Market Overview

Since the last newsletter, the major indices have pulled back, experiencing selling pressure over the past few trading sessions. On a year-to-date basis the S&P 500 remains up 2.4%, the DJII +2.1% and the NASDAQ Composite is up 1.1%. ALL model portfolios are being rebalanced this month.

International Stocks - An Attractive Option?

The US now represents nearly 70% of the world’s equity market valuation and continues to command over 60% of global net investment flows. These trends push US valuations to higher versus the rest of the world. BUT when do valuations and growth expectation get too large?

- Valuation: The S&P 500 currently trades for 9x expected earnings, vs historic price/earnings multiple of 16.

- Persistent Inflation: Trump’s deportation of undocumented immigrants & reduction in immigrant flows could put upward pressure on wages, while higher tariffs could boost consumer prices, especially for steel and The 4.5% yield on the 10-yr US Treasury reflects market concerns that inflation could revive.

- US govt’s worsening fiscal situation: The US dollar’s reserve-currency status aside, the large deficit (6.4% of GDP) and annual interest expense > $1 trillion, concern investors, who could be spooked if there isn’t a dent in debt

All portfolios will be rebalanced this month by reducing our overweight position in the S&P and reallocating to areas where we have been underweight, particularly in international markets.

Tariffs and the expected impact on the markets

On February 4, the Trump administration imposed an additional 10% Tariff on Chinese imports, and a 25% tariff on imports from Canada and Mexico (10% on Canadian energy products). These tariffs have introduced uncertainty into the markets, with concerns about trade wars and their impact on global supply chains. Many investors are monitoring this apprehensively, as higher import costs could contribute to inflationary pressures, particularly in consumer goods, manufacturing inputs, and energy prices. Inflation concerns, combined with potential retaliatory measures from affected countries, may lead to increased market volatility. In this evolving environment, diversification and close monitoring of policy changes are recommended strategies-both of which remain key priorities for USFPA.

What happened over the last week?

US equities faced notable pressure last week as new US data sparked concern over a slowing economy and persistent inflation. Catalysts for the selloff included new economic data (fall in existing home sales, US Services Purchasing Managers’ Index’s entering contraction territory), a severe drop in the U of Michigan consumer sentiment index, and investors’ anticipating another weekend of potential policy headlines from the Trump administration.

What We’re Watching

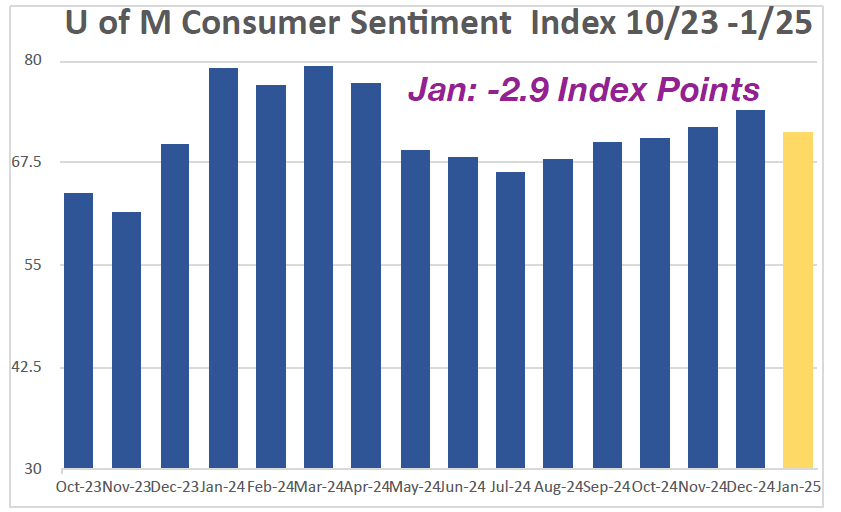

Index of Consumer Sentiment

February’s US Consumer Sentiment, as measured by the University of Michigan’s Index, fell off a cliff, sliding more than 10% to 64.7 index points from January’s 71.7. The decrease was seen across all income, age, and wealth groups. One major component was inflation expectations, which jumped from 3.3% to 4.3% (its highest reading since 2023). This increase in inflation was broad based across both short-term and long-term. While sentiment fell for both Democrats and Independents, it was unchanged for Republicans, reflecting continued disagreement on the consequences of new economic policies.

Index and Sector Analysis:

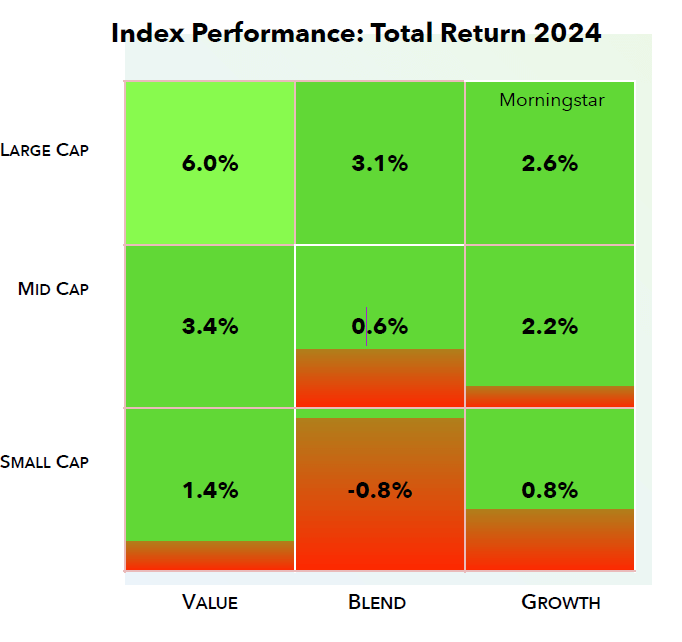

Indices: Since the last newsletter, all index quadrants (except Large Cap Value) experienced declines associated with the defensive pivot caused by the weak economic headlines over the last week. The lower-right (smaller-capitalized and growth index quadrants) were hardest hit (Small-cap Value -5.0%, Small-cap Blend -4.8% and Mid-cap Value -3.8%). Large-cap Value was the only sector that grew since the last newsletter, up 1.6%.

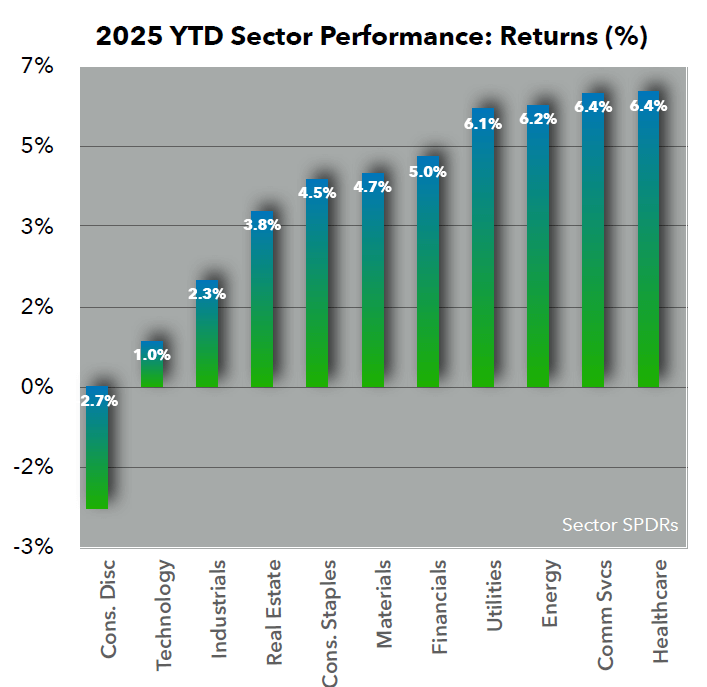

Sectors: The defensive pivot of last week’s selloff hit cyclical sectors hard and caused a re-ordering of the top-performers. Defensive sector Consumer Staples (the worst-performing sector in January) ended up almost 6% in February as a result. Communications Services (+4.83% one-month return) and Healthcare (+2.76%, a defensive sector) were also February leaders. The two biggest laggards in over the last month are Consumer Discretionary (-5.42%, a very cyclical sector) and Industrials (-4.08%, similarly cyclical).

Fixed Income Market Update – February 2025

In February 2025, the domestic fixed income markets have been influenced by evolving economic policies and shifting investor sentiment.

Monetary Policy and Interest Rates: The Federal Reserve maintained the federal funds rate at 4.25% to 4.50% during its January meeting, following a series of rate cuts totaling 100 basis points in late 2024. This decision reflects the Fed's cautious approach amid persistent inflation concerns and policy uncertainties.

Treasury Yield Movements: In response to the Fed's stance and market dynamics, Treasury yields have adjusted accordingly. The 2-year yield decreased by 6 basis points, closing at 4.202%, while the 10-year yield declined by 19 basis points to 4.43%. This narrowing spread suggests a modest steepening of the yield curve, potentially indicating tempered investor expectations for future economic growth.

In Summary

Bonds are expected to play an important role in portfolios in 2025. With bond yields looking appealing, they provide a favorable alternative when equity valuations and credit spreads are less attractive. Unlike cash, bonds have the potential for capital appreciation as policy rates decrease, which can help enhance their role as a stabilizer and diversifier alongside equity investments in portfolios. The fixed income landscape in February 2025 is navigating a complex array of policy decisions, inflation dynamics, and global economic factors. USPFA recommends staying informed and maintaining a diversified approach to navigate potential risks while identifying opportunities in the bond market.

Corporate Earnings

During the fourth quarter of 2024, domestic companies with businesses that focused on the international markets (5.9% Q4 sales growth and 21% Q4 earnings growth) outperformed companies who are inwardly-focused and had less international exposure (5.0% Q4 sales growth and 14.5% Q4 earnings growth). For example, NVIDIA has tons of international exposure, and its outperformance has helped in that respect. Domestic investors on the whole expect this trend to reverse in 2025.

As mentioned earlier, the recent economic and inflationary data showing slower growth caused a pivot away from cyclical and growth sectors and names such as NVIDIA (NVDA), Palantir (PLTR), Apple (AAPL), Meta (META) and Tesla (TSLA). Defensive names such as Consumer Staples P&G (PG) General Mills (GIS), Kraft Heinz (KHC) all advanced materially last week. Consumer Staples, Utilities and Healthcare all benefited.