safety is given the highest of priorities in their training, and for good reason – the traveling public is putting their absolute trust in them to do their job with care and precision. And, just like reaching any other destination, reaching retirement has its share of exposures.

First, there are risks that could keep you from physically reaching that target. Let’s start by assuming that you have health insurance, and that you get all the physicals, wellness visits, checkups, and tests – no matter how unpleasant – that your job mandates and your insurer advises. Beyond that, you may have long-term care insurance in case an accident or illness causes you to require assistance in what were normal daily activities before.

But what if the worst should happen? If you were to die, would your survivors have the wherewithal to carry on? Nobody wants to talk about life insurance. We don’t want to talk about life insurance. But life insurance – all insurance, really – is as much an integral part of your financial portfolio as your 401(k). And it’s just as complicated to parse. Just like you might want to seek out professional advice about adjusting your blend of stocks and bonds over time, you might want to hear a considered opinion about choosing between term, universal, variable and other categories of life insurance.

Let’s assume the best and most likely scenario—you are happily on your way to a healthy retirement. But are you prepared for a potential series of unfortunate events? Like extensive damage to your home from a flood or a fire, or a litany of other destructive occurrences.

If you own a home, your mortgage lender almost certainly has required that you take out an insurance policy to protect your home, and their collateral interest in it – but do you know what exactly that policy covers? You don’t want to find out the hard way after a water pipe bursts, or a mold infestation is discovered, or a passerby is bitten by your dog. And if you’re not sure if your policy covers damage due to flooding, you should probably assume that it doesn’t.

The same goes for your car. To be street-legal, you probably need liability insurance against bodily injury and property damage. But what about collision coverage? Comprehensive coverage? Uninsured motorist coverage? All of these are available, but are they warranted in your case? Are there conditions under which the insurer can avoid being compelled to make payment for loss, such as if speed limits were violated or blood-alcohol levels exceeded the legal limit? You probably want these questions answered, especially when all it costs you is a few minutes of your time and attention. Better that and fine-tuning your coverages, than being under-insured and incurring what could be a significant hit to your retirement portfolio.

Once you’re assured that the coverage you have matches your needs, then you can start bargain-hunting for the best deal. Most insurers will give you a break if you bundle your policies. Maybe you’re comfortable with higher deductibles, if so, those will lower your premiums. To be sure, there is such thing as being over-insured, although that’s not most people’s problem. There are lots of helpful rules of thumb out there about how much you should spend on insurance given your income, the market value of your home and so on. Many of them are proffered by people in the insurance industry, but they still can make sense. Consider having a talk with a financial professional with whom you have an ongoing working relationship about what types of insurance and coverage amounts best fit your needs.

What’s the real threat level?

As devastating as the Camp Fire was, it really wasn’t the worst thing that happened in 2018, a year in which events in Syria, Yemen and elsewhere caused the world to pause. The Camp Fire was just the costliest natural disaster of the year.

No matter where or how you live, there will always be the presence of at least some risk. That’s just life in the world we live in. And that risk can be as varied and unpredictable as this sampling of the destruction that occurred in 2018.