This month's models have been posted. There are CHANGES in ALL of the models (highlighted in yellow).

Plug and play: The rise of electric vehicles

We’ve wanted to do this one for a long time – about a year. Where did that year go? What could possibly have been so important that talking about cool cars seemed like too idle a pursuit? It escapes us now. Anyway …

It’s no exaggeration to describe America’s relationship with the automobile as a love affair. Cars came on the scene as part of the Second Industrial Revolution, around the turn of the 20th century, just as the United States was maturing past its adolescence. We were instantly smitten. While other nations embraced high-speed trains, light rail and bicycle lanes, we remained loyal to our first sweetheart – the car. Despite all those hipsters whirring around on Vespas, we are a car culture.

The thing about infatuations, though, is that they don’t stand the test of time. Habits which were once endearing become annoyances. In the car’s case, she is loud. She runs up the credit cards. And, let’s face it, she’s something of a slob.

But she’s been working on herself, and with amazing success. This is no mere facelift. With the advent of electric vehicles, be prepared to fall in love with the car all over again.

Our first electric vehicle. Credit: Scott's AFX

Our next electric vehicle. Credit: Audi

Money, money, money

As much as we’d rather talk about the cars, let’s bear in mind this is a personal finance newsletter and concentrate on whether or not switching to an EV could save you money. Evidence suggests it can.

Basically, there are two elements of cost: the initial purchase price and the periodic costs of ownership. Looking at initial purchase price in isolation, you’re almost always going to pay more for an EV than for a similarly equipped gas-powered vehicle in the same class. Subsequent costs, though, can be dramatically lower for the EV.

Obviously, fuel is cheaper. By all accounts, it costs roughly half as much to fill a battery array than a fuel tank. Your mileage, to coin a phrase, may vary. If you live near the Illinois-Missouri, Tennessee-Mississippi or California-Arizona borders, then you know how much gas prices differ across a dotted line on the map. Surprisingly to some, the same goes for kilowatt-hours. Some states have cheap electricity and expensive gas while some have cheap gas and expensive electricity. Some have expensive both. (Looking at you, California.) CleanTechnica lists five states where driving an EV could save you $1,000 or more per year. Oregon and Colorado are among them, sure. But so are Maryland and Delaware. The real surprise is New Jersey, though, where New Yorkers and Pennsylvanians both go to fill up.

Even so, it’s important to note that fuel is not a huge portion of a vehicle’s total cost of ownership – just the most visible and thus the most emotionally fraught. Car & Driver estimates the average driver pays $1,700 per year for gas. That’s like three new-car payments, according to LendingTree.

Those payments include not just the purchase price, but the financing as well – and that interest adds up if you have creditworthiness issues, or even if you elect to pay the car off over five years instead of three or four. Car payments also include a warranty. Typically it’s for one year, but they can often be for several years.

Then there’s insurance, taxes, registration and all the other gotchas of car ownership, but they’re not likely to make much of a difference in the gas-versus-electric choice. Post-warranty maintenance strongly favors EVs, though, because a whole lot more can and will go wrong with an internal combustion engine than with a battery.

One item that will affect the calculus – but shouldn’t – is depreciation. It reflects the reality that equipment loses its value as it ages, but it’s really an accounting trick with no cash impact. Let’s say you believe that you’ll own your car for six years; straight-line depreciation suggests that it loses one-sixth of its value annually. Does that mean your car is worthless if you hold onto it for a seventh year or longer? No – it just means you’re driving “free” from an accounting perspective.

Depreciation, though, isn’t straight-line when it comes to cars – it’s accelerated. Your car loses more value during its first year than its second, more during its second than its third, and so on.

Both C&D and Consumer Reports factor depreciation into the equation. CR, however, examines the entire expected lifetime when comparing gas- and electric-powered vehicles, and C&D only looks at the first three years. That’s why CR estimates that EVs are cheaper to own than gas-powered models and why C&D reaches the opposite conclusion. C&D is, to use the technical term, wrong.

But wait! There’s more!

Still, that purchase price is not an inconsequential factor and, if all you’re looking at is sticker price, you’ll pick the gas-powered model every time. There are, however, tax incentives to sweeten the deal for EVs.

Since 2010, the federal government has offered up to $7,500 in tax credits upon the acquisition of an EV; the credits might be lower for you if you pick a hybrid. This was always intended as “training wheels” for the industry and, once an automaker sold 200,000 units, it was no longer eligible to pass this benefit on to its customers. Accordingly, the U.S. Department of Energy, General Motors and Tesla no longer need training wheels.

But there are other automakers. Most of the luxury brands – Audi, BMW and Mercedes-Benz, for example – still qualify. At the other end of the scale, so do Kia and Hyundai. In the middle, you have Ford and Toyota.

Aside from the legacy car companies, though, there are also such EV natives as AMP, BYD, Koda Kandi, Wheego and Zenith.

But even if you’re already sold on the Chevy Bolt or Tesla Model 3, there might still be tax dollars to be found. Different states have different enticements. While tax credits on the purchase price is the most obvious, states also offer:

Discounted utility bills for EV owners,

Vehicle registration discounts and emission testing exemptions,

Rebates and tax credits to install charging stations at both businesses and residences,

Reduced insurance rates,

More favorable financing rates, and

Toll-free travel on roads, bridges and tunnels.

There are further non-financial incentives to go EV, such as unlimited HOV lane usage and free parking close to store entrances. Plug In America has a great interactive map.

Charging forward

So, while it’s a complicated formula, EVs are likely to be in your future. And in your near future at that. We haven’t even discussed the impact of the next iteration: self-driving vehicles. Right now, they’re still very much a work-in-progress, but it’s only a matter of time before they evolve from an accident-prone, late-night punchline into a shiny piece of metal your neighbor makes a display of washing and polishing every weekend. It might be a self-driving Uber that takes you to the airport, and a self-driving truck that delivers the fuel to the flight line. Of interest to many readers of this newsletter, there could come a day when the airplane itself is a self-driving vehicle.

But for now, we’re just talking about cars and light trucks, and whether it makes sense to buy one. The devil is in the details. It might be worth your while to discuss the pros and cons of EV ownership with a trusted financial advisor. And if that advisor already has an EV, it might be a long conversation.

Are you ready to retire? Can you afford to retire?

Provided by Smith Anglin Financial, a 2020 Financial Times 300 Top Registered Adviser Firm

US Economy

Gross domestic product (GDP) for the first quarter was adjusted down to a 6.4% annual rate, according to the second estimate released by the Bureau of Economic Analysis. Exports and private inventory investment were not quite as robust as the initial report suggested but, with an overall score that high, nobody is complaining.

Initial jobless claims for the week ending May 29 came to 385,000, a 20,000 week-over-week decrease. This is the lowest reading since the pandemic lockdown started. The four-week moving average was 428,000, a decrease of 30,500 from the previous week's revised average. These numbers are significantly below those reported here last month.

Total nonfarm payroll employment rose by 559,000 in May, the Labor Department reports, and the unemployment rate dipped to 5.8%.

The Consumer Price Index for All Urban Consumers increased 0.6% in May on a seasonally adjusted basis after rising 0.8% in April, the Labor Department reported. A 7.3% jump in used cars and trucks accounted for one-third of that. Over the last 12 months, the all-items index increased 5.0% before seasonal adjustment.

US Stocks

The S&P 500 posted a +0.7% gain in May on a total-return basis, while the Chicago Board Options Exchange VIX “fear gauge” moved sharply in the opposite direction; its month-end 16.76 close was 9.9% lower than the previous month-end.

International

Globally, equities were all positive. In Europe, Frankfurt’s DAX, Amsterdam’s Euronext 100 and London’s FTSE 100 were up +1.9%, +1.7% and +0.8% respectively. In Asia, Tokyo’s Nikkei 225 eeked out a 0.2% gain, and that was its best monthly performance in some time. Hong Kong’s Hang Seng rose +1.5%, in line with the Western exchanges, but Shanghai’s SSE Composite beat the world with a +4.9% surge.

Central Banks

The Federal Reserve plans to wind down the portfolio of the emergency lending facility that supported large employers’ credit through the Covid-19 pandemic. Based on Fed data, we estimate this comes to about $13.8 billion in corporate bonds and exchange-traded corporate bond funds.

Commodities

Oil prices, which often rally late in the economic cycle, continue to push higher. West Texas Intermediate crude gained +4.3%, ending May at a profitable $66.32 per barrel. Meantime, inflation hedge gold rose +7.8% to end the month at $1,905.30 per ounce.

The dollar was down another -1.7% against the euro and -2.9% against the pound in May, but rose a slight +0.2% against the yen.

Cryptocurrency continued its reversal as Bitcoin dropped to $36,880 (by month end?). While the plunge might cause intestinal distress to most investors, losing -35.4% in a month is not the worst thing that’s happened to any long-term crypto investor or enthusiast. So far, it has always come back and is in fact still positive year-to-date.

Trading Restrictions Reminder!

Your 401k plan has trading restrictions, so you must keep track of your buy and sell orders. Not paying attention could leave you locked out of trading.

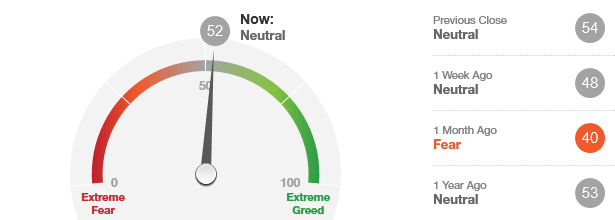

Fear & Greed Index

As of 6/14/21.

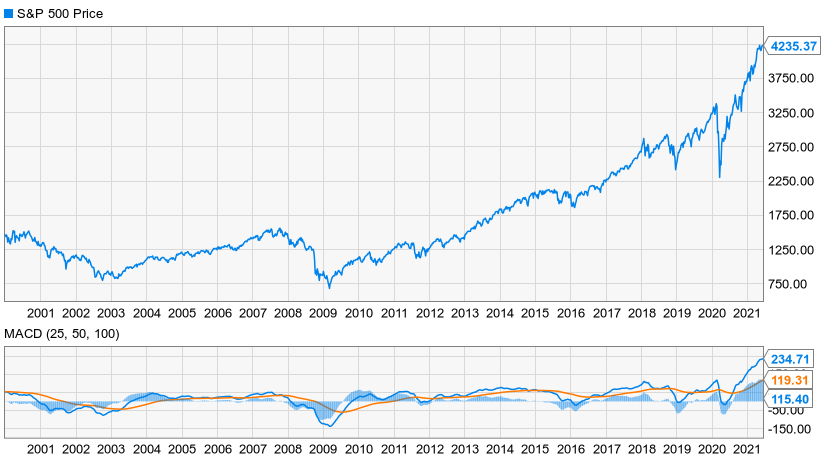

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

Dare to DeFi?

“DeFi” is the buzzword of the year in financial circles. But what does it mean – and what does it mean for you?

DeFi is shortened version of decentralized finance and is defined as “the ecosystem of financial applications being built with blockchain technology,” according to cryptocurrency news source CoinMarketCap. The term “DeFi” was coined in an online chat among crypto-famous luminaries in August 2018 who “were discussing what to call the movement of open financial applications being built on Ethereum,” according to Camilla Russo, the article’s author. “Other options considered were Open Horizon, Lattice Network and Open Financial Protocols.” But it was hard to beat the winning entry which, after all, is pronounced “defy”.

That kind of oppositional stance is endemic in the crypto community, so how did it end up being discussed by Wall Street’s graying establishmentarians?

“Banking has always meant bankers, the people who arrange everything from savings accounts to synthetic collateralized debt obligations. But what if computer code could take their place?”, Olga Kharif asks on behalf of Bloomberg.

The building blocks of DeFi are more than a decade old, and the goal of decentralizing finance has been aided immensely by crypto experimentation.

“A DeFi world could be one where money flows more efficiently and more fairly, its proponents say, pointing to platforms where users are boasting of hefty returns,” Kharif posits.

Nuts and bolts

You might have to spend an hour on YouTube tutorials to really get the following, but here are the bullet points:

Blockchain is the technology that enables cryptocurrencies, but it does that by creating a shared database that never requires auditing because all transactions are witnessed and agreed to by all subscribers to that database. There can never be a disagreement on a properly operating blockchain.

Decentralized applications – dapps – are the widgets that enable those transactions to be performed, whether they be sales of securities, or direct loans, or what have you.

Dapps function because they are programmed with so-called smart contracts, which are just self-executing contracts that automatically and unfailingly release one item of value in exchange for another as long as specific conditions are met.

DeFi uses specially designed cryptocurrency tokens to enable the sale of – for example – Bitcoin Core, which lives on one blockchain, with Ethereum, which lives on another, via a smart contract executed on a dapp, which functions as a neutral exchange.

Given that infrastructure, it’s easy to see how trading cryptocurrencies can be – indeed, has already been – made easier by DeFi. But not everybody is into crypto. Still, it’s certainly not uncommon to be trading in stocks, and there are millions of amateur traders who dabble in foreign exchange and commodity futures. And that’s where DeFi’s future lies.

Use cases

By the end of the year, you could be able to use DeFi dapps to trade anything you might trade electronically. They might provide you with margin lending. They might enable to you to leverage your equity 10 times or 100 times rather than the three times which current U.S. trading rules set as the ceiling. They might even extend you consumer loans or, for that matter, mortgages.

Of course, regulators are going to have something to say about all that. There are reasons why exchanges are regulated, and particularly why some of those regulations apply to trading on margin. Those overseeing banks will likewise look askance at any development which gets around their 26-page list of the actionable provisions of U.S. lending laws.

In the meantime, though, there has been some convergence between the industry side and the compliance side. For example, Coinbase – the leading U.S.-based crypto trading platform – is not only licensed by both the federal and New York State governments as a securities exchange, it’s also a public company with its own shares trading on the Nasdaq.

As for lending, the confluence is just as visible. The advent of cryptocurrency occurred in 2008, coincident with – but unrelated to – the financial crisis. That crisis, though, led Washington to pass the Jumpstart Our Business Startups Act of 2012, which extended all kinds of private placement and crowdfunding opportunities.

And crypto, by its very existence, flies in the face of the prerogatives of the Federal Reserve and the world’s other central banks. And yet, there’s no law that says all money has to have the picture of a dead president on it, so the Fed has had to reach a détente with the crypto space. So has every other monetary authority. Why, some have even found ways of working with it and establishing a reasonable regulatory system which crypto proponents can live with.

Laying down the law

America, though, is still a long way from that kind of accommodation. We’re not even sure how to regulate it here. It’s not really currency – at least, not yet – so it can’t be treated like forex. It’s not a commodity, so it can’t be treated like futures contracts unless it’s specifically structured like futures. Nor is it equity, although that’s how the Securities and Exchange Commission has at times viewed it, as we reported earlier this year in the case of XRP and its related corporate entity, Ripple Labs.

Crypto is an entirely new asset class, and our leaders would be well served to figure that out before the rest of the world’s economies do. And that has everything to do with the decentralized nature of its financial impact – the “De” nature of its “Fi”.

So be careful

While the prospect of sidestepping government regulations is tempting, there is a significant downside. If anything goes wrong, you would have no legal protection. If you get hacked or scammed, it’s on you. There’s no way to recover a penny. That’s why we live by the rules of the road which made the U.S. financial system the envy of the world. We accept the tradeoff: You can’t have both total freedom and total protection, so we need to give up a little of the former, however reluctantly, to have any of the latter.

DeFi is likely to affect you in very real ways, but exactly how has yet to be determined. Those who follow it closely will tell you that the foundation has barely been laid, and there’s no telling what the structure is going to look like once it’s substantively built out.

While DeFi might mean you never have to see a banker again, it’s likely to increase the number of options you have as an investor, regardless of asset class. We expect you’ll find, even when DeFi is completely ubiquitous, you’ll still need the advice of a trusted financial expert.

-David

David Camarillo, CFP®, ChFC, CFS

Director of Advisory Services

David is a proud Trinity University alum, where he earned his Bachelor of Arts in English and History. He started his career in the financial services industry in 2005 at Wells Fargo, and in 2007 he joined H.D. Vest Financial Services where he consulted for the company’s top financial advisors. He held a Series 7 and 66 until 2018, and he still holds life and health insurance agent and variable insurance products agent. He obtained the Certified Financial Planner™ (CFP) designation in 2011, the Chartered Financial Consultant (ChFC) designation in 2014, and holds the Certified Funds Specialist (CFS) designation. David has been a Wealth Advisor with Smith Anglin since 2014, and in 2019 he was promoted to Director of Advisory Services.

Outside the office David stays active with his wife, Mayra, and two kids, David Jr. and Amelia. David is an avid runner, racing everything from the 5k to the marathon. He enjoys hiking nature trails with his family and their dog, Bo, and playing guitar loudly when possible. He also volunteers with Back on My Feet and the North Texas Food Bank.