Market Overview

This month's models are posted. There are CHANGES in ALL THE MODELS (highlighted in yellow).

Looming debt: Worse than you feared, but not as bad as you think

Debt is piling up. That’s for sure.

If the headlines are to be believed, we’re all going broke except for the bill collectors and bankruptcy lawyers.

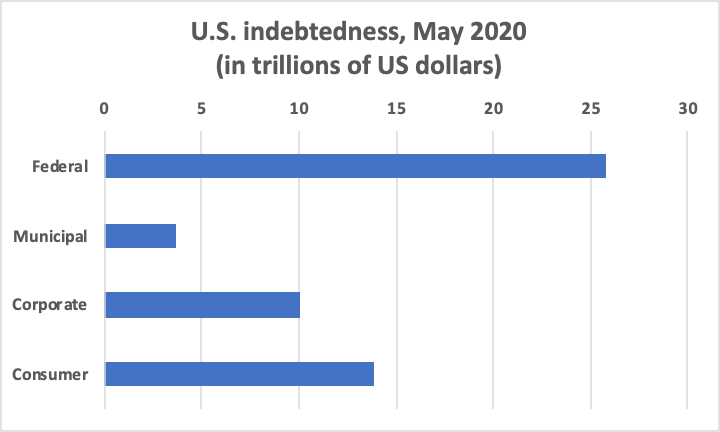

We do indeed live in a more indebted world than we ever have before; if you add up the different lines in the chart below, you’ll find liabilities totaling $53.5 trillion. But borrowing isn’t necessarily a bad thing. It often plays a useful role. The ratios that measure debt loads have their uses as well, but they also have their limitations.

As we exit the crisis stage of the coronavirus pandemic and enter the recovery stage, it’s important to avoid conflating different kinds of obligations and what their run-up means to the economy. Elevated levels of national debt, municipal debt, corporate debt and consumer debt are all going to be with us for some time, so let’s make sure we’re dealing with them each appropriately.

Don't spend it all in one place. Sources: U.S. Treasury, SEC, Federal Reserve, Debt.org

Federal

The problem is global, but it’s a daunting enough challenge to just keep track of all the red ink flowing here in the U.S. Let’s start, then, with the obligations of the federal government.

Prior to the pandemic, the Federal Reserve actually had a fairly solid balance sheet. It wasn’t great, but it was better than it had been in many years. We’d just finished paying off the Great Recession, and the monetary policy makers were starting to take a contractionary stance and shedding Treasury instruments off the Fed’s books. But President Trump, who built his career on debt financing, wasn’t in favor of such moves. We talked a little bit about that in this space last year.

As we all went into lockdown, the Fed moved to effectively 0% target interest rates and broadened its palate for debt securities. The next shoe soon dropped, with the president and Congress agreeing to undreamt-of stimulus funds. So now we’re dealing with $25.8 trillion in total federal debt.

The debt is essentially the running tally of the government’s annual budget deficits. The deepest, according to a brilliant article in The Balance, was $1.5 trillion. That was in 2010, when the bills came due for the financial crisis. The 2021 deficit was supposed to be a more modest $1.1 trillion, but that projection was made before covid-19 had a chance to effectively doubled it. But all these numbers pale in comparison to the projected, virus-fueled current-year shortfall of $3.7 trillion. That is to say, take the worst deficit we’ve ever had, double it, and you still don’t approach how much this pandemic has cost us as a nation.

Even so, the one-month total is sobering enough: $737 billion. But wait, it gets worse. The month in question – the most recent for which we have Congressional Budget Office data – is April, you know, the month when the national coffers are flush with new revenues from income taxes. No matter how bad the deficit is the other 11 months, the Treasury is generally flush in April. In April 2019 for instance, Washington reported a $160 billion surplus.

And yet there may be little cause for panic.

“The whole point of having a strong balance sheet is to be able to use debt aggressively when you are faced with a full-on crisis. I would have no problem with policymakers taking the same actions twice over if it means we get out of this in one piece,” Harvard University Professor Thomas Rogoff told Goldman Sachs’s Top of Mind podcast. While he expressed mild concern over the economy’s ability to grow with that kind of debt load, “the growth implications of not borrowing would be a lot greater than any growth implications of borrowing.”

And yet Rogoff, a former International Monetary Fund chief economist who teaches both public policy and economics, concedes that the headline federal debt number is a lowball figure. It only tallies all the bonds, bills and notes floated by the Treasury Department and other issuing bodies. It doesn’t include the unsecuritized obligations of the federal government. Social Security, the largest of these, amounts to $53 trillion – or roughly the federal, municipal, corporate and consumer debt combined. Yikes.

Even so, Rogoff doesn’t believe the conventional wisdom that high federal debt inevitably leads to high inflation.

“As long as interest rates stay very low, that isn’t necessarily the case,” he told interviewer Allison Nathan. “Something has to happen that creates pressure, and the reality is that we will probably see deflation for a prolonged period.”

Municipal

When Washington enacted the coronavirus bailout package, there was one glaring omission: aid to state and local governments. For all the lip service paid to the frontline responders who work under the banners of police, fire, transit, ambulance, hospital and – let’s not forget – sanitation, $0 was funneled their way under the CARES Act. Another multitrillion-dollar bill is currently stalled on Capitol Hill as we deal with not only with the Senate’s usual leisurely pace but also the emergence of yet another generation-defining national crisis.

While the $3.7 trillion in aggregate muni debt isn’t all that huge compared with the other sources of encumbrance under consideration, it’s likely to spike. States face a current budget shortfall of $350 billion, mainly due to the revenues foregone and expenses incurred as a result of the pandemic, according to Goldman Sachs fixed-income co-head Sylvia Yeh. That compares to the $230 billion the states had to forego during the 2008-09 financial crisis.

“States are unlikely to default regardless of their circumstances. Even the most stressed states in the country have broad powers of taxation, budget cuts and access to the capital markets and [the Fed’s Municipal Liquidity Facility],” Yeh told Top of Mind. Still, “localities tend to default more than states. This is in part because municipalities are generally less sophisticated and more prone to errors in judgement … [but] local municipal defaults are well telegraphed by local financial metrics, debt figures and credit ratings.”

Corporate

Yeh further notes that, while municipal and state borrowing has been fairly constant over the past decade, corporate debt – now passing the $10 trillion mark – has roughly doubled over that time.

It’s not just the quantity that’s an issue, though. It’s the quality. Corporate bankruptcies were on the rise long before covid-19 even existed, as a 2018 Global Finance article indicates, and the rise of covenant-lite – bank-speak for “no questions asked” – corporate loans were on the upswing. Essentially, cov-lite loans are to corporate lending now what subprime loans were to mortgages just before the 2008 collapse.

“I do expect a wave of [bankruptcy] filings this time around,” University of Pennsylvania law professor David Skeel told Nathan. “It’s hard to tell just how big that wave will be, but I wouldn’t be surprised if filings increased a lot more than they did during the global financial crisis, when they essentially doubled.”

Skeel said that, the larger the company, the more likely it is to be allowed to continue operations while it restructures under bankruptcy protection. But the smaller the company, the more likely it is to be forced to liquidate. Because that’s the way it has always been.

What’s new, though, is that the courts, which hear bankruptcy cases, are going to be flooded with them, and will probably be running at a reduced degree of efficiency in order to accommodate social distancing and other new-normal protocols. As reorganizations take longer and become costlier, that might force more filers to accept simply selling off their stock and assets, then going out of business.

Consumer

Which brings us to your personal debt, and ours. The positive side of having a consumer-oriented economy is that the means of production and distribution are geared toward making us all happy. The negative side is that, when millions of U.S. consumers have been infected with a virus that is killing off roughly 10,000 Americans per week, that economy shuts down.

And by “that economy,” we mean income. The money stops flowing. Demand remains, even if we can’t pay for it. So consumer debt spikes. According to Debt.org, that totaled $13.9 billion before the pandemic. About two-thirds of that was mortgages, with the rest divided more-or-less evenly between cars, student loans and credit cards.

Although there is not yet much in the way of hard data available to measure how much, it’s clear that Americans are putting more on the plastic as a result of the shutdown. According to CreditCards.com, almost one in four of us have increased our balances due to the crisis.

This suggests then that one in four of us – at the very least – could use some counseling on how to get out of debt. Chris Lott discussed that in broad strokes in a recent “From the Captain’s Table” column, but so far 2020 has done everything it can to further complicate the matter. So maybe it’s best to consult a financial professional before you get lulled once again by allure of that PayPal Credit button.

Steve Anglin, CPA is a Managing Partner at Smith Anglin Financial, and the Head of the Tax Preparation Services. He is also responsible for Smith Anglin’s compliance supervision. He holds a BBA in Accounting and a BBA in Real Estate, and numerous securities licenses and designations.

Steve Anglin, CPA is a Managing Partner at Smith Anglin Financial, and the Head of the Tax Preparation Services. He is also responsible for Smith Anglin’s compliance supervision. He holds a BBA in Accounting and a BBA in Real Estate, and numerous securities licenses and designations.