There are changes in EVERY MODEL. The new funds are in YELLOW. The rest of the newsletter will be published by mid-month.

Are we already in a recession?

The sad truth about recessions is that you could already be in one and not know it.

The most commonly agreed-upon definition of a recession is two consecutive readings of negative growth of a country’s gross domestic product. Considering that these readings are conducted quarterly, the economy could have been contracting for quite a while before it becomes “official.”

You don’t have to go back too far in history to see the perfect example. On December 1, 2008, the National Bureau of Economic Research – the non-profit institution which serves as the arbiter of such things in the U.S. – declared that the country was in a recession. It noted that the recession began in December 2007, a full year earlier. You’d think that the doubling of the unemployment rate, the bankruptcies of Bear Stearns and Lehman Brothers, the near-nationalization of the auto industry and the 40% drop in the Dow Jones Industrial Average would’ve provided some kind of heads-up.

But two straight quarters of shrinking GDP isn’t the only definition of recession. Maybe, by some other measure, we have already passed the cusp into a new – and less benign – economic era.

Maybe so

GDP is a less-than-perfect indicator of how the average person experiences the economy. As noted below in the market overview, the most recently ended quarter’s GDP reading was adjusted down because of slow exports and a bump in inventories, neither of which is going to make too many families cancel vacation plans.

Most people don’t feel a recessionary experience until they or people close to them are out of work. If there is an early-warning system for that, it’s hiring freezes. Companies tend to stop building staff well before they start cutting it. So far, that hasn’t been happening in a significant way. American firms added 130,000 new jobs in August – lower than expected, but still not a bad read. By almost every metric the Labor Department can throw at the count – employment-to-population ratio, unemployment rate, individuals not in the labor force – the numbers just keep getting better.

The key word is “almost.” There are some dark clouds. The number of people who can only find part-time work is growing, as are the number of discouraged workers leaving the work force. But the most interesting tea leaves to read have to do with workers’ reasons for unemployment. More people are losing their jobs and fewer people are leaving them.

Ironically, Uber – the company that practically invented the gig economy – is the only major private-sector employer that recently announced a hiring freeze. If more follow, that would be a recessionary signal.

LinkedIn, 1930s-style. Credit: Virginia Commonwealth University

It’s also important to note that there’s no such thing as “the” economy. The U.S. is a well-developed nation in terms of its financial health and it has many interdependent but distinct components: manufacturing, services, finance, farming, the public sector. Taken together, it all looks fairly healthy today, but a closer look reveals that not everyone is experiencing the current expansion equally.

It’s easy to forget that manufacturing is not doing particularly well at the moment. Factory output dropped 1.2% in the second quarter, according to the Federal Reserve, following a 1.9% drop in the first quarter, as capacity utilization languishes below 78%. Fed Chairman Jay Powell cited this – credibly or not, considering the politics involved – as the reason for the recent Fed funds rate cut, and MarketWatch quotes one leading economist as saying the manufacturing sector is in de facto recession.

Maybe not

First, let’s get one thing out of the way: The yield curve inversion you’ve read so much about – including here – is not an accurate predictor that a recession is imminent. A Bankrate.com analyst told Forbes that there’s generally a two-year lag from flash to bang.

To restate, hopefully for the last time, an inverted yield curve “suggests that investors favor short-term rather than long-term investments, indicating a likely lack of confidence that the economy will keep growing at the present pace.” That was written in April about an event that occurred in March. Half a year later, GDP is still gaining.

But the yield on the 10-year Treasury note dipped below that of the 2-year again in August and once more people got a little skittish. After all, a yield curve inversion has presaged every U.S. recession since 1955.

That said, yield curve inversions are not all created equal. It’s a matter of longevity and it’s a matter of degree. The March 2019 inversion was essentially a blip. The one last month didn’t last much longer. As of this writing shortly after Labor Day, the 10-year note is once again offering a higher yield than its shorter-term counterpart.

Also, let’s not forget that there are more Treasury instruments than just the 10- and 2-year notes. Those are just the arbitrary “benchmarks,” and that’s not even the comparison the Federal Reserve looks at; the central bank pays far more attention to the spread between the 10-year note and the three-month bond. Foreign exchange traders prefer to contrast the 10-year note yield with the Fed funds rate. But however you slice it, no two points indicate a trend. Of course, once the 3-month – or for that matter the 1-month – bill’s yield is higher than the 30-year bond’s, then the time for panic has already come and gone. Somewhere along the path to that nightmare scenario is the right moment to switch to playing defense.

Also, let’s remember that the worst inversion of this past half year was a negative 5-basis point spread between the 10- and 2-year bonds. That might have been the worst since 2007, but it’s hardly the worst of all time. In the “stagflation” days of the 1979 recession it dropped to the 200-basis point neighborhood.

Former Fed chair Janet Yellen, for one, has stated that there might be more noise than signal coming out of this warning beacon.

“On this occasion, it might be a less good signal,” she told Fox Business News. “There are a number of factors beyond market expectations about the future path of interest rates that are pushing down long-term yields.”

She has a point. Just because every recession in living memory was preceded by an inverted yield curve, that doesn’t mean that every inverted yield curve in living memory preceded a recession. Yield curves inverted in 1966 and again in 1998, and the good times kept rolling. Thus, this indicator has accurately predicted five of the last seven recessions.

But that Bankrate.com analyst, Greg McBride, had one more thing to tell Forbes: “The most dangerous words in finance are ‘it’s different this time.’”

Rescue a Pilot Month

During this month, refer a pilot and get a reward!

Here’s how it works:

For every pilot you refer who becomes a NEW member in September, we will give you and them a free month of membership! Everyone wins!

Pilots, don’t let your fellow pilots worry about their investments!

US Economy

For the second consecutive quarter, the Commerce Department’s second read of gross domestic product revised the initial estimate downward. While still not signaling a recession, the latest figure indicates that U.S. growth slowed to +2.0% growth in the second quarter compared to the first quarter’s 3.1% growth. The initial reading for 2Q was 2.1%.

The revision reflects a good news-bad news dichotomy. On the one hand, the domestic economy saw the strongest growth in consumer spending in more than four years. On the other, exports declined and inventories built up, presumably in response to or anticipation of escalating trade tensions between the U.S. and China.

US Stocks

U.S. equities met with resistance in August, with the S&P 500 giving back -0.7% on a total return basis.

The CBOE VIX index, which measures market volatility, spiked +42.4% last month. The so-called “fear index” continued to be rattled by the prospects of a hard Brexit and hawkish trade stances as well as the warning signs that this record-breaking expansion might soon be exhausted. We can quote what we said here after the market recovered from frayed nerves in May: “In historical context, a VIX that peaked above 21 and ended the month below 19 is not that frightening, but it compares most unfavorably with the much lower levels seen over the past couple years.” Except in August it peaked above 24.

International

World markets overall retreated even further than did U.S. equities.

In Europe, Germany’s DAX dropped -3.3% for the month, while Britain’s FTSE 100 lost -5.0% as markets digested news and rumors around Brexit.

In Asia, Shanghai’s SSE Composite eked out a +0.6% gain while Japan’s Nikkei 225 fell -1.8%. The Hang Seng, out of strife-torn Hong Kong, dropped -4.4%.

Central Banks

The world’s leading central bankers held their annual Jackson Hole, Wyo., meeting. It was, by all accounts, an awkward exchange.

Their shared brief is to keep inflation just high enough that it reflects economic growth, and unemployment as low as possible without causing a labor shortage which, in turn, creates inflation. The U.S. Federal Reserve is more than a century old; the Bank of England is more than three. Their current stewards and their direct-reports have decades of personal experience in keeping the economic train on the tracks. They know what they’re doing.

Or at least they did until the rules suddenly changed. They know how to fight a cyclical business slowdown. They even know how to react to a full-on financial crisis, as they proved in 2008, although then-Fed chair Ben Bernanke had to dust off his doctoral dissertation on the causes of the Great Depression to get ahead of that one.

But how do you guard against a recession for which the proximate cause is politically driven policy decisions? The Jackson Hole attendees have no more to go on than the reader of this space.

The usual method is lowering interest rates but, if these interest rates are already being dialed down as a tactic in the trade war – as we reported here last month – then there could be a shortage of ammunition when it’s time to redirect fire away from trade and toward a looming recession.

President Trump, who was in France at the time for the G7 meeting, received a great deal of criticism from Jackson Hole, some of which was captured by Reuters. This was unusual in that central bankers are generally insulated from politics, so rarely feel the need to discuss politics. But this is one of those aforementioned rules that were changed.

Commodities

West Texas crude slipped -5.9% in August to almost $55.10 per barrel.

When Wall Street gets jittery, the price of gold trends upward. The precious metal rose +7.2% to $1,529 per ounce by the end of August.

The British pound appears to have steadied, now that all the bad news has been discounted; it was essentially flat against the dollar in August. The euro, on the other hand, dropped another -0.8%. The emerging safe-haven Japanese yen appreciated +2.3% versus the greenback.

Bitcoin ended August at $9,615, toward the bottom of its recent trading range, a -4.4% decline for the month.

Is Your Card Up To Date?

Is your credit card about to expire? Have you recently received a new card? It’s easy to update your CREDIT CARD information. Just call us at 717-569-8162, or go to the Update Credit Card Information section under the Member’s Tab.

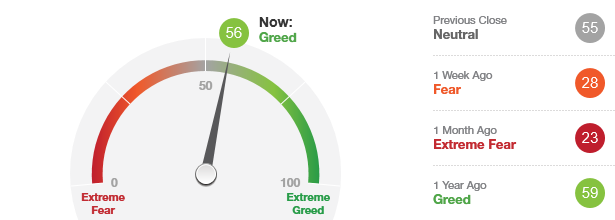

Fear & Greed Index

As of 9/11/19.

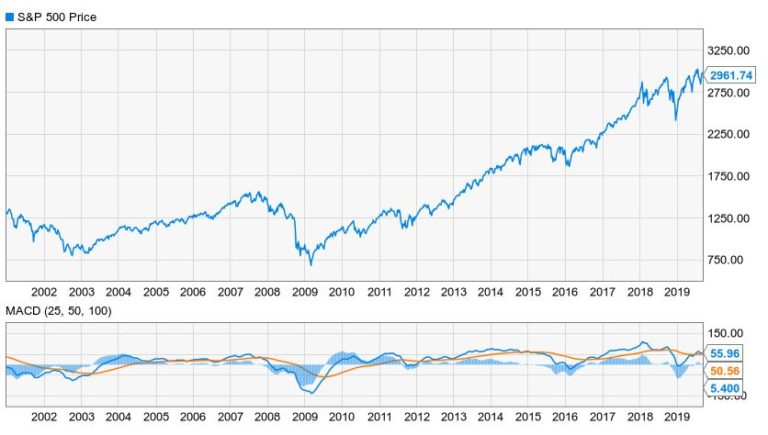

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

Getting educated

The American middle-class family has three major reasons to put money aside. The first is buying a starter home, which – we can safely assume if you’re reading this column – got checked off your list long ago. The last is, as you already know, retirement. But there’s that one in the middle that often gets neglected by investors and advisors alike: your children’s college education.

The 101 on 529s

The most commonly referenced vehicle for college savings is the 529 plan, which provides a tax shield for putting money aside for education. And a lot has changed since it was first added to the Internal Revenue Code in 1996.

To start with, it wasn’t always a savings plan. In a classic example of states acting as laboratories for federal policy, Michigan began allowing its residents to prepay their kids’ tuition at public institutions starting in 1986. The immediate effect was that the tuition bill for future members of the Michigan State Class of 2007 could be no more than that of their older cousin who still wore a Members Only jacket. Considering that tuition inflation is historically more than double that of consumer price inflation, this was an incredibly good deal.

It took more than a decade to sort out, but Michigan was able to persuade the IRS that its education trust could invest the prepaid tuition tax-free in order to make it viable; more correctly, it persuaded an appellate court to persuade the IRS. Today, there are 10 states that offer prepaid tuition plans and are accepting new applicants:

Florida

Illinois

Maryland

Massachusetts

Michigan

Nevada

Pennsylvania

Texas

Virginia

Washington

Once the law was settled, it became clear that the difference between what the parent prepaid for tuition in the 1980s and what its market value would be in the 2000s constituted income. The question switched to whether that income ought to be tax-exempt or just tax-deferred. After some political tussling, the tax-exempt advocates won. That means the donor can’t write off contributions in the year they’re made, but they won’t be taxed when they’re withdrawn for qualified expenses.

Once that was established, it opened the door to 529 savings plans. Rather than prepaying tuition, parents could invest in a vehicle similar to a retirement account, perhaps grow the money faster than colleges can raise their tuition, then pay education costs tax-free.

And that led to the question of what constitutes qualified college costs. Tuition, sure, as well as dorm rooms, meal plans and text books. But it took some time for off-campus housing and groceries to be accepted. It wasn’t until 2011 that computers were undisputedly covered. Student loan interest and debt are specifically denied as educational expenses.

While 529s continue to be administered by each state, the national standard for tax treatment enabled students and their parents to pick whatever school they chose. It no longer had to be their home state’s university. In fact, it neither had to be within that home state, nor a public school. It could be any accredited university, college or vocational school, as long as the beneficiary is at least a half-time student. You can even invest through any state’s 529 plan – it doesn’t have to be the one offered by the state you live in or where your kid plans to go to school.

And, as a result of the 2017 tax law, 529 savings can also be spent on K-12 education at public, private or parochial schools. Those who choose to home-school their children do miss out on this benefit.

Today, 529 savings plans might be state-sponsored, but they are professionally managed and generally invest in mutual funds rather than individual securities. In this tight labor market, some employers have started matching employees’ 529 contributions.

NerdWallet presents a couple of tables that compare each state’s 529 prepaid tuition and savings plans. It does not compare their historical returns or their fees. For that kind of information, consider contacting your financial advisor.

Advanced seminar

On a related note ABLE accounts, also called 529As, allow Americans with disabilities to put aside additional funds for education, per the Achieving a Better Life Experience Act of 2014. Prior to that, disabled people faced disincentives to saving for post-secondary education, up to and including loss of eligibility for government benefits. ABLE accounts allow their beneficiaries attending school to spend on expenses related to their disabilities without putting other benefits at risk, having their parents go through the expense of putting together a trust fund or simply living below the poverty line.

As part of the 2017 tax law, 529 funds can now be rolled over into ABLE accounts.

But there are other ways to save for your children’s education that are unrelated to 529s. One is the Coverdell Education Savings Account, also called an ESA or an education IRA. The advantage to ESAs is that you can invest in pretty much anything, unlike the 529 approach that limits you to selecting among mutual funds. As with 529s, the 2017 tax law allows ESAs to be used for K-12 expenses. There are income limits and you can only contribute up to $2,000 per year, so an ESA isn’t always the best basket for all your college savings eggs.

We have previously discussed Uniform Transfer to Minors Act and Uniform Gift to Minors Act accounts, so no need to repeat ourselves. But UTMA and UGMA funds can be used for educational purposes. Ditto for Roth IRAs; even though the “R” stands for retirement, withdrawals can be made for qualified educational expenses. This gets tricky, however. Qualified education expenses could help you avoid early withdrawal penalties if you are under 59.5 but income tax may still be due on earnings. Distribute at your own risk!

Homework

A recent study found that only 29% of taxpayers have even heard of 529s and know what they’re for. For comparison’s sake 32% not only know about 401(k) retirement plans but also put money into them every paycheck. And that 32% figure is itself nothing to brag about.

It gets worse. Fewer than half of all American parents are saving for their children’s education, and the average balance in a 529 is barely $18,000 and wouldn’t cover a year at a state college.

That’s why the states – and the professional money managers that run their 529 savings plans – are competing for investment dollars from plan-ahead thinkers like you, and state-by-state differences abound. Depending on where you live, there might be state tax benefits to keep you from straying. And there might also be tax disadvantages to paying all college costs out of the 529 rather than partially out of current income. Also, because 529s remain the property of the donor but are not included for estate tax purposes, they can be used for estate planning purposes – presuming you’re doing estate planning. But that’s an entirely different topic. It gets complicated, and perhaps you should discuss your goals and options with your financial professional.

Although there are different ways to save for your children’s education, the important thing is that you do so. Start now, even if you just put a few bucks a week into a generic savings account or parking some cash in Treasury bonds. You can roll it over into a more optimal vehicle after you and your advisor have determined what that is.

Steve

Steve Anglin, CPA is a Managing Partner at Smith Anglin Financial, and the Head of the Tax Preparation Services. He is also responsible for Smith Anglin’s compliance supervision. He holds a BBA in Accounting and a BBA in Real Estate, and numerous securities licenses and designations.

Steve Anglin, CPA is a Managing Partner at Smith Anglin Financial, and the Head of the Tax Preparation Services. He is also responsible for Smith Anglin’s compliance supervision. He holds a BBA in Accounting and a BBA in Real Estate, and numerous securities licenses and designations.

Steve Anglin, CPA is a Managing Partner at Smith Anglin Financial, and the Head of the Tax Preparation Services. He is also responsible for Smith Anglin’s compliance supervision. He holds a BBA in Accounting and a BBA in Real Estate, and numerous securities licenses and designations.