Technology is changing. And, while many of us still own shoes older than our first Web browser, the act of reading text on a computer is outmoded as a platform for communication, according to many (i.e., our kids).

And if you still own a landline phone and a cable TV box, well bless your heart. The world is leaving us cable viewers in the dust as it finds newer, more efficient ways to entertain and inform the public. Programming can now be viewed on desktop computers, laptops, tablets and phones, as well as built-for-purpose TV screens.

An entirely new industry emerged while we were watching Turner Classic Movies, and it has become such a huge business that any investor and any investment newsletter needs to understand this brave, new world of subscription streaming services.

“In 2019, we each spent $640 on digital subscriptions like streaming video and music services, cloud storage, dating apps and online productivity tools,” according to the New York Times. “That was up about 7 percent from $598 in 2017. We increased our spending the most last year on streaming TV services, paying $170 to subscribe to the likes of Netflix, Hulu and new entrants like Disney Plus and Apple TV Plus. While that was far cheaper than most traditional cable TV packages, which cost roughly $1,200 a year, it was up 30 percent from the $130 we spent on streaming TV services in 2017.”

Original Netflix programming from 2017 won the Academy Award for Best Documentary

Cast of characters

You’ve probably heard of the “FAANG” stocks, the bellwethers of the consumer discretionary space in the technology sector: Facebook, Amazon, Apple, Netflix and Google. Of those, all but Facebook offers a subscription streaming service.

Amazon connects with 100 million subscribers via Prime Video, with or without the Fire TV Stick device. Apple’s new Apple TV+ -- again, with or without the Apple TV device – is just getting off the ground, but Stephen Spielberg, Jennifer Anniston, Reese Witherspoon, Steve Carell, Samuel L. Jackson, Chris Evans, M. Night Shyamalan and, oh yeah, Oprah Winfrey are all onboard. Netflix is Netflix, the 167 million subscriber-strong company that put the corner video store out of business and is now a fixture at the Oscars. Google, in addition to owning YouTube and along with it the Originals slate of programs, is also moving into the infrastructure business, providing the Chromecast Nexus player, manufacturing routers and breaking into wi-fi provisioning.

With the exception of Netflix, though, none of these massive tech conglomerates focuses entirely on content. But there are certainly others who do.

To start with, there are the legacy companies who remember when content was called “programming”.

The Walt Disney Company actually has two subscription streaming services. Hulu offers a way around cable subscriptions by offering network TV shows on-demand or, more recently, live. Just this past year, Disney+ was launched to bring Disney’s productions and its franchises – Marvel, Star Wars, Pixar, 20th Century Fox Studios – under one umbrella. WarnerMedia offers HBO Go to those who still subscribe to cable and HBO Now to those who have already cut the cord; it also owns the DC Universe superhero channel. ViacomCBS declined to participate in Hulu, so CBS All Access serves as a standalone stream for the Tiffany Network’s fare; meantime, top executives are still trying to hash out how to best stream their newly acquired Paramount Pictures catalog.

There are others, but they tend to fill niches related to sports, genres, languages.

Over the top

Then there’s the whole world of over-the-top media services. The most prominently marked of these is Sling TV, Dish Network’s attempt to remain relevant. Sling is, by all accounts, a technologically elegant means to deliver network TV via internet. Still, it doesn’t offer all the channels Hulu does because broadcasters are concerned about how cable providers might react to their entering a deal with Dish, which is in the satellite TV business.

Sling’s service is not to be confused with digital players. We already mentioned Amazon’s, Apple’s and Google’s appliances, but the discussion isn’t complete without mentioning Roku. This company sells a device that serves as the “brain” of a TV, which allows you access to a selection of decidedly second-rate channels and local news outlets.

Hardware tends to be replaced over time by software, though, so Roku might not be around long. One exception to that rule might be game consoles, at least for now. At some point, you’ll be able to wear your virtual reality console like a hat and gloves, or maybe even have it implanted. But for now, Sony Playstation 4, Microsoft Xbox One and Nintendo Switch aren’t going anywhere. In fact, they’re all pretty much as they were in 2016. In addition to being used for their intended purpose, though, they also work as digital players. They can all receive Amazon Prime Video, Hulu, Netflix, YouTube and much more.

We interrupt this program

So why are we giving you so much detail on the state of entertainment? It’s about what stocks or sectors are likely to be trendy, and thus may be likely to outperform the market. This diversity of delivery systems – in terms of both origination and delivery – can’t last forever. At some point, the economics are going to require consolidation. Some production companies will remain while others are absorbed or disappear entirely. The same will happen with the networks and the hardware that supplies them.

While we’re confident in that educated guess – it’s just part of every industry’s path to maturity – it is still too early to pick winners and losers with any confidence. Through your qualified retirement plan, you’re probably already invested in several of the companies mentioned above. And it might not be the companies you think, or that you want. Talk to a qualified financial advisor to help you fine-tune your exposure and remember, today you can’t just turn the dial.

Is an In Service Rollover Right for You?

Federal law and your FedEx 401k plan provisions allow you to transfer a sizable portion of your 401k over to an IRA in your name. An In-Service Rollover (ISR) allows you to get more control of your hard-earned money, and in many cases you can upgrade the investments available to you. But it’s not right for everyone.

Call us today at 1-800-301-8486, or email us at emailinfo@smithanglin.com, to learn more about the benefits of an In-Service Rollover, and whether doing one is right for you.

Provided by Smith Anglin, a 2018 Financial Times 300 Top Registered Investment Adviser Firm.

The Commerce Department’s first estimate of fourth-quarter GDP indicated that it increased at an annual rate of +2.1%, matching the previous quarter’s growth. While that was above expectations, it showed a slowdown in personal consumption. It also suggests that the second half of 2019 was distinctly less vibrant than the first half, since full-year GDP grew +2.3% last year. And that was slower than 2018’s 2.5% expansion. Still, for a mature economy, growing at a +2.1% to +2.3 clip isn’t bad.

US Stocks

While U.S. equities got 2020 off to a jackrabbit start, they faded toward the end of January. The S&P 500 posted a fractional loss of -0.4% on a total return basis as concerns mounted over the economic impact of China’s containment of the coronavirus.

The CBOE VIX index, which measures market volatility, reflected this abrupt change in direction, and clearly demonstrated investors are spooked. The so-called “fear index” ended January at almost 19, a sudden surge of +36.7%.

International

Europe was even more shaken by the risk of pandemic. Germany’s DAX lost -2.0% in January, all in the month’s last week. Britain’s FTSE 100, meanwhile dropped -3.4%. The denouement of the Brexit drama didn’t seem to effect markets in London.

In Asia, Shanghai’s SSE Composite fell -3.5% before the lunar new year break. Similarly, Hong Kong’s Hang Seng dropped a sobering -7.8% in January. Japan’s Nikkei 225 showed more resilience, giving up only -1.9%.

Central Banks

In related coronavirus-inspired economic news, the Federal Reserve signaled that it is reconsidering its wait-and-see stance on interest rates. Another cut might be coming in 2020. It’s even possible that the world’s major central banks will again work in concert to stimulate the global economy.

Commodities

Oil prices dropped sharply in reaction to the reduced travel stemming from containment of the infection. West Texas crude swooned -15.6% for the month.

Gold, often a “fear trade”, rose +4.3% to end January at $1,588 per ounce.

For the month, the euro and British pound dipped -1.0% and -0.5% against the dollar, respectively, while the Japanese yen gained a marginal +0.2%.

If there’s one thing bitcoin investors love, it’s global chaos. The bellwether cryptocurrency ended January at $9,504, a +32.2% surge. Double-digit moves like this, though, come with the territory for bitcoin.

Trading Restrictions Reminder!

Your 401k plan has trading restrictions, so you must keep track of your buy and sell orders. Not paying attention could leave you locked out of trading.

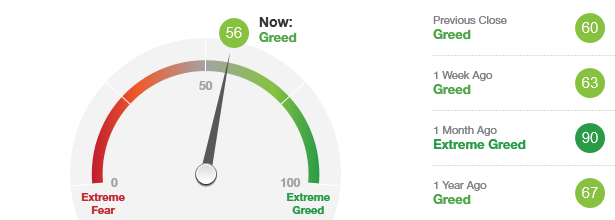

Fear & Greed Index

As of 2/13/2020.

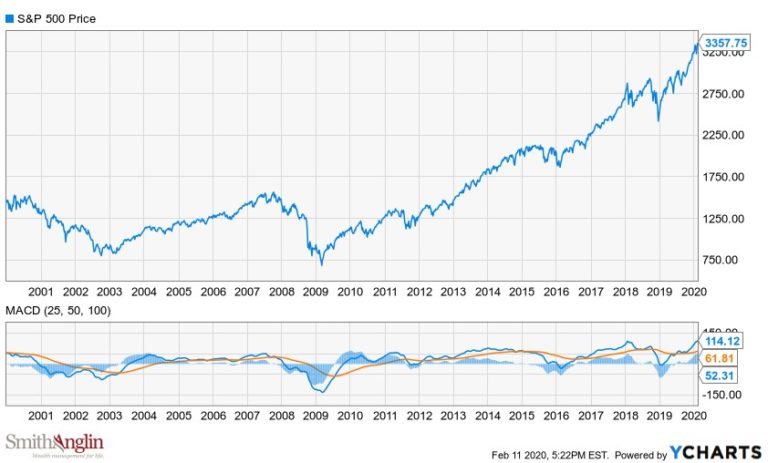

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

Before you retire, retire your debt

Let’s start by saying: Debt itself isn’t a bad thing. If we’re in a period of low interest rates, and we expect our earnings to increase over time, the use of debt can be very helpful. It enables us to buy houses, cars, appliances, furnishings and all the other accoutrements of The Good Life without denying ourselves the pleasure of enjoying them to their fullest extent until we’re too old to really do so.

But debt is a double-edged sword. No, make that a chainsaw, and it can chew up those who mishandle it. A new credit card is not, as some compulsive people seem to believe, the same as a raise in pay. But you don’t have to be a spendthrift to go into debt. Unexpected medical expenses and career interruptions can make those unpaid bills stack up as fast as that annual blur of Thanksgiving, Christmas, New Year’s, Super Sunday, Valentine’s Day, Mother’s Day, Father’s Day, graduations, weddings, summer vacation and back-to-school shopping. And are you still paying off a student loan?

If you’ve reached the point where you’re not taking on any more debt – or have at least slowed your spending to the point where you’re actively paying debt off – then it’s time to strategize how to best free yourself from debt for good.

It’s not that simple

You’re probably thinking, “My credit card charges 14% and my home equity line of credit charges 6%, so I should just attack the Visa first.” And while that’s generally true, there’s more to consider.

A HELOC is essentially a mortgage, secured by the value of your house. That means you need to at least make the minimum payments on it just to make sure you get to keep that house. It’s hard to stay on top of the rest of your capital stack if you have no fixed address. So even though secured debt tends to have lower interest rates than unsecured debt, you need to make sure you keep up payments on the secured debt before you dig out from under the rest.

Another form of secured debt you might have incurred is an auto loan. The good news is that you’re not locked into it for 30 years like a first mortgage. If you want to unload debt, you can usually return the car before it’s fully paid off because the dealership is eager to get it on its used-car lot; you can call them, but odds are they’ll call you first.

If you still need wheels, consider buying a pre-owned vehicle. If it’s only two or three years old and hasn’t been involved in an accident, there’s probably nothing in the least wrong with it. Leasing is another option, and Carlease.com has got a great primer on the topic. Of course, if your car is already close to being paid off, why not wait for the title to come in the mail, then frame it and hang it on your wall? There’s no law that says you have to trade in your ride every four or five years. Consider driving it payment-free until you actually start having mechanical problems with it.

School’s out

Before we talk more about unsecured debts – essentially credit card bills – we need to acknowledge one thing that often gets lost in the noise: You can walk away from them at any time. It means declaring bankruptcy, which is fraught with a whole host of other issues related to your credit score, your ability to take on other debt in the future for any purpose, your self-esteem, and perhaps even your sense of honor. But sometimes you do what you have to do, and that’s why bankruptcy laws exist in the first place.

Student loans, however, cannot be discharged by bankruptcy. Sallie Mae will find you, take you to court and garnish your wages, even if American Express and Mastercard walk away empty-handed.

It’s important to pay those student loans down. And that doesn’t mean just paying the interest. Make sure you’re on some version of the payment plan that includes principal. At that point, it becomes a judgment call how quickly you move on that.

Plastic surgery

What informs that judgment call more than anything else is how much credit card debt you have and your interest expense on those credit cards.

If your student loan rate is lower than your credit card rates, and it typically is, then just make the minimum interest-plus-principal payment while you hack away at paying down the plastic. Otherwise, pay off the student loan first and make the minimum payments on the cards.

The general rule with unsecured debt is: Pay off the bill with the highest interest rate first. That said, a lot of people choose to pay off the smallest bills first. Objectively speaking, this means you’ll end up paying more interest. Subjectively, though, there is a sense of accomplishment to be gained by having one fewer payment to make each month. Take your pick, but understand there is an actual price to be paid for the satisfaction of retiring a lower-rate card ahead of a higher-rate card.

One last resort

It’s best to pay off debt from your income. For some, though, it might not be entirely feasible. There is one other possibility.

No, not payday loans. We’re just going to assume that the readers of this column are smart enough to never go near those.

Rather, you do have investments to tap. If they’re not in a qualified plan and you’re prepared to take the possible capital gains tax hit, then consider cashing out to the extent you need to retire your debts. You might miss out on some upside if this bull market keeps running, but if you’re paying more than 15% interest, you might wonder how realistic it is to project the 15% after-tax return your investments would have to net you over the coming year to break even.

If your money is tied up in qualified retirement plans – employer-sponsored funds or IRAs of any flavor – then it gets a little more complicated to tap those places to pay down debts. Generally, it’s a bad idea to crack open that nest egg. And it’s an even worse idea to do it to cover discretionary consumer purchases such as the ones that might have gotten you into credit card problems. But if there are legitimate hardships, you might be able to get the money out of your retirement account or perhaps borrow against those funds at a lower rate than your creditors are demanding. We wrote about that here a few months ago.

Everyone’s circumstances are unique, so there’s no “one size fits all” answer. If you’re thinking of cashing out from your investments, though, you might want to talk to an expert. A qualified financial professional might not only give you advice on how to do it, they might even give you advice on how to not do it and still remain solvent. And they might even be able to help you put a plan in place to never get overwhelmed by debt again.

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.