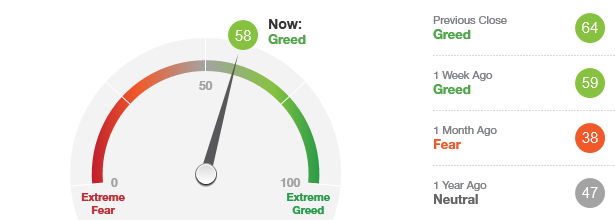

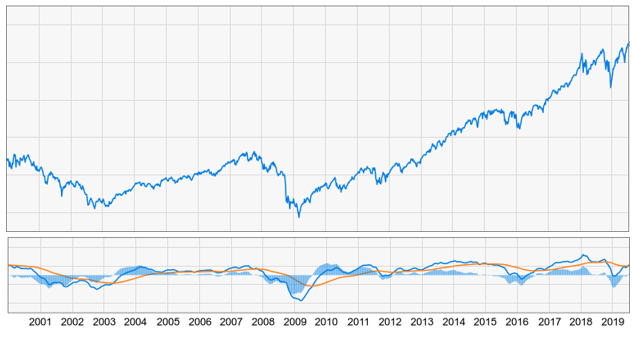

Market Overview

This month's models are posted. There are NO CHANGES in any of the models.

The student debt bomb

Quick: What’s the biggest source of debt in the U.S.? If you answered, “mortgages,” you’d be right. But that’s almost too obvious. What comes next? Cars? No, that’s third. Credit cards? Not even close. Medical bills? Someday, maybe.

It’s student loans – the bankruptcy-proof ones you can never get out of until they’re all paid off. The typical American paying off student loan debt is 30-something, not 20-something, according to a Federal Reserve Bank of New York-Equifax study cited by CNBC. And it will take that individual an average of 19.7 years to pay off the whole note. So, the typical American who started paying back a student loan in their 30s won’t make their last student loan payment until they reach their 50s.

For those of us stuck with this burden, there’s not a lot we can do about it. But maybe we can provide some guidance for the next generation.

The problem

Seven out of every ten recent college graduates have student loans to pay off. According to Debt.org, the average debt is nearly $40,000, and the average monthly payment is almost $382. That’s almost $4,600 per year that isn’t going toward saving for retirement or starting a family. The Wall Street Journal offered a dire report this year on how this indebtedness is keeping younger adults out of the housing market.

But it’s even worse than that. These figures are only for loans taken out for the specific purpose of paying for college. This doesn’t include parents’ second mortgages or borrowing against their retirement assets. It doesn’t include credit card debt racked up in pursuit of college educations. Although ten years have passed since federal law ended the Wild West show that was the campaign to market credit cards to students, Sallie Mae reports than 9% of college students still put some of their tuition on the plastic.

But it’s worth it, right? After four years of living on ramen noodles and free refills of Mountain Dew, you would think that a college graduate still stands to make substantially more than a high school graduate.

Depends on your definition of “substantially.” The average freshly minted college graduate makes $48,400 in starting salary according to CNBC. Meantime, the average kid out of high school made $30,500. By the time the college grad makes their job market debut, though, the high school grad has been making that salary for four years and is probably already due for a raise or promotion. Eventually, that bachelor’s degree will unlock its value, but student loans issuers generally expect payments starting six months after graduation.

Don’t worry – you can pay it all off in less than three years if you don’t buy food, rent a home or pay taxes. Credit: CNBC.com

So, it’s clear that college debt is a challenge for recent graduates and their families. But consider the aggregate effect of all this red ink.

The even bigger potential problem

If $40,000 doesn’t sound like a lot of money to you, then how about $1.5 trillion? That’s how much Forbes reports is the total outstanding student loan debt in the U.S.

For comparison’s sake the total outstanding mortgage debt is $10.2 trillion, or almost exactly where it was at the start of the Great Recession. But it wasn’t so much the total mortgage debt that was the problem. It was the subprime portion that triggered the worst economic disaster America had faced in a lifetime. Subprime mortgages totaled $1.3 trillion in 2007, or pretty much exactly where we are now, inflation-adjusted, with student debt.

Now let’s define our terms. At the beginning we referred to student loans as bankruptcy-proof, but they are not default-proof and the consequences are bad. Think damage to your credit score, garnishment of your tax refunds or even wages. While you still may be able to get a used car with a bad credit score, banks might be less likely to give you the money you need to buy a house. A sub-prime mortgage is typically one taken out by a borrower with a sub-600 credit score. Federal direct student loans are often extended to students without any credit score at all, and private companies are lined up to provide loans to students who have a co-signer with virtually any credit score.

It’s hard to determine if student loan asset-backed securities – SLABS (not kidding) – are inherently more or less risky today than the mortgage-backed securities (MBS) and collateralized mortgage obligations (CDOs) were in 2007. That’s mainly because of the way bond rating agencies were incentivized back then – a lot of junk MBSs and CDOs were actually given A+ ratings.

But risk of default is not the same as actual default. As long as the economy keeps growing and the value of the degree keeps increasing, there really isn’t a problem. At the moment, the economy is exceptionally strong – especially considering how long the current expansion has been playing out. Still, there’s some reason for alarm.

“Because of the inherent similarities between the student loan market and the sub-prime mortgage market, there is rampant fear that the student loan industry will be the next market implosion to trigger a financial crisis,” according to Investopedia. “Evidence has shown that even in the current recovering economy, the majority of new college graduates have not been able to find jobs that allow them to pay back their student loans. The result is a default rate that has been increasing since 2003.”

And here’s a thought that is a little off-topic, but only a little: subprime auto loans also exceed $1 trillion.

The solution

From a policy perspective, there are a number of ideas circulating about how to cap exposure to student loan debt and thus, perhaps, postpone the next recession. The most radical of these, coming off the stump speeches of more than a couple Democratic presidential hopefuls, is to make college free to students, at least at public institutions. Conservatives tend to oppose this because it constitutes another mandate for taxpayers to fund. Liberals aren’t all on the same page on this one because it would represent a transfer of value to families that tend to be wealthier. So a free tuition plan isn’t likely to materialize anytime soon.

What might happen, though, is a “needs test” for free tuition or a loan forgiveness program for graduates who volunteer for national service.

Another thought is getting employers to contribute to their employees’ student loan payments, in much the same way as they contribute to retirement plans or healthcare savings accounts. The reason why they don’t already is that there’s no tax incentive to do so, as a recent op-ed in The Hill points out.

But this is still as theoretical as those other policy fixes and, while it has many private-sector virtues, let’s also remember that this would leave out all 60 million workers in the gig economy.

Obviously, the best way to get out of the debt trap is to not get into it in the first place. Scholarships are available for truly worthy recipients who need the money. But there will never be enough scholarship money to go around. So before cosigning on a student loan with your kid, here are some other things to consider.

Needs-based grants may be available from the federal government, the state government, or from the college itself. This involves filling out the Free Application for Federal Student Aid as well as state-level equivalent paperwork – an unpleasant task, certainly, but quite possibly the most cost-effective use of your time. Some paperwork just has to get done, no matter how one feels about it.

Work-study and other part-time jobs can at least take care of the student’s personal expenses during their college years. Considering that this generation is less likely than its predecessors to work during high school, so this might be a big leap, but it’s time to start adulting.

A $2,500 per American Opportunity Tax Credit is available through the federal government, and similar programs exist at the state level in some locations. Ask your accountant or tax professional for more details.

On one level, securing a college education is like any other business transaction. It’s OK to haggle with the school.

It’s also OK to spend a year or two in community college before transferring to a more prestigious, that is, expensive, school. When your kid gets out, nobody is likely going to care where they were a freshman or sophomore, only the name of the school on the diploma matters.

So, while there’s a lot to be concerned with when it comes to college debt, students and parents have options. If you’re planning on taking on this challenge, think about scheduling an appropriate amount of time to consider them, and plan how you’ll tackle this education funding conundrum.

Rex Moxley joined Smith Anglin in 2001. Since then, he's served as a Managing Partner and as a member of the firm's Investment Committee. He regularly meets with prospective clients, counsels existing clients, participates in investment portfolio analysis and develops materials for communicating with the firm's clientele and target markets. He holds a BBA in Finance and Marketing, a graduate degree in Law and numerous securities licenses and designations.

Rex Moxley joined Smith Anglin in 2001. Since then, he's served as a Managing Partner and as a member of the firm's Investment Committee. He regularly meets with prospective clients, counsels existing clients, participates in investment portfolio analysis and develops materials for communicating with the firm's clientele and target markets. He holds a BBA in Finance and Marketing, a graduate degree in Law and numerous securities licenses and designations.