With Halloween in the rearview mirror now, it makes you wonder: why do we like to be scared so much in the first place? Experts will tell you there are several reasons, but basically fear works on our bodies like a stimulant. When we get frightened, a lot starts to occur in us physically. Our hearts beat faster. We breathe more intensely. We perspire and get butterflies in the pit of our stomachs. There’s also a hormonal component. When we perceive a threat, we feel more physically powerful and strong. We also feel more intuitive emotionally. This jolt to our physical and mental state is a feeling that we as humans are naturally drawn to. In those fearful moments, we’re more in tune with our senses. In many real ways, we’re more “alive.”

ECONOMIC NEWS

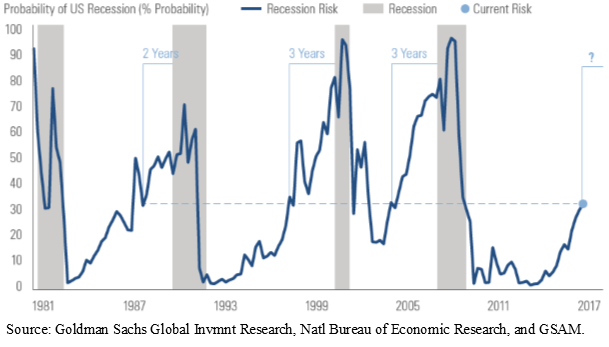

The U.S. economy remains lively and has been growing for the last 99 months (i.e., no recession), an expansion exceeded in length only 2 times since 1900, according to the National Bureau of Economic Research (NBER). It’s also picking up steam: for the first time since 2014, the U.S. economy has recorded back-to-back quarters in which GDP has grown at an annualized rate of at least 3%. Economists had expected growth to moderate in Q3 because of Hurricanes Harvey and Irma. However, the 3.0% growth achieved in Q3 may be hard to sustain moving forward. Since employment gains are responsible for about half of GDP growth, and with September’s unemployment rate clocking in at 4.2%, a rate at the lower end of the spectrum, there is limited room for employment to boost GDP growth moving forward.

Sentiment indexes in Europe have been mixed recently. One German business climate survey hit a record high in October, which is notable considering the backdrop of uncertainty surrounding Brexit, Catalan independence, and the final makeup of Angela Merkel’s ruling coalition. Uncertainty abounds in the United Kingdom as well. In the wake of the June 2016 Brexit vote, business investment has been flat, owing to uncertainty over the U.K.’s future relationship with the EU.

In Asia, Chinese economic indicators suggest a slowing economy, but one still firmly in growth mode. In Japan, Prime Minister Shinzo Abe won a landslide victory in the recent general election, opening the way for a push to amend the country’s pacifist constitution. Abe campaigned on the idea that the threat from North Korea requires leaders to remove any doubt over the legitimacy of Japan’s military. Abe’s victory was received well by investors as the Nikkei 225 Index pushed through 22,000 for the first time in 21 years.

CAPITAL MARKETS

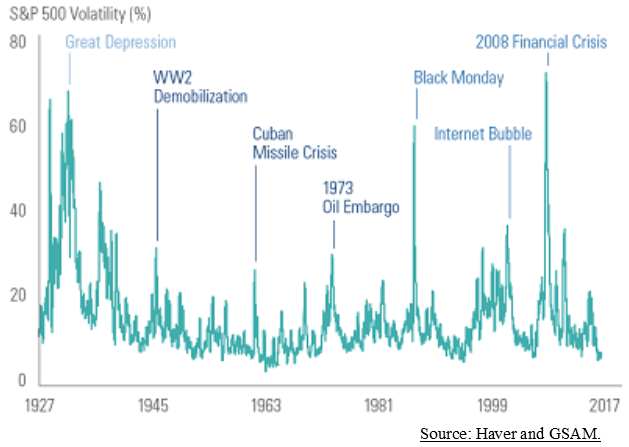

It was in October of 2007, 10 years ago last month, that the S&P 500 peaked before beginning a painful 17-month tumble that resulted in a more than 50% drop in value. What a difference a decade makes. The volatile, plummeting market action that prevailed 10 years ago has given way to the steadily rising, record-breaking markets of today. The major indexes climbed to record highs in September and then, as solid quarterly earnings reports began rolling in, did so again in October. Every major U.S. stock index advanced each week in October, extending the streak of positive weeks to seven in a row. The Dow topped the 23,000-point mark for the first time ever in October, and it was the index’s fourth 1,000-point milestone of 2017, a year that began with the index slightly below 20,000. It took only two and a half months for the Dow to climb from 22,000 to 23,000. All the while, market volatility has remained near record-low levels. In fact, volatility in the third quarter was the market’s least volatile quarter on record.

International stocks advanced in October as well. The MSCI EAFE Index, the primary equity benchmark for stocks from Europe, Australasia, and the Far East, posted a gain of more than 1.5% during the month. Japan’s stock market advanced to its highest level in more than two decades in October, while emerging market stocks, as tracked by the MSCI Emerging Markets Index, posted gains of more than 3%.

CENTRAL BANK POLICY

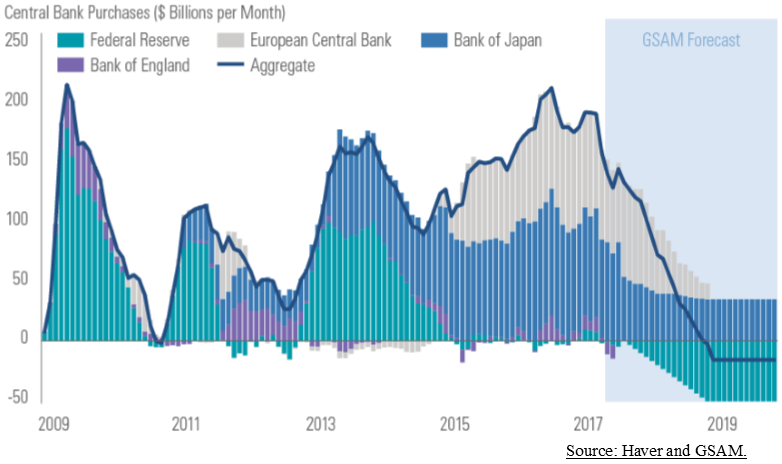

After having already raised rates twice in 2017, the Fed kept interest rates unchanged at its most recent meeting. The minutes from the Fed’s mid-September meeting show that policymakers appear to be leaning toward raising interest rates one more time, in December. Fed Chair Janet Yellen presided over what most believe will be one of her final meetings as chairman, and speculation swirls about who will replace her. President Trump is likely to tap Fed Governor Jerome Powell to be named chair. Among the leading candidates, he is viewed by many as closest to Yellen on his policy views, and he is set on normalizing interest rates.

The European Central Bank (ECB) announced in late October that it would begin slowly tapering its stimulus program. The ECB will halve its bond-buying program, and only buy €30 billion worth of European bonds each month starting in January 2018 and ending in September, a period longer than the six-month interval some had feared. The current amount is €60 billion a month. ECB president Mario Draghi said that interest rates will stay at present levels well past the end of the quantitative easing program, with the central bank keeping open the option of increasing the size and duration of QE if necessary. In addition, the ECB said it will reinvest the principal from maturing bonds for an extended period after the end of the bond-buying program.

Even as its peers in the U.S. and Europe begin to wind down stimulus, albeit ever-so-slowly, the Bank of Japan (BOJ) will continue its extraordinary monetary policy, keeping its short-term interest rate at -0.1% and maintaining its yield curve control and asset purchases. The BOJ’s argument is that extraordinary measures continue to be needed for an extraordinary problem. Their main problem is that, in terms of people, Japan is shrinking. The country’s strict immigration policies and its low birth rate mean that economic growth via more workers just isn’t an option. In 2010, Japan’s population was 128 million. By 2100, it’s projected to fall to 85 million, a drop of 34%! (source: The Brookings Institute).

WHAT SHOULD REALLY SCARE YOU

There’s also a darker side to our fears and our desire to face them. Psychologically, it’s appealing to vicariously experience what’s unknown, forbidden, and even bizarre. This is why horror films are so popular with adults and why most kids love a good ghost story. Both allow us to explore a fearful experience in a safer way. After all, for most of us, our daily lives don’t typically present ways to experience these intense feelings.

But Americans fear real world problems too. Chapman University in Orange, California polls Americans each year about their fears and recently released their Top Fears of 2017 survey. (https://blogs.chapman.edu/wilkinson/2017/10/11/americas-top-fears-2017/). This is the fourth year the school has conducted the survey, and the top ten fears listed is instructive into what Americans are the most apprehensive about at that time, even though one could argue the fears may be driven by headlines in the media. Two top ten fears involved government and policy, four involved environmental issues, and another two related to war. However, the remaining two fears in the top ten, while not being sensational, are very telling. Both related to running out of money. It’s apparent that Americans know deep down that they aren’t saving enough for the future … and they’re dead right.

According to the Center for Retirement Research at Boston College, the balances for 401(k) and individual retirement accounts (IRAs) held by households ages 55 to 64 – basically families within 10 years of retirement - reached a median $135,000 in 2016. Sadly, the Center found that half of households that are close to retirement have no 401(k) savings at all. A lot of Americans would tell you that, for them, saving for retirement just isn’t an option. A recent survey found that 43% of survey respondents said they “have difficulty [even] making ends meet” (source: National Financial Well-Being Survey, Consumer Financial Protection Bureau). No wonder saving is so hard.

The data is just as dismal for Americans on the cusp of retirement. The median value of a retirement account for someone 65 and over is about $60,000. Let’s assume at 65 you're going to live another 20 years; $60,000 isn't much to live on if you had to spread it out over two decades. This is important because the other two "legs" of the retirement "stool"—Social Security and pensions—are increasingly under pressure. As of January 2017, the average retiree receives $1,360 per month from Social Security. That's $16,000 a year, before taxes and Medicare premiums. About one-third of adults over 65 also collect a pension, but it's not usually a large amount of money. In fact, the median private pension was only $9,376 per year, according to the Pension Rights Center.

So, for those who collect Social Security and are lucky enough to also collect a private pension, they are getting roughly $25,000 a year in income. And those are the lucky ones. Anyone looking for more income is going to need to tap their personal savings or find extra income somewhere. That gets us back to the 401(k). That $60,000 is roughly $3,000 a year assuming a 20-year lifespan. That's not going to do much to move the needle. In fact, you’d need 10 times that amount of savings, around $600,000, to make a significant impact, but the vast majority of retirement plan balances aren't anywhere near that.

Given how difficult the situation is, you'd think people would be throwing money into retirement funds, but oddly they're not. Vanguard says that only 10.9% of 401(k) plan participants contribute the maximum amount allowed by IRS guidelines. That's partly because most people don't make enough money to contribute the total amount, but a lot of other people are just not incentivized enough to save. One thing's for sure: if we don't find some way to get people to save more, a lot of people are going to need to work well into their eighties, or they're going to outlive their retirement savings.

Market moves are not as easily measured and predicted, but economic and market data are helpful in forecasting trends. When you fly into bad weather, you rely on specific procedures for handling the turbulence and the rocky flight. Investing is similar in that you should rely on a consistent and disciplined approach to handling risk and volatility in the markets.