This month's models have been posted. There were CHANGES in ALL the MODELS (highlighted in YELLOW). The rest of the newsletter will be posted by mid-month.

The New World’s new world

Every 10 years, the U.S. Census Bureau counts America’s heads. And while the press fixates on how the results will change the boundaries of electoral districts, that’s not the Census’s only or even main purpose. The Census Bureau’s objective is to take a snapshot of what America looks like, and that is constantly changing.

The changes are broad-based. Age, ethnicity, race and national origin are moving targets. So are expectations about education, income and living arrangements. These changes are well underway. Whether they are good or bad is a value judgment far outside the scope of this article. But people’s reactions to them are often quite heated just the same.

The next Americans

So, who is the typical American now? And who will it be when the 2060 Census rolls around?

As of the 2020 census, the average American is a 38-year-old, native-born, non-Hispanic White female. She is a high school graduate who owns her own $217,500 home, which she shares with one or two other people. Her job with one of the nation’s 27.6 million employers pays $34,103 per year but, with her husband of 10 years also working, they make a total of $62,843. Odds are two out of three that they’ll stay married the rest of their lives.

But the country is changing, as it always has.

First of all, America is getting grayer. By 2060, the mean age will have advanced from 38 to 43. The fastest-growing age group over that period is likely to be centenarians; those 100 years of age or older are expected to increase by 618%. Meantime, those of traditional working age – 18 to 64 – are expected to grow by only around 15%.

By 2035 there will, for the first time, be more Americans over 65 than under 18. And, as America ages, we will have fewer children. At that point, immigration will become the main source of population increase as more people will become Americans via swearing-in ceremonies than as newborn arrivals in maternity wards. Even so, the country’s foreign-born population isn’t likely to exceed 20% for the foreseeable future. Canada, Australia and New Zealand all exceed that threshold now.

As naturalization overcomes birthright citizenship, we can expect a shift in ethnicity. Between now and 2060, the number of non-Hispanic White Americans is expected to decrease in real terms, from 199 million now to 179 million – continuing a trend first realized in 1970 – while the number of White Americans without reference to heritage should increase from 253 million today to 275 million 40 years hence. The total population is projected to grow from 332.6 million as of the 2020 Census to more than 400 million in 2060 so, although non-Hispanic White will still be the largest ethnic group in America, that group will be a plurality rather than a majority. Hispanic Americans without reference to race will comprise 27.5% of America by 2060, and will almost double the number of Blacks living in the U.S. By the time the 2022 election rolls around, Pew Research reports that Hispanics will outnumber Blacks at the voting booth.

And yet race is likely to matter less and less to both the people being counted and the people doing the counting. The fastest-growing ethnic group right now is “Two or More Races” (capitalized here because that’s how the Census Bureau categorizes that demographic). While multi-race Americans are expected to triple in number by 2060, they are projected to account for only 6.2% of the population.

The family unit might be revealed to be as much a societal construct as race is.

“A growing share of parents are unmarried,” Pew reports. “Among parents living with a child, the share who are unmarried increased from 7% in 1968 to 25% in 2017. Part of this increase is due to a growing share of unmarried parents cohabiting, as 35% of unmarried parents were in 2017. Over the same period, the share of U.S. children living with an unmarried parent more than doubled, from 13% in 1968 to 32% in 2017.”

Michelle Rodriguez – Letty from the Fast & Furious movies. She’s a 43-year-old, American-born Hispanic woman, just like the average U.S. citizen will be in 2060. If you have a problem with that, take it up with Vin Diesel. Credit: Universal Studios

“When asked about projections by the U.S. Census Bureau that a majority of the U.S. population will be nonwhite by the year 2050, about half of Americans say this shift will lead to more conflicts between racial and ethnic groups,” according to Pew. “And about four-in-ten predict that a majority nonwhite population will weaken American customs and values, larger than the shares who say it will strengthen them (30%) or will not have much of an impact (31%).”

Even so, Americans are tolerant of interracial marriage. Almost half say it’s a good thing and only one in 10 say it’s a bad one. Interestingly, results were consistent whether the respondents were Black, White or Asian and without reference to Hispanic heritage.

What they should focus on instead

Perhaps all this fascination with ethnicity and national origin misses the point, though.

Let’s set aside issues of history’s uneven playing field that advantaged some groups over others in the quest for generational wealth. From a strictly empirical perspective, Black, White and Brown don’t matter. Gray does. The proportion of working-age Americans to retirement-age Americans shrinking – and not slowly, and not by a little. Right now, one-third of Americans are supporting the other two-thirds, most of whom are children but many of whom are seniors. By 2060, one-fourth of Americans will be supporting the other three-fourths, and a majority of those dependents will be retirees.

Maybe that’ll be you. Maybe that’ll be your children. Maybe, long, comfortable retirements will be a thing of the past by then and you or your children will have to work longer than you ever expected.

It’s not enough for our generation to save for retirement. We need to save retirement. It’s a daunting challenge, so please talk with your financial advisor about how you can help keep the whole concept of the Golden Years alive, at least in your own family.

Gross domestic product grew at a 6.7% annual rate in the second quarter, slightly faster than either the original or revised pace, according to the final estimate released by the Bureau of Economic Analysis. The update reflects upward revisions to personal consumption and net exports.

Initial jobless claims for the week ending October 2 came to 326,000, a 38,000 week-over-week decrease as the covid-19 delta variant appeared to start burning out. The four-week moving average was 344,000, an increase of 3,500 from the previous week's unrevised average.

The seasonally adjusted unemployment rate was 2.0% for the week ending September 25, a decrease of 0.1 percentage point from the previous week. The advance number for seasonally adjusted unemployment was 2,714,000, a decrease of 97,000 from the previous week. This is the lowest level for unemployment since immediately before the pandemic shutdown in March 2020.

The Consumer Price Index for All Urban Consumers increased 0.4% in September on a seasonally adjusted basis after rising 0.3% in July, the Labor Department reported. Over the last 12 months, the all-items index increased 5.4% before seasonal adjustment. The index for food rose 0.9 percent, with the index for food at home increasing 1.2%. The energy index increased 1.3%, with the gasoline index rising 1.2%.

US Stocks

The S&P 500 reversed course with a -4.7% loss in September, ending a seven-month winning streak. The CBOE VIX “fear gauge” surged as a result, closing 40.4% higher at 23.14, suggesting a loss of confidence in equity markets, though investors do not appear to be panicky.

International

In Europe, Amsterdam’s Euronext 100, Frankfurt’s DAX and London’s FTSE 100 dipped -2.5%, -3.7% and -0.5%respectively in September. In Asia, Hong Kong’s Hang Seng joined its European peers by sinking -5.0%, but Shanghai’s SSE Composite and Tokyo’s Nikkei 225 were up +0.7% and +4.9% respectively.

Central Banks

Libertarians never had enough power to push their “end the Fed” position, but now the central bank is getting it from all sides.

Senior Federal Reserve officials have been caught with their alleged hands in the figurative till, and senators in both Republican and Democratic mainstreams want a full investigation. Meantime, the White House is trial-ballooning the elevation of liberal-leaning Fed board member Lael Brainard to the chair now held by Jerome Powell, a move opposed by senior Republicans.

In an upcoming confirmation hearing, you can expect senators to bring up a) that the Fed is the fourth central bank in American history and, for 76 years from 1836 to 1913, the republic managed to survive without one, and b) whether monetary policy will still be if cryptocurrency continues to grow at the pace it has over the past dozen years.

Commodities

Oil prices returned to form in September, with West Texas Intermediate crude gaining +9.5% to end the month at $75.03 per barrel, eliminating August’s swoon. Meantime, inflation hedge gold ticked down -3.4%, to end the month at $1,757.00 per ounce.

The dollar improved across the board for the third month in a row, reclaiming +1.9% against the euro, +2.1% against the pound in June, and +1.0% against the yen.

Cryptocurrency took a pause in September, with Bitcoin dipping -7.3%, to end the month at $43,869.28.

Is Your Card Up To Date?

Is your credit card about to expire? Have you recently received a new card? It’s easy to update your CREDIT CARD information. Just call us at 717-569-8162, or go to the Update Credit Card Information section under the Member’s Tab.

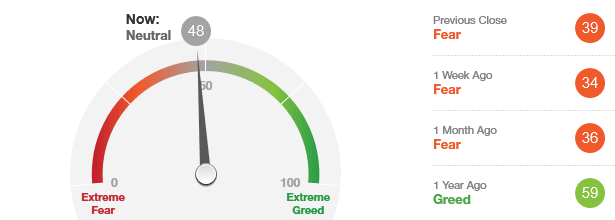

Fear & Greed Index

As of 10/15/21.

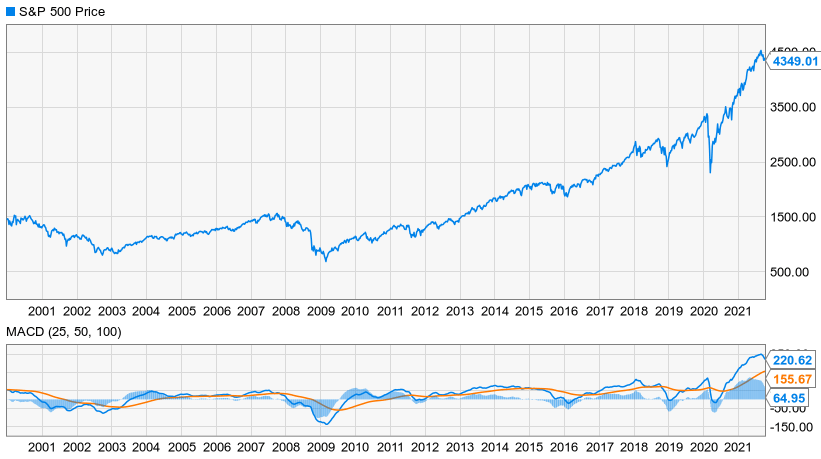

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

‘Sandwich Generation’ needs bread

If you’re at or approaching retirement age, today you live in a different reality than the one you were born into. When you came into this world, there was a concept of someday “becoming a burden to my children,” but it was only a remote possibility. Life expectancy was shorter, and thus was the time adult offspring would have to devote to being eldercare givers.

Also, a single income was enough to provide for a family, so one spouse – the wife, inevitably – would be in position to take on the chore. It helped that she expected this would be part of her life cycle and could rely on her daughter or daughter-in-law to care for her and her husband. Because her children came along while she was still in her 20s, they were fully grown and independent by the time caring for elderly family members became a necessity.

Which brings us to one more bit of nostalgia: Once upon a time, young adults couldn’t wait to get out of the house, launch their careers, and start their own families.

That whole armada has sailed. A baby born today can expect 79 trips around the sun – that’s nine more than those of us of grandma/grandpa age – and we get 10 more than our own nanas and pappies did. Today, almost 60% of married couples with children have dual incomes. One consequence of two careers is that child rearing is delayed, often by about a decade. Lastly – and the covid-19 pandemic gets some but by no means all of the blame for this – a majority of young adult Americans live with their parents. This last phenomenon hasn’t occurred since the Great Depression of the 1930s.

Welcome to the Sandwich Generation – those in middle age who must care for not only their aging parents but also their age-defying children. The term, though, is a little dated. Social workers first observed the Sandwich Generation 40 years ago. The people they were describing – women in their 30s and 40s – are themselves the elders now. And the adult offspring who care for them have their own children at home.

So, the sandwich has gotten bigger. It’s not just people in their 30s and 40s caring for parents and young children. Now there are many in their 50s and 60s caring for parents, children and even grandchildren. Gerontologists call this a “club sandwich”.

Looks great, as long as you’re not the turkey. Credit: Food Network

So, the challenge becomes: How does a late middle-aged couple provide for themselves and three other generations?

Ingredients

“Nearly half of adults in their 40s and 50s are caring for a parent who is 65 or older while also raising or supporting children,” according to three Fiduciary Trust Co. lawyers writing in WealthManagement.com. “To navigate this phase of life, one of the most important steps is to make sure [you have] a comprehensive financial plan in place.”

The website for financial advisors offers this stepwise advice:

Get organized. List all your assets and liabilities in a net worth statement, then track your income and expenses to arrive at the gap between how much you’re saving and how much you need to save. While this is good advice for anyone, those in the Sandwich Generation also need to parse out income and expenses from parents and adult children to understand the level of support you’re giving them.

Reset emergency fund.The more people in your household, the more likely an emergency will occur in any given year. That means you’ll need more in the way of liquid reserves.

Don’t neglect opportunities.We know you’re exhausted physically and emotionally, but unless you want to also be exhausted financially, make sure you’re doing the commonsense things to take care of your own fiscal health. Refinance that debt. Rebalance that 401(k). Take advantage of available tax shields.

Plan for the needs of children. We won’t go into detail about all the different vehicles created to pass wealth on to children. We did cover it here.

Take inventory of parents’ financial lives.Mom and Dad aren’t going to like this but, if they’re under your care, you need to know at least some of their financial details. As long as they’re healthy, you can respect their privacy. If and when they can no longer attend to their own affairs, they need to understand you’ll have to step up and have a plan in place to do that. Have them introduce you to their accountant at the very least, who could then advise you regarding health benefits, power of attorney and elements of financial eldercare.

Don’t forget the greens

While we agree with what WealthManagement.com has to say on the subject, they do miss one important element: that bottom slice. What about your children?

It might be uncomfortable, but it might be a good idea to discuss you finances with the kids. Otherwise, they might develop expectations around the First National Bank of Mom and Dad that simply aren’t realistic. Not everyone can pay for all college expenses, a car as a graduation present, the down payment on a house and all those other things that some of their friends might be getting from their parents.

Maybe you intended to throw your daughter a Downton Abbey-themed wedding, but then you were surprised by the sudden addition of a parent with persistent health issues to your household. You can’t do it anymore. What do you tell her?

You never know how much your children can do to support themselves until you make it clear to them that they have to try.

Garnish

Maybe you, as a Sandwich Generation member, have to bring home the bacon. And the cheese. And the tuna, lettuce, tomatoes and coleslaw.

But you don’t necessarily have to provide all the bread. Your parents very likely have some passive income and some assets they can sell if need be. If your kids are still at home, that suggests that perhaps they’re not making all they expected to, but they’re still making something and it need not all be spending money.

Your financial advisor can help you ensure that your parents live comfortably, you reach your own financial goals, and your accumulated wealth finds its way to the next generation. But taking those first steps toward providing for your multigenerational family is on you. As long as you can, build your sandwich on a foundation of artisanal seven-grain brioche.

Otherwise, you might be toast.

-Steve

Steve Anglin, CPA

Managing Partner

Steve Anglin, CPA is a Managing Partner at Smith Anglin Financial, and the Head of the Tax Preparation Services. He is also responsible for Smith Anglin’s compliance supervision. He holds a BBA in Accounting and a BBA in Real Estate, and numerous securities licenses and designations.

×

USPFA is Now Part of EZTracker 401k

EZTracker has taken over the USPFA newsletter and is offering subscribers an exclusive deal.

Check your email for a message titled “Important Update About Your USPFA Newsletter.”

If you didn’t get it, email info@eztracker401k.com or call 201-503-6445.