Months into the budget battle – we used to say “budget process” – America is still waiting for a final bill that can pass both houses of Congress.

The less partisan – we used to say “bi-partisan” – $1.2 trillion hard infrastructure plan is now law. But then there’s the reconciliation bill – House Resolution 5376, which Democrats call "the Build Back Better Act." It would provide free community college education, paid parental leave, affordable preschool childcare, and other provisions that amount to "soft infrastructure." As of this brief moment, its price tag hovers just below $2 trillion over 10 years. (Before we start panicking, we need to realize that the federal government would be spending close to $15 billion even without the act’s new programs.)

While it seems likely that all these provisions will be paid for, the question remains: How? There are two possible ways: more taxes or more debt. In the current case, more taxes are almost a certainty.

The problem is, we still don’t know which taxes will go up and by how much. But a lot of ideas are on the table, a number of which could directly affect your retirement savings.

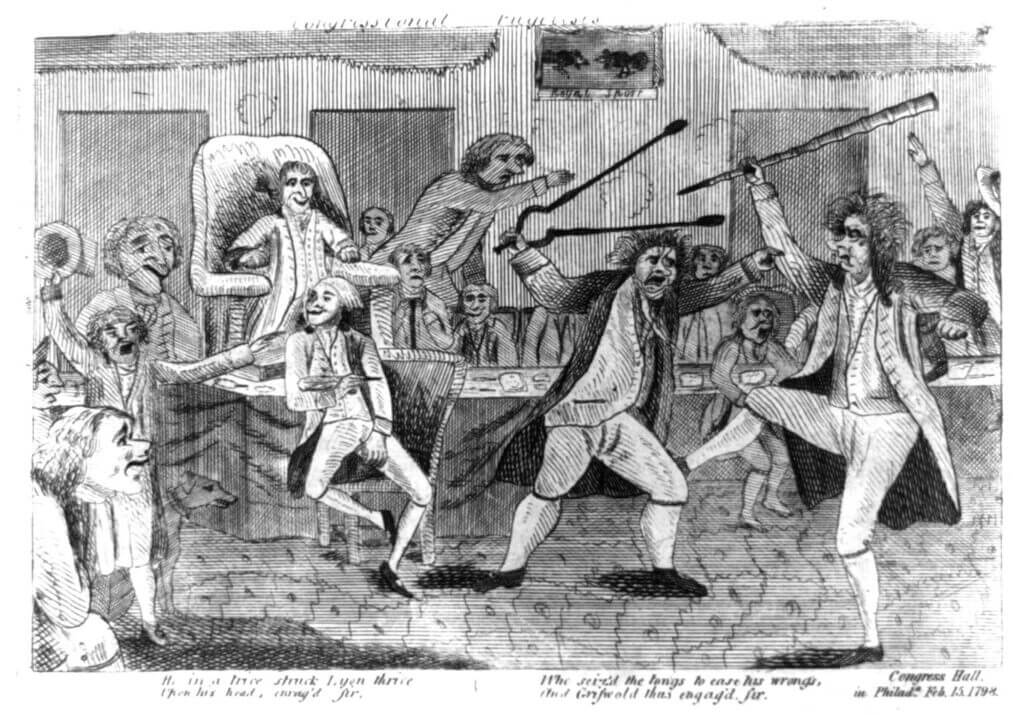

Could the battle over the budget get worse? Yes. Much. Vermont’s Matthew Lyon and Connecticut’s Roger Griswold scuffled in 1798. Griswold called Lyon a “scoundrel”. So Lyon spit in Griswold’s face. One thing led to another. Now imagine how these two would react in the current climate. Credit: Library of Congress

Tax brackets and capital gains

The most obvious and immediate impact would be on the tax rates of high earners. Individuals earning $400,000 per year or couples earning $450,000 would see their marginal rate rise from 37% to 39.6%. While that’s an increase over the 2017 rate pushed through by the Trump administration, it’s neither a big jump nor a historically high rate. And it wouldn’t take effect until the Tax Cuts and Jobs Act expired in 2026.

Still, the capital gains rate – currently 15%-ish – would go up to 25% for earners in that sub-half-a-million-dollar-a-year category. But those at the tippy-top should prepare for a soaking.

“Under the new Build Back Better framework, the United States would tax capital gains at the third-highest top marginal rate among rich nations, averaging nearly 37 percent,” according to The Tax Foundation, which points out that there would be an 8% surcharge on all taxes paid by those with modified adjusted gross incomes exceeding $25 million, and that applies to their capital gains as well as their earned income.

In Washington, nothing is agreed to until everything is agreed to. So even though you may have read that the so-called “billionaires’ tax” is dead on arrival, don’t be so sure.

The interesting thing about the proposal isn’t that it’s levied against the ultra-rich, it’s that it doesn’t tax income. It taxes unrealized capital gains. In other words, if your net worth takes three commas to express numerically, then you’re not taxed on how much money lands in your checking account by year’s end; instead, you’re taxed on how much money could have. For example, if you founded a company that last year was worth $10 billion and you still own 10% then your stake was worth $1 billion. Let’s say business was good and it’s now a $12 billion business and your stake is worth $1.2 billion. The billionaires’ tax would treat that $200 million increase in your net worth as if it were any other capital gain. That is, you’d have to pay 23.8% tax on it.

This should bother you even on the off chance you’re not worth a billion dollars. That’s because it’s unconstitutional to tax unrealized gains. Still, it’s possible the courts could rule that unrealized gains are actually income and thus legal to tax under the authority of the Sixteenth Amendment. And in the more likely event that the courts rule in the billionaires’ favor, let’s remember that, prior to the 1909 passage of that amendment, an income tax was illegal. There’s no reason why a Twenty-eighth Amendment couldn’t legalize an unrealized gain tax.

If that were to happen, then any wealth you as a non-billionaire acquire could be taxed in the year you make it.

Retirement accounts

The current version of H.R. 5376 introduces provisions limiting what you can do with ERISA-qualified retirement plans. If you earn at least $400,000 or you and your joint filer earn at least $450,000, you’ll face a $10 million cap on your retirement savings. If you exceed that, you’re required to take a distribution of at least 50%. If you're above that income threshold and your plan exceeds $20 million, you must withdraw from 401(k) plans and Roth IRAs first.

H.R. 5376 also eliminates “backdoor” and “mega-backdoor” Roth IRAs. At the moment, these allow people to open and sock away money in Roths even if they exceed the income limitations.

It gets even more challenging if you hold a self-directed IRA. You’ll no longer be able to keep anything in it that you have to be an accredited investor to trade in. If you do, the account stops being an IRA, and you lose all your tax advantages.

The bill goes on to specify that an IRA holder can’t invest in a business if

its securities are not exchange-traded,

the IRA holder is an officer of the business or can exercise control through some other means, or

the IRA holder holds more than 10% of the voting or economic stock, down from the current 50%.

Next steps: Theirs and yours

None of these provisions of the Build Back Better Act would take effect until 2023, so you’d have until the end of 2022 to make whatever moves you need to make.

As for what those might be, we won’t know until the president signs it into law. At that point, it’ll be up to the Internal Revenue Service to write the rules which fill in the gaps and make it operational.

Once the dust settles, you might want to have a detailed discussion with your trusted financial professional, and your tax advisor.

Gross domestic product growth slowed to a 2.0% annual rate in the second quarter, according to the first estimate released by the Bureau of Economic Analysis. That’s down from the second quarter’s 6.7% expansion. The deceleration was accounted for by a slowdown in personal spending on motor vehicles, food services and accommodations. While the latter two were likely dialed down by lower demand due to the spike in Covid-19’s delta variant, the first was probably caused by supply disruptions.

Total nonfarm payroll employment rose by 531,000 in October, and the unemployment rate edged down by 0.2 percentage point to 4.6%, the U.S. Bureau of Labor Statistics reported. Job growth was widespread, with notable job gains in leisure and hospitality, in professional and business services, in manufacturing, and in transportation and warehousing. Employment in public education declined over the month.

Initial jobless claims for the week ending October 28 came to 281,000, the lowest level since immediately before the pandemic and a 10,000 week-over-week decrease. The four-week moving average was 299,250, a decrease of 20,750 from the previous week's unrevised average.

The Consumer Price Index for All Urban Consumers spiked 0.9% in October on a seasonally adjusted basis after rising 0.4% in September, the Labor Department reported. Over the last 12 months, the all-items index increased 6.2% before seasonal adjustment. While inflation was broad-based, it was clearly led by energy costs, which are volatile and considered non-core. The energy index increased 4.8%, with the gasoline index rising 6.1%.

US Stocks

The S&P 500 returned to its winning ways, gaining +7.0% in October on a total return basis. The CBOE VIX “fear gauge” likewise dropped to a benign 16.26 level, closing 29.7% lower, suggesting a surge of confidence in equity markets.

International

In Europe, Amsterdam’s Euronext 100, Frankfurt’s DAX and London’s FTSE 100 improved +5.3%, +2.9%, and +2.1% respectively, in October. In Asia, Hong Kong’s Hang Seng joined its European peers by gaining +3.3%, but Shanghai’s SSE Composite and Tokyo’s Nikkei 225 were down -0.6% and -1.9% respectively.

Central Banks

The Federal Reserve plans to continue buying Treasury and mortgage-backed securities but will incrementally reduce the monthly volume of these purchases. By lifting its foot off the gas but declining to step on the brake, the Fed is looking for “smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses.”

Also the Fed put out a statement in support of the goals of the recent COP26 climate talks, expressing “appreciat[ion for] the magnitude of the challenges ahead of us” and expressing “commit[ment] to do our part.” The U.S. monetary authority coordinates with a network of other central banks dedicated to “greening the financial system”. Still, the Fed offered no concrete policies specific to any proposals coming out of Glasgow.

Commodities

Oil prices continued to gain in October, with West Texas Intermediate crude gaining +11.4% to end the month at $83.57 per barrel. Meantime, inflation hedge gold rose +1.5%, to end the month at $1,783.90 per ounce.

The dollar improved +0.2% against the euro and +2.6% against the yen, but slid -1.6% against the pound.

Cryptocurrency roared back spectacularly in October, with Bitcoin leaping +42.5% to end the month at $62,533.38.

The USPFA Team

wishes you a

Happy Thanksgiving!

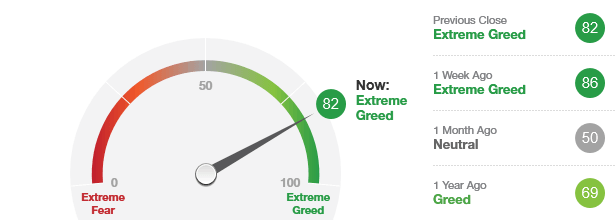

Fear & Greed Index

As of 11/16/21.

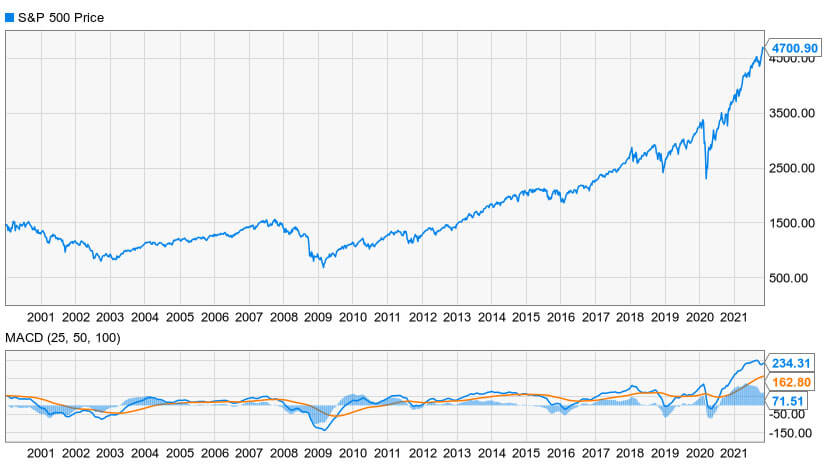

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

When investors freak out

The price of gold jumped from $650 in 2007 to $1,900 in 2011. Then, on one September day, the price for this inflation hedge dipped 6%. It then kept dropping as panicky investors tried to dump it as fast as they could. There was no real reason to fret, though. It hit a support level around $1,100 and now trades back in that $1,900 range.

So why the irrational behavior? Is it just that “gold bugs,” as New York University economist Nouriel Roubini calls them, are “a combination of paranoid investors and others with a fear-based political agenda [who] were happily predicting gold prices going to $2,000, $3,000, and even to $5,000”?

While that’s partially true, that would only explain why it happened in the precious metals space. But it has happened in everything from real estate to stocks to mortgage default swaps to tulips.

“Despite standard investment advice to the contrary, individuals often engage in panic selling, liquidating significant portions of their risky assets in response to large losses,” according to findings from a team at the Massachusetts Institute of Technology. “We find that a disproportionate number of households make panic sales when there are sharp market downturns, a phenomenon we call ‘freaking out’.”

Trigger warnings

Freaking out, by definition, suggests that the perceived problem in the market is not as bad as the out-freaker thinks. Still, freaking out itself is a major problem and leads to significant dissolution of a household’s wealth.

The MIT team defines freaking out as a decline of at least 90% of a household account’s equity assets in less than a month, of which 50% or more is due to trades.

There’s also evidence to suggest – our assertion, not MIT’s – that freaking out follows the same pattern as the Dunning-Kruger effect, which demonstrates how low-skilled people overestimate their skill while high-skilled people underestimate their own.

"[T]he miscalibration of the incompetent stems from an error about the self, whereas the miscalibration of the highly competent stems from an error about others," according to David Dunning and Justin Kruger, the psychologists who identified the phenomenon in 1999.

But back to freaking out.

“Investors who … self-identify as having excellent investment experience or knowledge tend to freak out with greater frequency,” according to the MIT paper.

It doesn’t take much to trigger the response. It could be rooted in the assumption that the price of an asset that’s going up now will continue to trend up. It happens in real estate all the time. At the lowest point of the 2008 financial crisis, there were 11,000 homes in foreclosure in Cape Coral, Fla. You could’ve bought with a credit card. The same thing happened in Dubai, United Arab Emirates, just a few months later for pretty much the same reason. It looks like it’s happening in China now.

This is what happens when speculation gets too far ahead and economic instability sets in. With economic instability often comes political instability, and that can also lead to panic.

Misbehavior

This all falls under the aegis of behavioral economics, the study of how emotional and cognitive factors effect financial decisions. Behavioral economics sits at the corner of the rational, data-driven world of finance and the messy, confused world of the human beings to whom the implementation falls.

Oddly enough, the scientific study of behavioral economics is older than that of economics itself. They both go back to Scottish academic Adam Smith, whose The Wealth of Nations is considered the cornerstone of all subsequent economic thought. He published that treatise in 1776, but his similarly groundbreaking essay, The Theory of Moral Sentiments, went to press in 1759.

“The thought of their own safety, the thought that they themselves are not really the sufferers, continually intrudes itself upon [people]; and though it does not hinder them from conceiving a passion somewhat analogous to what is felt by the sufferer, hinders them from conceiving any thing that approaches to the same degree of violence,” Smith wrote.

Sadly, not all Enlightenment writers had the same knack of getting to the point as did Thomas Paine, but the gist is this: While individuals might truly have empathy for someone else, they’ll take care of their own needs first. And if, in their own minds, that means dumping their shares before you get a chance to dump yours, then that’s what they’ll do regardless of whether or not it makes objective sense.

While we can’t recommend Smith’s collective works to you, we’re fortunate to have a contemporary economist who makes the case more clearly. Nobel laureate Richard Thaler (pronounced “taller”) was among the founders of the modern field of behavioral economics. In the late 1970s, Thaler and his colleagues first identified the endowment effect, which suggests that people prefer to value an object they own in excess of what they’d have to pay to acquire it. This led to many other academic rabbit holes:

People seek a quick, satisfactory solution rather than invest time and mental energy in finding an optimal one.

People are more eager to avoid a loss than to realize a gain of the same value.

Positive reinforcement works better as a behavior influencer than education, legislation or enforcement.

Have you ever freaked out? Would you ever? Are you the best judge of how to answer these questions?

This is where having a trusted financial advisor comes in handy. We all have biases. We all have blind spots. Sometimes it helps just to have a dispassionate person take an objective look at your financial decisions.

The hardest thing investors need to figure out, it seems, is their own selves.

-Chris

Chris Lott, CFP®, CPA

Financial Partner and Wealth Advisor

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.