This month's models have been posted. There are CHANGES IN ALL THE MODELS (highlighted in yellow). The rest of the newsletter will be posted by the middle of the month.

What does ‘recession’ even mean anymore?

Type “definition of” into your Google search field and see what autocomplete prompts you get. Your algorithm may vary, but when we did it just now, “narcissist” was high on the list and “insanity” was even higher. But the top prompt was “recession”. Yet so many of us throw around this term without knowing what it means.

The broadest definition might be the most widely accepted, but at the expense of being the least useful: “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” That’s courtesy of the National Bureau of Economic Research, the Cambridge, Mass., charm school for Nobel laureates which was founded more than a century ago to study business cycles. Since the 1960s, the NBER has been the arbiter of when American recessions start and end.

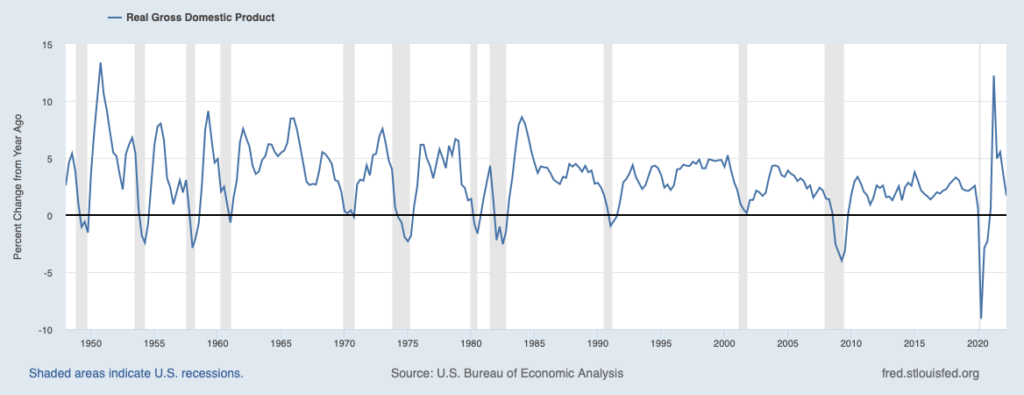

: The gray stripes are the recessions, whatever that means. Credit: Federal Reserve

Rules aren’t laws

The rule of thumb has always been: Two consecutive quarters of negative growth in gross domestic product constitute a recession. It’s been so ingrained that we had to go back to our college Economics textbook – some of us just can’t throw anything out – and were surprised to read that, even back then, the two-quarters rule was unofficial guidance.

Well, not everywhere. The United Kingdom adheres to the two-quarters rule in determining its recession dates. Other countries have their own sets of metrics.

This raises another question: How do we determine if the whole world is in a recession? That’s the job of the International Monetary Fund. The IMF used to define a global recession as a period in which the world’s aggregate GDP grows at a rate of less than 3% per year. (Three percent is a pretty good year for developed countries but is considered slow growth for nations that are still industrializing.) But the Fund changed that definition to a less quantitative one. As a result, the global recessions of 1998 and of 2001-2002 disappeared.

And yet, while the IMF is making recessions go away, the NBER appears to have invented one. The think tank appears to be using more art than science since declaring the single-quarter Covid-19 recession in 2020. It now says that contractions in income, employment, industrial production and wholesale or retail sales are taken into account along with contractions in GDP.

Are we or aren’t we, and does it matter?

There are smart people who disagree on the question: Are we in a recession right now?

We’ve had two – mildly – contractionary quarters in a row. So, the two-quarter rule – barely – applies. It really is a judgment call at this point.

“Most of the data [the NBER is looking] at right now continues to be strong,” Treasury Secretary Janet Yellin, a former Federal Reserve chair, told NBC News’s Chuck Todd. “I would be amazed if they would declare this period to be a recession, even if it happens to have two quarters of negative growth. We have a very strong labor market. When you are creating almost 400,000 jobs a month, that is not a recession.”

But there are troubling signs. The yield curve is inverted; that is, you can get a higher interest rate on a two-year note than on a 10-year bond. That means investors are incentivizedd to shorten their time horizons and go for fast bucks rather than long-term value. While it is a signal for a potential recession, an inverted yield curve is not always followed by one.

Still, not all sectors in the economy are doing equally well.

“I think we’re in a housing recession right now,” Robert Dietz, chief economist at the National Association of Home Builders, told Politico. “After a year and a half of post-Covid housing strength, this isn’t just a retrenchment to a more normalized trend — this is definitely a weakening.”

The Politico article notes that the housing market cooled since the stimulus supports ended. Meantime, mortgage rates nearly doubled in the first half of the year. Housing starts and builder confidence are plunging. The Great Recession started with collapsing real estate prices, so there’s every reason to believe that could happen again.

What next?

The consensus among financial professions is that the NBER … doesn’t matter. Who cares if some Harvard and MIT economists call our current state a mild recession, a contraction, a cyclical pause, a soft landing or make up a whole new term for a whole new phenomenon?

“Should I dump my tech stocks and buy dividend-paying value stocks?”

“Should I take my money out of equities altogether and put it all in fixed income?”

“Am I going to get laid off?”

These are the important questions. And you might want to talk to a trusted financial advisor to determine how to best insulate your portfolio from the worst effects.

Still, there is less difference between a mild recession and a mild expansion than there is between a mild recession and a depression. “Depression” is another one of those ill-defined terms, although Ronald Reagan got in the last word on that:

“Recession is when a neighbor loses his job,” the Great Communicator said during his 1980 campaign. “Depression is when you lose yours.”

Are You Prepared for Retirement?

Because you are a member of USPFA, you can schedule a complimentary consultation with an advisor from Smith Anglin Financial, a leading financial advisory firm for aviation professionals.

Gross domestic product declined at an annual rate of 0.6% in 2022’s second quarter, according to the second estimate released by the Bureau of Economic Analysis. This revises an initial a 0.9% estimated drop. The update reflects upward revisions to consumer spending and private inventory investment.

Total nonfarm payroll employment The US economy added 315,000 jobs in August, compared to a downwardly revised 526,000 in July, but above market forecasts of 300,000 and pointing to broad-based hiring across many sectors. The labor Force participation rate rose to 62.4% in August, the highest since March and up from 62.1% in July. Manufacturing added 22,000 jobs, and leisure and hospitality added 31,000, following average monthly gains of 90,000 in the first seven months of the year. August is historically a weaker month for employment data but nonfarm employment is now 240,000 higher than its pre-pandemic level in February 2020. Source: U.S. Bureau of Labor Statistics

Initial jobless claims The number of Americans filing new claims for unemployment benefits decreased by 6,000 to 222,000 in the week that ended September 3rd. This was below market expectations of 240,000. The figure marks the lowest amount of weekly jobless claims since the final week of May, highlighting a tight labor market and giving the Fed more space for aggressive interest rate hikes. On a non-seasonally adjusted basis, initial claims rose by 1,978 from the previous week to 175,842. The 4-week moving average, which removes week-to-week volatility, was at 233,000. Source: U.S. Department of Labor

The Consumer Price Index for All Urban Consumers unexpectedly rose another 0.1% in August on a seasonally adjusted basis after a flat July, the Labor Department reported. Over the last 12 months, the all-items index increased 8.3% before seasonal adjustment, compared with 8.5% in July suggesting that inflation is slowing but not yet contained. Increases in the shelter, food and medical care indexes were the largest of many contributors to the broad-based monthly all-items increase, which was offset by a 10.6% decline in the gasoline index. The index for all items less food and energy rose 0.6% in August, a larger increase than in July.

The benchmark 10-year Treasury yield ended August at 3.2% having started the month at 2.6%.

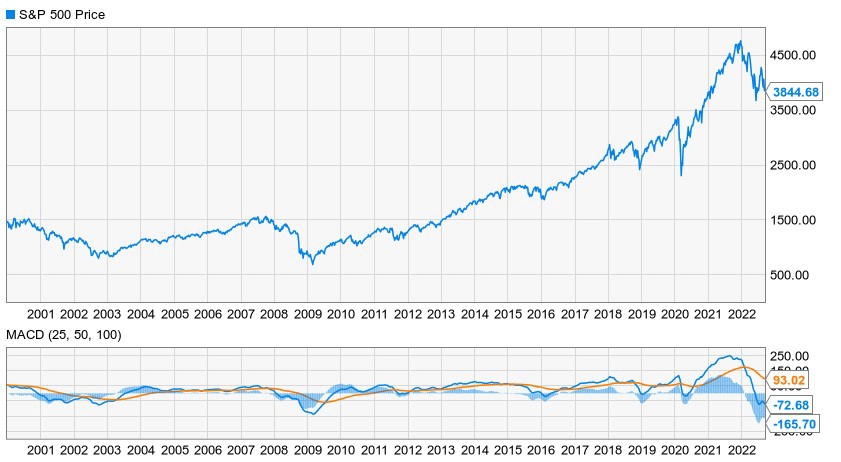

US Stocks

The S&P 500 fell -4.1% in August on a total-return basis, offsetting much of July’s surge. The CBOE VIX “fear gauge” ended the month up 21.3% at 25.87. This suggests investor confidence is back to the same shaky ground it was on two months ago.

International

Continental Europe followed Wall Street’s suit, with Frankfurt’s DAX and Amsterdam’s Euronext 100 down -4.8% and -4.7% respectively. London’s FTSE 100 thrived by comparison, dipping only -1.9%.

Asian stocks were narrowly mixed. Shanghai’s SSE Composite and Hong Kong’s Hang Seng declined -1.6% and -1.0%, respectively, while Tokyo’s Nikkei 225 eked out a +1.0% gain.

Central Banks

Every August, central bankers from around the world gather in Jackson Hole, Wyoming. It probably wasn’t much of a party this year. After all, they ended up taking the proverbial punch bowl away from equity investors by continuing with a campaign to tap down inflation by raising interest rates.

The Federal Reserve’s “overarching focus right now is to bring inflation back down to our 2% long-term goal,” Chair Jerome Powell told the assembly. “Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. ... While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.”

Commodities

West Texas Intermediate crude prices continued their decline, dropping -9.2% to end August at $89.55 per barrel.

Another indicator that inflation is slowing is the price action of gold. The safe harbor precious metal continued to settle lower, dipping -2.1% to end August at $1,726.20 per ounce.

The dollar gained +1.6% in Frankfurt, bringing it to virtual parity with the euro. The U.S. currency soared +4.5% in London and dipped -5.0% in Tokyo.

Bitcoin giveth and bitcoin taketh away. The bellwether digital asset dropped 15.1% to end the month at $20,240.86, erasing most of July’s bull run.

Is Your Card Up To Date?

Is your credit card about to expire? Have you recently received a new card? It’s easy to update your CREDIT CARD information. Just call us at 717-569-8162, or go to the Update Credit Card Information section under the Member’s Tab.

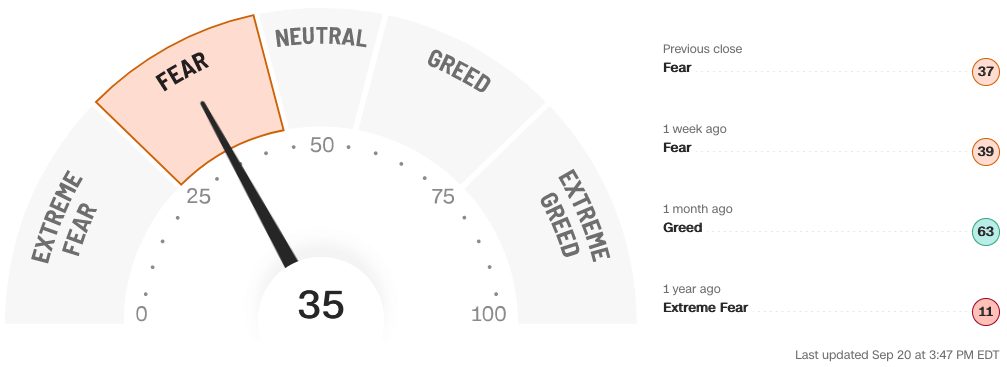

Fear & Greed Index

As of 9/20/2022

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

Master of your house, or master of disaster?

If you want to make God laugh, tell Him about your plans. – Woody Allen

But whatever you do, don’t ask God what’s so funny. You probably won’t find as much humor in it, especially if you just bought a home. There’s a legal term, “Act of God,” for a disaster outside of human control and for which no human can be held responsible. That is, there’s nobody you can sue for damages. If one of these Acts of God strikes your new home, you might be facing down a 30-year note on a smoking ash heap or small duck pond.

Fires and floods happen. So do earthquakes, tornadoes, and let’s not tempt fate by even pondering what else. If you can’t stop them, can’t mitigate the damage they cause, and can’t make someone else pay to clean up the mess and fix your property, what can you do?

You can get property insurance, of course, but that’s often an incomplete answer. If you’re like most people, you have the bear minimum coverage your lender required of you when you took out the mortgage. But does it cover everything it needs to?

Minimalist approach

The average American homeowner’s policy covers $250,000 in damages and costs $1,383 per year, according to Bankrate. But it’s a big country and that figure varies immensely by location. Bankrate, a popular personal finance site, parses data from Quadrant Information Services to show that property insurance is one of those few commodities which cost more in the middle of the U.S. than along the coasts. Oklahomans pay $3,519 per year while Hawaiians pay $376 – an order of magnitude less. At the city level, it costs $2,291 per year to insure a home in tornado-prone Fort Worth but, shockingly, only $867 in earthquake-prone San Jose.

By the way, it’s important to note that your credit score is likely to be an input to your insurance premium amount. If you have poor credit, you could be paying almost triple what someone with excellent credit is paying for homeowner’s insurance.

The insurer’s credit rating is also a factor. Insurance is a competitive game, and companies generally compete on price. This race to the bottom can seriously weaken any company’s balance sheet. When the company you’re hiring to offload your home loss risk becomes risky itself, it then has to pay more to secure reserves to pay off claims. If it’s just one company, fine, good riddance to bad management. But in Florida the problem appears to be endemic, meaning that you can’t just switch to another insurer for a better deal. The result is that Floridians’ property insurance premiums are skyrocketing.

What you get for the money though is pretty standard. Every homeowner’s insurance policy covers losses due to fire, storms, theft, vandalism and legal liability. According to Bankrate, the most common home insurance coverage types include:

Damage to the dwelling and other structures on the property: the home, detached garage, sheds, fences, playsets, and so on;

Personal property: clothing, furniture and electronics;

Personal liability: your own medical expenses as well as others’ injuries and property damage; and

Loss of use: rent on a temporary living space until the home can be occupied again.

But the only thing that’s 100% covered up to the limit is the dwelling. The insurance company will probably pay out only 10% to 20% of the damage to your garage. You’ll also only see restitution of between 50% and 75% of your personal property, and it might not apply to cash or collectibles.

And just because this is what’s considered standard coverage doesn’t mean it’s precisely what’s written in your policy. It’s always best to check. The standards are often set by algorithm, and they’re every bit as fallible as the humans who code them. The Denver Post ran an unsettling article about how many homeowners found that, even though they were covered for such a contingency, they found themselves seriously out-of-pocket for damages caused by December 2021’s Marshall fire. Twin Cities residents faced similarly poor outcomes as a result of wind and hail events, according to ABC News’s Minneapolis-St. Paul affiliate.

The gap

Policy Genius, an insurance comparison site, lists 13 exclusions that are probably not covered by your current policy. Those include:

Flooding

Earthquakes, landslides, and other ground movement

Termites, rats, and other infestations

Mold

Aggressive or dangerous dogs

Poor maintenance or neglect

Power surges or outages

Home-based businesses

Local building ordinance or law requiring you to bring your home up to code

Intentional damage caused by you or another resident family member

Nuclear hazards

War

Government action

If any of those last three listed actions occur, insurance is probably the least of your worries. Vermin and mold are things you can take action against – but the expense will likely fall to you.

It’s those top two, though, that are causing quite a firestorm of public policy debate in states as far apart as Florida and California; ironically, firestorms themselves are usually covered.

The more things stay the same …

Regardless of how much money you’ve managed to save for retirement, the equity in your house is still likely to be your largest asset. And just as you’ve mitigated risk by diversifying your securities portfolio by sector and asset class, you should consider how to best mitigate risk at home as well.

Do you have adequate coverage for storms and wildfires? Are you protected against floods or earthquakes at all? Are there less expensive plans out there which offer the same benefits?

Consider posing these questions to a financial professional who understands the ins and outs of property insurance.

-Chris

Chris Lott, CFP®, CPA

Financial Partner and Wealth Advisor

Chris Lott, CFP®, CPA is a Managing Partner at Smith Anglin Financial, and is a member of the firm’s Investment Committee. He regularly meets with prospective clients, counsels existing clients, leads investment portfolio analysis and develops materials for communicating with the firm’s clientele and target markets.