This month’s models are now available. There were CHANGES in ALL of the models (highlighted in yellow).

The Only Thing To Fear Is Mild Anxiety Itself

Wall Street is worried. But does it really have a reason to be?

The CBOE Volatility Index (VIX)—the so-called “fear gauge”—has had some rough sledding lately. After 15 months circling in a holding pattern in the 10-to-15 range, the line rocketed straight up to 37. Since then, it settled into another range between 15 and 25.

Some perspective. The only time the VIX was uncomfortably stuck above 30 for more than three straight months was during the Great Recession. Even then, it wasn’t until Lehman Brothers’ September 2008 meltdown that the VIX reached that level—kind of a lagging indicator. The VIX would double, reaching the 60s a few weeks later, and on a few days it reached a stratospheric intraday high of almost 90. And if you are curious, when the S&P 500 bottomed on March 9, 2009, the VIX closed at 49.

Lehman Brothers sign in an auction house window. Photo credit: Jorge Royan.

The VIX’s spike up to 37 last month was just that, a spike … a furious, although temporary event. It also occurred annually, like clockwork, in 2009, 2010 and 2011, then quickly became last week’s news as the slow, steady recovery progressed. Same thing happened in August 1998 in the middle of the dotcom boom. It actually dropped into the teens during the mini-recession that followed the tech bubble bursting.

Where is the VIX right now? It’s near the historical norm—so you see that we’re actually in pretty familiar territory.

Our agitation today is about one-third what it was when Hank Paulson and Ben Bernanke were trying to save the world. In other words, the VIX is right about where it was once we figured out they managed to do just that. It’s actually lower than it was most the time that any stock with “Web” or “e-“ in its name could expect a three-digit P/E ratio.

So why are so many people still so nervous?

The VIX tends to move in parallel with interest rates. As bond yields rise, there’s less of an incentive to take the risk of equity ownership when you can get solid returns with comparatively risk-free debt securities.

Bond yields rise in response to increases in the Fed Funds rate. The Federal Reserve resets this rate in anticipation of inflation. Raising the cost of borrowing reduces the money supply, so inflation can only erode the spending value of a dollar so far, or so the theory goes.

Array

The Fed retains its 2% target rate for annual inflation over 2018. That’s low. To give an idea of just how low that is consider that inflation peaked in 1980 at 13.5%. Lesson #1 in getting a second term – don’t let inflation get to the double-digits your re-election year. That was all that was needed to end Jimmy Carter’s presidency. Candidate Ronald Reagan went on the air and asked America, “Are you better off than you were four years ago?” And that changed the whole political dialogue in this country ever since.

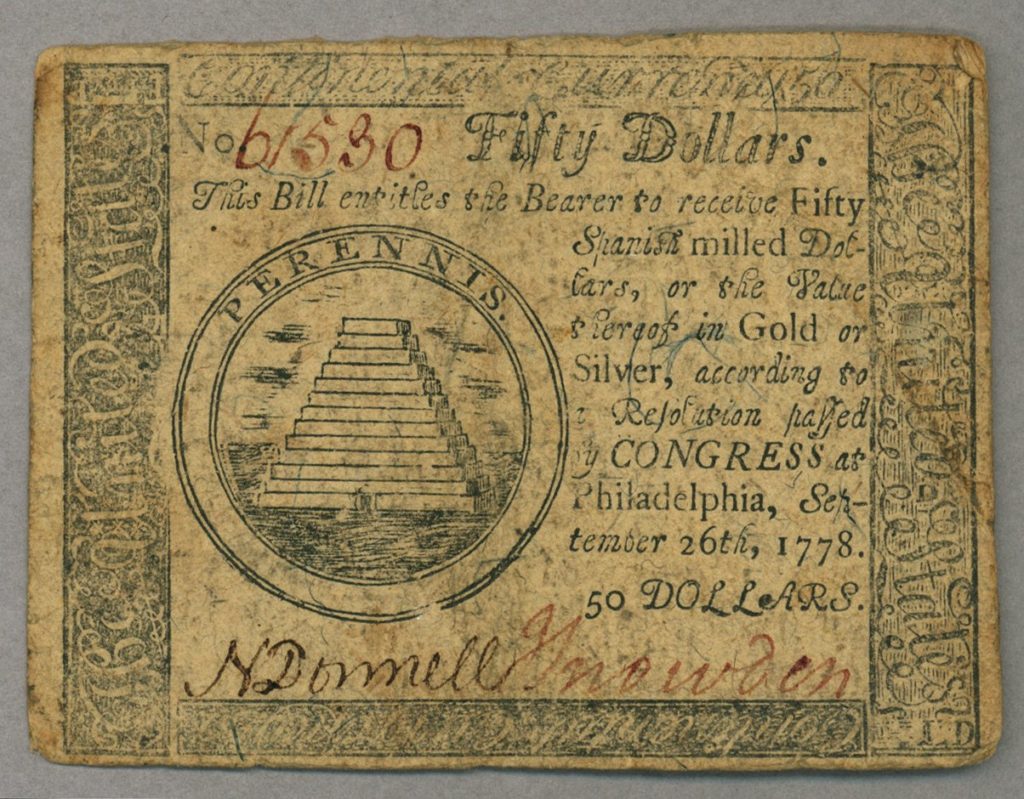

The worst inflation in U.S. history—Confederacy aside—occurred before we even had a Treasury. In November 1779, at the height of the Revolutionary War, the continental dollar reached peak inflation of 47% in a month. The definition of hyperinflation is price increases exceeding 50% per month.

The $50 note a century before President Grant. Credit: U.S. Diplomacy Center.

So the United States avoided hyperinflation, but just barely. Countries that lived through hyperinflation in recent memory wouldn’t recommend it. For example, Poland decided on “shock therapy” rather than a soft landing when that country traded in communism for a market economy in 1989. It was worth it in the long run, but one cannot simply dismiss the pain of 600% inflation. It would’ve surely been worse if the International Monetary Fund wasn’t there to provide some cushion. And of course there’s Zimbabwe, the poster child for bad monetary policy. From 2006 through 2009, the Mugabe regime continually failed to learn any lessons, and the inflation rate during that period can only be rendered in scientific notation.

So when you take a long, historic view of U.S. consumer prices, you’re left with the inescapable conclusion that we’ve basically been spoiled rotten.

Are you 59 1/2 or older?

Unlock the hidden growth potential of your 401k assets!

You now have the opportunity to do a Retirement Rollover into a personal IRA. Starting at 59 1/2 you are able to move a sizable portion of your 401k, which is called an In-Service Rollover (ISR). Break the chains of the rules within your 401k plan and have more control over your hard earned money in an IRA.

Call today, toll free, at 1-800-301-8486 to learn more about the benefits of doing an In-Service Rollover.

Provided by Smith Anglin, a Registered Investment Advisor.

US Economy

The initial read of U.S. GDP growth was revised down from 2.6% to 2.5%, suggesting that the economy is cooling down slightly faster than expected. Lending some shade to President Trump’s increasingly protectionist stance is that one of the drivers of the fall from 3%+ GDP growth over the rest of 2017 is a trade imbalance that shows the U.S. importing 1.13% more than it is exporting. The greatest negative impact, though, was a drop in inventory spending.

US Stocks

The S&P 500 steadily regained its footing after the first few trading days of February. At the lowest point of that dip, the index was down 9.5%, but ended the month down only 3.8%. As of this writing, the S&P is up almost 2% year-to-date.

The VIX index, which measures market volatility, has settled into a broad range, if not a steady state. As reflected in this month’s lead article, it is now consistent with historical norms rather than with 2017 long stretch of very low readings. This suggests that investors view equity markets with a typical dose of skepticism instead of over exuberant optimism.

Many stock watchers still maintain a favorable view of the economy but await the first wave of 1Q earnings reports before placing their bets.

International

European bourses have not bounced back as effectively as U.S. exchanges. Indexes in London, Paris and Frankfurt are down between 3% and 6% so far this year. Still, they don’t appear to be falling much further.

In Asia, the Nikkei is down more than 7% so far this year, but the Hang Seng and Shanghai indexes are right around where they started 2018.

Central Banks

Inflation fighter Jay Powell is now firmly ensconced in his new role as Federal Reserve chairman. Even he concedes, though, that his nemesis is likely to remain tame, with prices expected to rise at only around a 2% pace. Based on that, many analysts expect three or four Fed Fund rate hikes of 25 basis points each in 2018, and anticipate that pace of rate increases ticking up next year. Considering the U.S. Commerce Department’s recent report boasting 313,000 new jobs in February, the Fed will have the luxury to focus on inflation to whatever degree it impacts economic growth.

The Bank of England Governor Mark Carney has not been shy about his skepticism around cryptocurrencies. In a recent speech, he hammered home the point that the gyrating valuations of this new asset class constituted “speculative mania.” He called for greater regulation to “hold the crypto-asset ecosystem to the same standards as the rest of the financial system.”

Commodities

Oil prices are up modestly so far in 2018 and have, uncharacteristically, proved much less volatile than stock prices.

The view from 2017 was that the dollar was going to slide lower against the euro in what was expected to be a fairly boring year for currency trading. The opposite, though, has proven to be true, at least so far. The dollar is gaining on both the euro and the pound as U.S. stocks recover more quickly than their European counterparts from early February’s disruption.

Bitcoin recovered from that inflection point, then kept going. Though still far short of its $17,000 record price from January, it stuck for quite a while in a respectable range around $11,500. Daily gyrations might be nerve-wracking, but its ability to regress to a mean cannot be wished away by skeptics. Even so, recent concerns related to the platforms on which the cryptocurrency trades have brought it down below $9,000. Bear in mind, that’s still $1,700 above where it was February 5, and $5,500 above where it was a year ago.

Attention FedEx Pilots

You may not have realized that there’s something special about the FedEx 401k plan. You could be a prime candidate to utilize a special rule in your 401k, which could greatly improve your money and your retirement strategy!

The sooner you act, the sooner you could benefit so contact Smith Anglin Financial for more info at 800-301-8486.

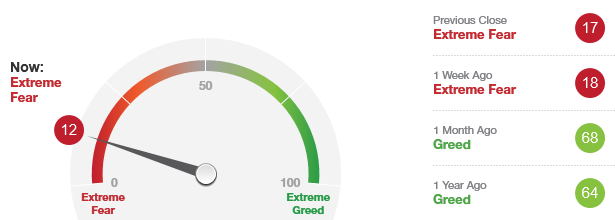

Fear & Greed Index

As of 2/28/18.

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From The Captain's Table

Emotional Rescue

Some of the most hackneyed suggestions you’ll hear from financial advisers is, “Don’t invest with emotion.” We’re going to gently push back on that notion a little.

The reasons why you invest are deeply emotional because the stakes are high. This isn’t about scorekeeping, it’s about ensuring that your loved ones—yourself included—are provided for when you aren’t generating income anymore. And it’s about taking control of deciding exactly when that day comes, rather than having it arrive unannounced. So you have our permission to be passionate about this domain of your life.

The trick, though, is to have a plan and to make sure your investments serve your passions rather than the other way around. So let’s take a look at some of the biases that often get baked into our decisions. Just being aware of them will allow you to insulate yourself against making mistakes based on them.

Number One on the bias list has to be what’s called “loss aversion”. Here’s an example: Let’s say you bought a stock at $50, and it goes down to $40. The natural inclination is to wait until it goes back up. But there are two problems with that thinking. First, what if it never does? Then you’re stuck with a loss. Second, what if it does … but it takes a long time? What if by the time it crosses that magical $50 barrier again and becomes a win, you could’ve sold your slightly-reduced holding and moved the money into a stock that was making gains fast enough to make up the difference, and then some?

That’s a major impediment to sound decision making, year in and year out. But over the course of this past year, what had been a relatively benign source of misinterpretation has become an incredibly oversized bias: “the bandwagon effect” (Number Two if you are counting along with us).

That’s what it’s called traditionally but, as Bitcoin’s price rose from the hundreds to the thousands to the tens of thousands, the bandwagon effect earned a new name: FOMO. That stands for the Fear Of Missing Out. Certainly, blockchain technology is here to stay and cryptocurrencies aren’t going away anytime soon, but the rise in Bitcoin probably has as much to do with the herd instinct and FOMO buying as anything else. Remember that momentum players eventually run out of momentum, but contrarians are almost always proven right … eventually.

Number Three and perhaps the most pernicious risk to good investing, though, is what’s called “present” bias. This is the tendency we all have to sharply discount the importance of the future when making decisions today. You could make the analogy to overeaters. Alcoholics know they need to stop drinking. Gamblers know they need to stop gambling. These vices are rooted in unnecessary activities. But we all have to eat, so it’s easy for an overeater to discount the future health effects of his gluttony when he’s really hungry right now. An overeater needs to find a healthy way of approaching food.

Similarly, the entire financial world is predicated on discounted cash flows: the notion that a dollar today is worth more than the promise of a dollar tomorrow.

That doesn’t mean tomorrow isn’t important, but our tendency to fall victim to “Present bias” leads to some of the most devastating misallocations of resources we can make. Consider this: according to one study, more than a quarter of younger workers haven’t saved any money at all for retirement. And more than one-third of all workers of all ages have set aside less than $1,000 toward retirement. Now to some degree, this is unavoidable. A lot of people simply aren’t getting paid what they’re worth. But readers of this column tend to be compensated well enough to be able to take ownership of their financial future. One good way to approach this is to make sure that you’re investing every dollar for which your company provides matching funds, and every fractional share of stock the company is offering to employees at a discount.

Ultimately, though, the best way to avoid the catastrophic results these biases can lead to—along with the other ones we didn’t have the time or space to discuss here—is to have a planning discussion with a financial adviser who can provide you with the independent, clear-eyed view that can save you from a host of tricks of the mind.

Fear and greed are some primal emotions. So is love for your family. But in its own way, sober reflection is also an emotion. Let it work for you.

Upgrade your 401k Autopilot ProgramSM with VBO!

Remove the restrictions imposed within the 401k platform fund choices and open your retirement savings to more investment opportunities.

EZTracker has taken over the USPFA newsletter and is offering subscribers an exclusive deal.

Check your email for a message titled “Important Update About Your USPFA Newsletter.”

If you didn’t get it, email info@eztracker401k.com or call 201-503-6445.