Market Overview

This month's models have been posted. There are changes in SOME OF THE MODELS (highlighted in yellow). The rest of the newsletter will be posted by the middle of the month.

Is Uncle Sam a deadbeat?

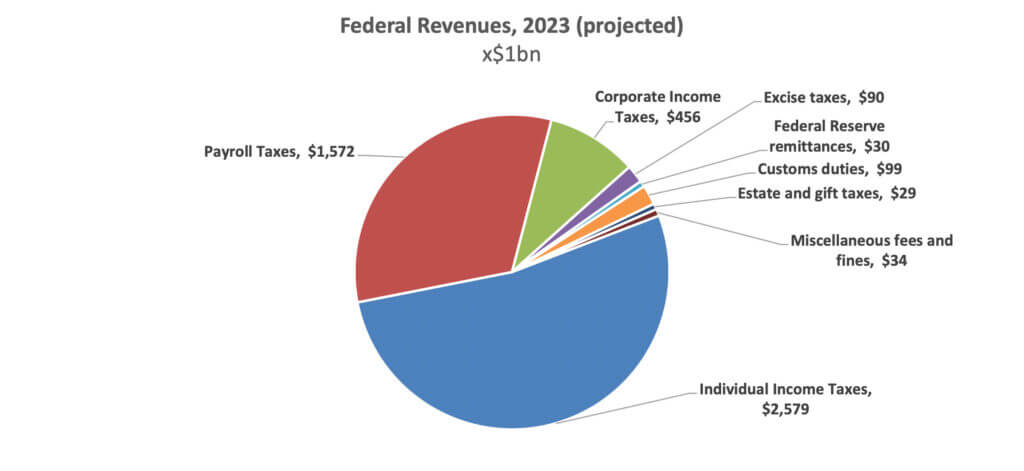

This year, the federal government expects to take in about $4.9 trillion in fiscal year 2023, compared with last year’s $4.8 trillion. You could make the case that, allowing for inflation, government revenues are actually going down, but be careful who you try to make that case to. If it’s to the American taxpayer who’s funding it all, the argument might not be well received.

That’s especially true because most of that $4.9 trillion is coming straight out of the taxpayer’s hide. Fully $4.0 trillion comes from income tax as well as remittances – split 50/50 with employers – for Social Security, Medicare and unemployment insurance. Aside from corporate income taxes the rest are, taken one at a time, almost low enough to be rounding errors.

Where the money comes from in fiscal year 2023. Short answer: You. Source: Congressional Budget Office

For all the political posturing surrounding corporate income or estate taxes, if you add them up it’s about a dime out of the federal dollar. No incremental change in the marginal tax rates to these revenue sources – or for that matter to customs duties or taxes on tobacco and alcohol – are going to move that needle in any meaningful way.

Still, this exercise in parsing federal revenue prompts three important questions:

- Do we need to spend this much?

- Are we spending it wisely?

- Can we afford it?

Mandatory funds

Let’s tackle the last question first, because it’s the easiest to answer: Yes, we can afford it. At least for now as it relates to the size of our economy. That doesn’t mean we ought to be spending that much, it just means we can.

The metric for this is looking at revenue as a percentage of gross domestic product. Currently, federal tax receipts amount to around 18% of annual GDP, according to the Congressional Budget Office, or CBO. Of that, a steady 4.3% per year gets locked away in the Social Security trust fund and the rest goes to general purposes – more on that later. All in, though, federal revenues have amounted to between 16% and 20% of the U.S. economy since as far back as 1962.

If you add in state and local levies, taxes amount to 26.6% of American GDP, according to the Organisation for Economic Co-operation and Development, which represents wealthy and middle-class nations. The tax-to-GDP ratio for all OECD members combined comes to an average of 34.1%. Citizens of other developed nations pay more than those in the U.S. do, but they generally get more services from their governments as well. It’s a tradeoff, and Americans have historically been wary of the kind of centralized policy solutions that others have come to rely on.

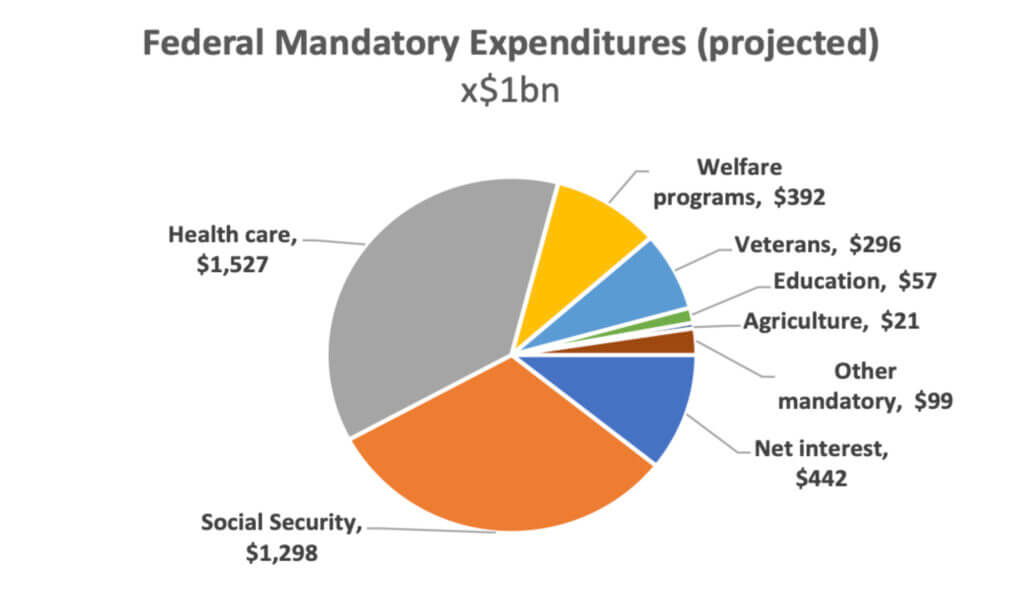

So, what does Washington sink it all into? Mostly stuff that we don’t really have a choice about: mandatory expenditures and net interest.

What we are required to spend it on in fiscal year 2023. Source: CBO

The astute reader will note that mandatory expenses add up to $3.7 trillion, compared to revenues of $4.9 trillion. So, we’re actually pretty thrifty, right? Well, no, not really.

Keep your eye on that net interest slice going forward. That’s how much we have to pay to keep current on our debt payments. It has always been more expedient politically to borrow money than raise taxes, and leaders in both parties have embraced floating more debt – at least once the mics were turned off.

And when interest rates were low, it made sense to borrow. If issuing a bond paying 2% interest would provide the incentives to get a global tech company to build a major semiconductor factory in a rural state here rather than in a foreign country, that would be viewed by most as money well spent. The thinking goes: We’d quickly make it all back by adding jobs to grow the state’s economy, which helps everyone. But, as you’ve surely noticed, interest rates are not what they used to be. And the CBO knows it.

Even so, that $442 billion – which amounts to $3,055 per American household – is probably an undercount. That’s just the budgetary number so don’t be surprised if, at the end of the fiscal year on September 30, it’s more like $500 billion. And we’re just getting started.

For about 20 years our debt service hovered around $200 billion per year then, in 2017, it started ratcheting up. For most of that time, not too many people cared because interest rates were so low. But now that we must make higher semiannual payments on our sovereign debt, it’s really blowing up. Expect the annual debt service amount to pass the $1 trillion mark in about seven years.

Surely, though, things aren’t that bad, right? We’re still taking in $1.2 trillion more than we are legally mandated to spend, aren’t we? True, but the devil always seems to be in the details.

What is technically but inadvisably called “discretionary” spending is where the real problems start. If you add in the Pentagon’s tab – and we can all agree that spending a significant amount of money on our nation’s defense is absolutely necessary - that tacks on $795 billion. Civilian discretionary spending comes to $963 billion. That category includes everything from funding embassies to NASA to general keep-the-lights-on expenses at federal buildings, as well as the pork projects and arts-and-culture grants that attract the attention of the budget hawks. There’s probably plenty of fat that could and should be trimmed from both military and civilian discretionary budgets, but good luck getting enough of that red-lined out. The new Republican majority in the House of Representatives has been vocal about cutting funding in both categories, but their proposals will have to win Senate approval and survive a presidential veto. More on that in the Captain’s Table column below.

Rent comes due

Netting it all out, the federal government anticipates spending $542 billion more in fiscal 2023 than it expects to take in via taxes and other revenues. That budget gap has to be made up somehow. That’s where borrowing – mainly in the form of bond issuance – comes in.

And sometimes there is nothing wrong with deficit spending. As alluded to above, many economists think that running a deficit can be good, if what you’re spending the money on actually spurs growth. Nobody, however, thinks that running a deficit year after year after year is a good idea. And yet that’s exactly what we do. Except for a four-year streak from 1998 to 2001, the federal government has run at a loss for at least the last 60 years.

That said, deficits from the 1960s were generally below $10 billion, a much smaller percentage of GDP at the time. The stagflation period of the late 1970s and early 1980s hiked that up by an order of magnitude, even though it was part of a plan to tame rampant inflation at the time. A plan, by the way, that worked. The economic expansion of the dotcom days erased the annual deficits for a few years, and then deficits returned during the George W. Bush administration. Whatever one thinks of W personally, or of his broader policy stances, it is problematic to describe him as a fiscal conservative. The $128 billion budget surplus he inherited became a $158 billion deficit in just 12 months. Not all of that was his fault, of course. We were drawn into a war, and we all know that wars are expensive and can strain a government’s financial resources. Still, that might have been the moment to simply refrain from raising taxes, rather than cut them. Bush’s refund checks to American taxpayers were essentially backed by borrowed money.

And again, it’s not Bush’s fault that his term ended during the Great Recession, but the last budget he submitted to Congress was the first to exceed $1 trillion of red ink. The Obama and Trump administrations can both take bows for getting the deficit under control – that is, back into the hundreds of billions – but then came Covid, and the deficit surged again to more than $3.1 trillion. In 2023, though, it’s projected to be only about one-sixth that number.

The worst thing about deficits, though, is that they’re cumulative. They don’t go away. Instead, they get added to the debt the government already owes. According to the U.S. Debt Clock – and you have to see this to believe it – the national debt is roughly $31.5 trillion.

We won’t depress you with what that comes to per citizen or per taxpayer, which the Clock will show you in big, bold red type. “Kitchen table” budget analogies can be helpful, but aren’t really applicable because running a household and running a government have their differences. A two-income family living in a split ranch can’t print its own money in the basement. There’s something special about being a sovereign nation, especially one that issues the world’s most in-demand reserve currency. It doesn’t matter how much you borrow if you own the bank, at least for a while. Still, there are limits and running large deficits year after year and piling debt onto ourselves will at some point result in a painful reckoning.

Spending time

GDP is the real benchmark of a nation’s ability to pay back its debt. The Reagan administration caught a lot of flak for taking the federal debt from 30% of GDP to 50%. The White House, though, was able to counter that the ratio hit 100% during World War Two and we came out winners. Today, though, we’re at 120% and nobody’s shooting at us. This isn’t a good place to be. What if we’re suddenly thrown into a conflict or face some other major disruption that takes a toll on our nation’s finances? We are really on the warning track now.

If you’re uncertain how to invest during a time of rising government debt, you might want to consult with a trusted financial advisor who’s lived through this before and who has thoughts on the best places to put your money.